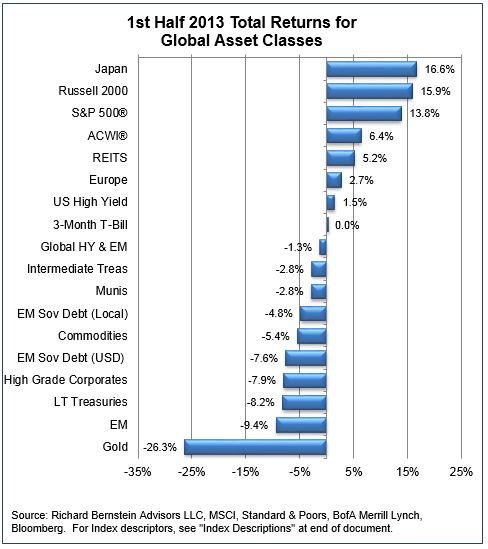

We have been ardent bulls on the Japanese stock market since last Fall.Our thesis has been a simple one:

For the first time in the history of our data, Japan began running consecutive monthly current account deficits.

Poor demographics and decreasing productivity left Japan with few options other than to depreciate their currency to reverse these deficits.

Historically, the Japanese stock market has generally moved inversely to the currency, i.e., the stock market tended to go up when the currency depreciated, and vice versa.

We were quite alone when we first invested for this theme, but that changed quickly as the Japanese stock market rose.Today, everyone is talking about Japan, and the Japanese stock market’s daily volatility has increased as leveraged, short-term traders now dominate daily results.

However, one must remember that economies do not change drastically on a daily basis.The media wants investors to believe that economies are constantly and rapidly changing, but watching economies is a slow and boring process.The increase in the volatility of the Japanese stock market, therefore, does not deter us from our longer-term investment focus.

Chart 1:

Current Account Deficits

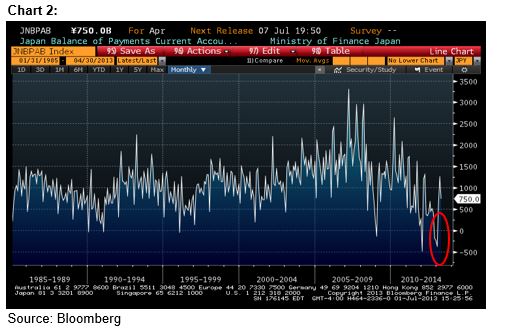

Chart 2 shows Japan’s current account surplus/deficit.There have been very few months when the country ran a current account deficit.However, Japan ran a deficit for three straight months toward the end of 2012.

That suggested to us that Japan might have to depreciate the Yen.

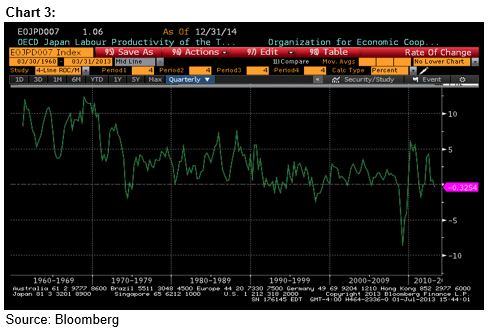

Productivity growth waning

Japan might have had alternatives to weakening the Yen if their productivity growth was demonstrably improving.However, as Chart 3 points out, that was not the case.Japan’s productivity growth was negative for 1q13, and has been negative in the past four years about as much as in the previous forty years.

Debt levels already high

Japan also didn’t have the option of financing growth via debt issuance.As most investors know, Japanese government debt as a percent of GDP has been high for some time (see Chart 4).The IMF is forecasting gross government debt as a percent of GDP will be 245% at year-end 2013.

Weaker currency

With other options not viable, it’s likely the Yen will secularly weaken.There will probably be shorter-term fluctuations in the Yen’s value, but we prefer to ignore the short-term news flow.Longer-term fundamentals seem to argue for a weaker Yen.

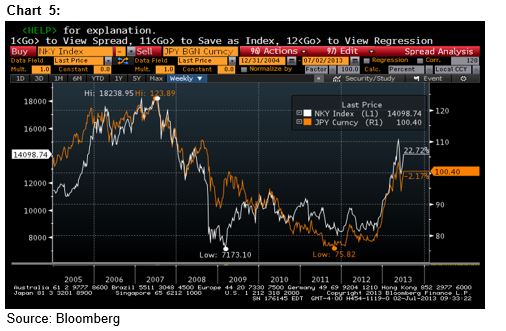

Chart 5 shows the secular relationship between the Yen/dollar exchange rate and the Japanese stock market.Since 2004, the Japanese stock market has tended to increase in value when the Yen depreciated, and decreased when the Yen appreciated.Prior to 2004, the relationship varied largely because of the on-going restructuring issues related to the deflation of their earlier credit bubble, the technology bubble, and other issues.

Japan is a notorious export-driven economy.A secularly appreciating Yen made Japanese goods less competitive and made foreign operations less profitable (i.e., Japanese companies’ offshore operations’ profits were translated to fewer Yen).In addition, the flood of capital into the emerging markets gave emerging market companies an added advantage.

Global fundamentals seem to be significantly changing, and the factors that hurt Japanese companies’ profitability and the Japanese stock market’s performance seem to be reversing.The Yen is depreciating and the cost of capital in the emerging markets is rising.Japanese companies are starting to recoup some competitive advantages.

The land of the rising market

Short-term trading volatility in Japan has unfortunately diverted investors’ attention away from the fact that economic and profit fundamentals seem to be improving.We have invested in Japan because of this secular backdrop, and expect the country’s secular fundamentals to improve.

Japan was one of the world’s best performing markets during the first half of 2013, but market volatility dominated the news flow and scared investors.Our research continues to allow us to remain dispassionate and focus on fundamentals instead of noise.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends.An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results.Indices are not actively managed and investors cannot invest directly in the indices.

S&P 500®Standard & Poor’s (S&P) 500® Index.The S&P 500®Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

Russell 2000®: Russell 2000®Index.The Russell 2000®Index is an unmanaged, market-capitalization-weighted index designed to measure the performance of the small-cap segment of the US equity universe. The Russell 2000 Index is a subset of the Russell 3000®Index.

MSCI ACWI®: MSCI All Country World Index (ACWI®).The MSCI ACWI®is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of global developed and emerging markets.

MSCI EM: MSCI Emerging Markets (EM) Index.The MSCI EM Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of emerging markets.

MSCI Europe: MSCI Europe Index.The MSCI Europe Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of developed European markets.

Japan: MSCI Japan Index.The MSCI Japan Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of Japan.

Gold:Gold Spot USD/oz Bloomberg GOLDS Commodity.The Gold Spot price is quoted as US Dollars per Troy Ounce.

Commodities:S&P GSCI® Index.The S&P GSCI® seeks to provide investors with a reliable and publicly available benchmark for investment performance in the commodity markets, and is designed to be a “tradable” index. The index is calculated primarily on a world production-weighted basis and is comprised of the principal physical commodities that are the subject of active, liquid futures markets.

REITS:THE FTSE NAREIT Composite Index.The FTSE NAREIT Composite Index is a free-float-adjusted, market-capitalization-weighted index that includes all tax qualified REITs listed in the NYSE, AMEX, and NASDAQ National Market.

3-Mo T-Bills:BofA Merrill Lynch 3-Month US Treasury Bill Index.TheBofAMerrill Lynch 3-Month US Treasury Bill Index is comprised of a single issue purchased at the beginning of the month and held for a full month.The Index is rebalanced monthly and the issue selected is the outstanding Treasury Bill that matures closest to, but not beyond, three months from the rebalancing date.

Long-term Treasury Index:BofA Merrill Lynch 15+ Year US Treasury Index.TheBofAMerrill Lynch 15+ Year US Treasury Index is an unmanaged index comprised of US Treasury securities, other than inflation-protected securities and STRIPS, with at least $1 billion in outstanding face value and a remaining term to final maturity of at least 15 years.

Intermediate Treasuries (5-7 Yrs):The BofA Merrill Lynch 5-7 Year US Treasury Index

TheBofAMerrill Lynch 5-7 Year US Treasury Index is a subset of TheBofAMerrill Lynch US Treasury Index (an unmanaged Indexwhich tracks the performance of US dollar denominated sovereign debt publicly issued by the US government in its domestic market).Qualifying securities must have at least one year remaining term to final maturity, a fixed coupon schedule and a minimum amount outstanding of $1 billion. including all securities with a remaining term to final maturity greater than or equal to 5 years and less than 7 years.

Municipals:BofA Merrill Lynch US Municipal Securities Index.TheBofA Merrill Lynch US Municipal Securities Index tracks the performance of USD-denominated, investment-grade rated, tax-exempt debt publicly issued by US states and territories (and their political subdivisions) in the US domestic market.Qualifying securities must have at least one year remaining term to final maturity, a fixed coupon schedule, and an investment-grade rating (based on an average of Moody’s, S&P and Fitch).Minimum size requirements vary based on the initial term to final maturity at the time of issuance.

High Grade Corporates:BofA Merrill Lynch 15+ Year AAA-AA US Corporate Index.TheBofAMerrill Lynch 15+ Year AAA-AA US Corporate Index is a subset of theBofAMerrill Lynch US Corporate Index (an unmanaged index comprised of USD-denominated, investment-grade, fixed-rate corporate debt securities publicly issued in the US domestic market with at least one year remaining term to final maturity and at least $250 million outstanding) including all securities with a remaining term to final maturity of at least15 years and rated AAA through AA3, inclusive.

U.S. High Yield:BofA Merrill Lynch US Cash Pay High Yield Index.TheBofAMerrill Lynch US Cash Pay High Yield Index tracks the performance of USD-denominated, below-investment-grade-rated corporate debt, currently in a coupon-paying period, that is publicly issued in the US domestic market.Qualifying securities must have a below-investment-grade rating (based on an average of Moody’s, S&P and Fitch) and an investment-grade-rated country of risk (based on an average of Moody’s, S&P and Fitch foreign currency long-term sovereign debt ratings), at least one year remaining term to final maturity, a fixed coupon schedule, and a minimum amount outstanding of $100 million.

EM Sovereign (USD) : TheBofA Merrill Lynch US Dollar Emerging Markets Sovereign Plus Index

TheBofAMerrill Lynch US Dollar Emerging Markets Sovereign Plus Index tracks the performance of US dollar denominated emerging market and cross-over sovereign debt publicly issued in the eurobond or US domestic market. Qualifying countries must have a BBB1 or lower foreign currency long-term sovereign debt rating (based on an average of Moody’s, S&P and Fitch). Countries that are not rated, or that are rated “D” or “SD” by one or several rating agencies qualify for inclusion in the index but individual non-performing securities are removed. Qualifying securities must have at least one year remaining term to final maturity, a fixed or floating coupon and a minimum amount outstanding of $250 million. Local currency debt is excluded from the Index.

EM Sovereign (Local)TheBofAMerrill Lynch Local Debt Markets Plus Index is designed to track the performance of sovereign debt publicly issued and denominated in the issuer's own domestic market and currency other than the more established top-tier sovereign markets. In order to be included in the Index, a country (i) must have at least $10 billion (USD equivalent)outstanding face value of Index qualifying debt (i.e., after imposing constituent level filters on amount outstanding, remaining term to maturity, etc.); and (ii) must have at least one readily available, transparent price source for its securities. In addition, the following countries are specifically excluded from the index: G10 countries, Euro members; all countries with a foreign currency long-term sovereign debt rating of AA3 or higher (based on an average of Moody’s, S&P and Fitch). Qualification with respect to country size criteria is determined annually based on information as of September 30th, but does not take effect until December 31st.

© Copyright 2013 Richard Bernstein Advisors LLC. All rights reserved.

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in, any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Specifically, and without limiting the generality of the foregoing, before acquiring the shares of any mutual fund, it is your responsibility to read the fund’s prospectus. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is an inherently risky activity, and investors must always be prepared to potentially lose some or all of an investment's value. Past performance is, of course, no guarantee of future results.

© Richard Bernstein Advisors