Most of us plan for our vacations with giddy anticipation. We pore over glossy travel magazines and surf web sites for the perfect place to pursue our passions, or to just put our feet up and relax. And, if we’re responsible, we save our pennies, sometimes years in advance, to make our dream a reality. But when it comes to the ultimate “vacation” – retirement – many people are far less prepared. You probably have a good idea of how to finance a week’s vacation, but do you have a viable plan for a vacation that can last decades? The truth is, many people actually spend more time thinking and planning for their vacations than their retirement.

Money Doesn’t Buy Happiness – But Can Buy Security

It is said that money does not buy happiness – and it’s true that even the most frugal of vacations can create the most lasting memories, such as camping in your own backyard when you were a kid. However, most people would agree that roughing it loses its appeal as one reaches more advanced ages. The reality is conditions that promote happiness—vitality made possible by proper nutrition and exercise, the comfort and security of a safe living environment, the ability to stay connected to each other and the world—are sorely compromised when funds are limited.

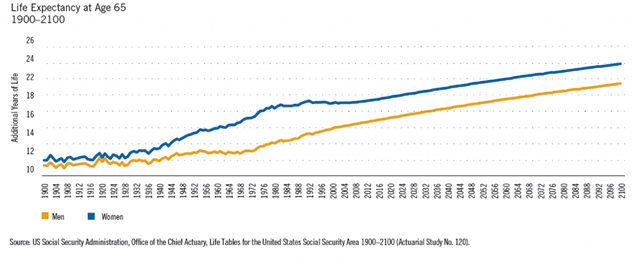

Until recently, retirement was not an overly worrisome societal issue, simply because much of the population never made it to that point. When 65 became the official age for collecting social security in 1935, average life expectancy in the United States was only 61.7 years.1 Few people could conceive of the possibility of living for decades without paid work. Nor was it necessary, as a large and relatively young workforce existed that could easily support the few who managed to live to a ripe old age. By 2008, however, the average life expectancy had increased.

And yet, according to the 2013 Franklin Templeton Retirement Income Strategies and Expectations (RISE) survey, three in 10 adults in the U.S. have not started saving for retirement.2 And it’s not just young adults who are without savings; 68% of respondents aged 45 to 54 and half of those aged 55 to 64 reported having less than $100,000 in retirement savings.

Thinking about Retirement Is Stressful; Living in Retirement should Not be

One of the more surprising results from our RISE survey was the age at which retirement-related stress levels peaked. As early as 15 years before retirement, fears associated with the financial consequences of growing older appear to spiral upward. The top three concerns for survey participants were health and associated expenses, longer lifespans and outliving their money. Although the vast majority (93%) indicated a solid grasp of the expenses involved, they were at a loss as to how to pay for them.

Many of us wouldn’t mind working a few extra hours to pay for our vacations, but putting off retirement and working longer simply may not be an option for many people due to factors like illness or layoffs. And, while most of us enjoy mapping out our vacation plans, the RISE survey revealed that the process of preparing financially for retirement was a source of stress for most. Nearly three-quarters (73%) of Americans said they find thinking about retirement saving and investing to be a source of stress and anxiety. But it doesn’t have to be that way.

Like working with a travel agent (or a travel app), working with a financial advisor can help alleviate planning stress and anxiety. The RISE survey revealed that individuals working with a financial advisor reported they were twice as happy and confident in their retirement income plans than those without. Among survey respondents who are currently working with a financial advisor, 87% reported feeling confident in their retirement income plan, compared to only 44% of those without a financial advisor. The survey also uncovered a correlation between working with a financial advisor and understanding one’s retirement income plan, with those who work with an advisor reporting being much more likely to actually understand their retirement income plan (86%) compared to those who do not work with an advisor (48%).

Interestingly, more than three-fifths (61%) of survey respondents looking to retire in the next 11 -15 years reported they would consider switching advisors (or use one for the first time) if they developed a written retirement income strategy.

One big difference between vacations and retirement is that when our allotted vacation funds run out, we simply go back to work. Once your retirement dollars run out, it’s not so simple, and the consequences are far worse than jet lag and lost luggage. But with the proper planning, it’s not only possible to live your dream, but even make your money work for you long after your working days have ended.

Traditional income-generating vehicles like bonds and money market accounts3 often are not generating sufficient income these days, so you may need to look elsewhere. Inflation can erode purchasing power of low-yielding investments, so you may want to consider vehicles that include other alternatives, such as dividend-paying equities.

Important Legal Information

All investments involve risks, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Bond prices generally move in the opposite direction of interest rates.

1. Source: Centers for Disease Control and Prevention/National Center for Health Statistics, National Vital Statistics System.

2. The Franklin Templeton Retirement Income Strategies and Expectations (RISE) Survey was conducted online among a sample of 2,002 adults comprising 1,001 men and 1,001 women 18 years of age or older. The survey was administered between January 10 and 22, 2013, by ORC International’s Online CARAVAN.®

3. Money market accounts are insured by the Federal Deposit Insurance Corporation (FDIC) for up to $250,000.

The information provided is not a complete analysis of every material fact regarding any country, region, market, industry, or fund. Comments, opinions, and analyses are those of Franklin Templeton Investments and the quoted person(s) and are for informational purposes only. Because market and economic conditions are subject to change, these comments, opinions and analyses are rendered as of the date of this posting and may change without notice. Opinions are intended to provide insight as to how the quoted manager analyzes securities and the commentary is not intended as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy.

All investments involve risk, including possible loss of principal.

For more information on any of our funds, contact your financial advisor or download a free prospectus. Investors should carefully consider a fund’s investment goals, risks, sales charges and expenses before investing. The prospectus contains this and other information. Please read the prospectus carefully before investing or sending money.

Data from third party sources may have been used in the preparation of this commentary and neither the author nor Franklin Templeton Investments has independently verified, validated or audited such data. We do not guarantee its accuracy. Reliance upon information in this posting is at the sole discretion of the viewer.

Links can take you to third party sites/media, directly or through new browser windows. We urge you to review the privacy, security, terms of use, and other policies of each site you visit. You use any third-party site, software, and materials at your own risk. Franklin Templeton does not control, adopt, endorse or accept responsibility for content, tools, products, or services (including any software, links, advertising, opinions or comments) available on or through third party sites or software. Franklin Templeton Investments and the author accept no liability whatsoever for any loss arising from use of this posting or any information, opinion or estimate herein.

Franklin Templeton Distributors, Inc.

© Franklin Templeton

http://us.beyondbullsandbears.com

© Franklin Templeton Investments