Global business and credit cycles are nothing new to investors. The familiar sequence of recession, recovery, expansion and slowdown plays out over time, influencing interest rates, credit availability, business climate and capital markets. It’s a time-honored process, but in practice, no two business and credit cycle pairings are exactly alike. Business and credit cycles tend to be driven by specific but varying factors that accumulate until an economic “tipping point” is reached, after which the business and credit climates deteriorate. Precisely anticipating these inflection points is impossible; however, identifying the drivers and monitoring their accumulation in the global environment is a possible, although complicated, task. A deep understanding of the complex relationship between the business and credit cycles may help identify the specific drivers of each pairing and provide valuable information to investors. To anticipate where cycles are headed, an investor needs to understand how central banks around the world are setting the price of credit, and how that action feeds the behavior of corporations, governments, consumers and investors.

Today, central banks have attempted to spur economic growth through substantial quantitative easing and low interest rates. The global economic recovery has been anemic thus far, even with central bank accommodation. Yields have remained historically low for an extended period, allowing corporations prolonged access to easy credit—a defining characteristic of this credit and business cycle combination. To help determine the key drivers of this cycle, we will first explore the typical, perhaps even idealistic,

connection between the credit and business cycles. Using this information, we will then review the current environment and discuss how we think this cycle will unfold.

The Typical Credit & Business Cycle Relationship

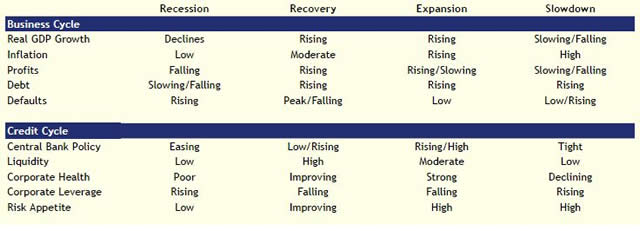

A business cycle refers to the expansion and contraction of economic activity over time. Typically measured by real GDP growth, business cycle phases include recession, recovery, expansion and slowdown. A credit cycle is related to, but different from, a business cycle. A credit cycle refers to the changing access to credit over time by governments, businesses and consumers. The credit cycle is more difficult to judge since it depends on the behavior of global central banks, the banking system, businesses and consumers, and the impact their collective behavior has on credit markets. The two cycles usually run in tandem; easy access to credit can boost economic activity, while tighter credit conditions can lead to slower growth or even recession. The typical relationship between the credit and business cycles is illustrated in the chart on the next page.

During a recession, GDP growth declines and businesses experience falling profits, causing leverage to increase and corporate balance sheets to deteriorate. Defaults begin to rise, usually peaking during the recovery phase of the business cycle. Through the recession and into recovery, corporations improve their balance sheets by shedding workers, reducing capital expenditures, building up cash and lowering debt.

Essentially, businesses are forced to deleverage because of the economic contraction. Meanwhile, central banks respond to declining GDP growth by opening the credit spigots in an attempt to reflate the economy. Risk appetite begins to improve as investors anticipate the worst of the recession is behind them. Credit spreads typically tighten dramatically, supporting relatively strong corporate bond returns. But, overall investor risk appetite and bond market liquidity remain low. As the easy credit from central bank policy begins to work and the economy begins to improve, liquidity returns to the market, but investors often remain cautious.

Moving into the expansion phase, corporate health is stronger, since both debt and expenses were reduced during the first part of the business cycle, and profits are rising. As the expansion continues, corporations begin to invest in capital projects and hire employees, causing the growth rate of corporate profits to slow. Early in the expansion, access to credit continues to be relatively easy, and resurgent investor risk appetite is supported by stronger economic conditions. Inflation pressures begin to build, in part due to a tightening labor market with rising wages. As this phase matures, central banks move toward tighter monetary policy to control inflation, which cools the economy. The expansion phase can be long, with a balance between stable but growing economic activity and tightening credit conditions and spreads. However, leverage begins to accumulate in the system, laying the foundation for future economic corrections.

Late in the business cycle, corporate profits are increasingly under pressure. As debt growth outpaces profit growth, corporate balance sheets begin to deteriorate and leverage increases. Stocks may continue to perform well in this late-cycle period despite slowing profit growth, but corporate bonds begin to

underperform Treasurys around this point in the cycle. As firms struggle to generate profits, managements may boost earnings per share with activities like issuing debt to purchase their own stock. So long as the expansion continues, this behavior tends to be good for shareholders but bad for bondholders, as the risk profile of the balance sheet has increased.

At some point, the economic expansion cannot be sustained, often because excess leverage, rapid growth and rising inflation pressures cause central banks to tighten monetary policies. Economic activity slows and tips, sometimes even tumbles, into contraction. Credit is generally tight, market liquidity evaporates since investors rush to sell higher-risk assets to a shrinking pool of buyers, and spreads widen. Investor panic can reinforce this part of the cycle. For the savvy fixed income investor, purchasing bonds trading below their fundamental value at this point can be beneficial over the long term. Eventually, central banks step in to restore order and begin to lower rates to stimulate economic activity. So, the cycle begins again.

The Atypical Drivers of This Cycle

Today, the business cycle appears to be in the early expansion stage for developed nations, while easy monetary policy has been provoking late-cycle behavior by corporations. Global central banks have prodded economic growth through what has been viewed as extreme intervention, keeping rates low and access to credit easy. As result, company balance sheets are largely repaired and flush with cash. So while the business cycle and central banks in developed markets are slowly progressing into expansion, the credit cycle has, at times, shown signs of pushing toward late cycle—a notable change from previous cycles when the business and credit cycles generally advanced together.

Focusing on the US, our current analysis suggests that credit spreads are more likely to tighten than widen from here, but that view is liable to change when we begin to see constant, increasing signs of late-cycle behavior emerging in the credit markets. However, we believe the most recent late-cycle signs will remain moderate as the global economy continues its path of gradual healing. Looking ahead, the pressing questions are: when and how quickly will the pendulum swing toward the deterioration of corporate balance sheets, and what will be the pace of global growth going forward? Backed by our macroeconomic research, which focuses on valuation, monetary and fiscal policy, global growth, corporate health, global risk appetite and liquidity, we will explore some the key factors that we believe will drive this cycle going forward. Specifically, we believe central banks will continue to keep rates low, although other forms of quantitative easing may decrease, which will support a tightening of credit spreads. Notably strong corporate health is beginning to show some signs of deterioration, but as economic growth slowly gains strength, attractive opportunities for business spending will likely emerge. An eventual strengthening of global growth, led by the US, is central to our view on the next evolution of this credit and business cycle.

The Importance of Easy Monetary Policy

Central bank liquidity was initially provided in direct response to the collapse of global demand that followed the 2008 financial crisis. Extreme central bank intervention has attempted to encourage economic growth, in part to offset tightening fiscal policies and deleveraging of governments, corporations and consumers. Many governments have been shrinking their bloated budget deficits, which has tempered global economic growth. Households have also been deleveraging following the sharp decline in the housing and equity markets, and corporations have been slow to invest, hire and spend. At the same time, uncertainty from the ongoing European crisis has contributed frequent setbacks to liquidity, financial stability and risk appetites. In many ways, this nascent global expansion has suffered more setbacks and volatility than previous cycles.

We believe the primary force supporting the continuation of this early expansion phase is the ongoing willingness of central banks to provide liquidity and keep real policy rates negative until an economic expansion truly takes hold. The chart at right illustrates the unusually persistent, easy posture of the Federal Reserve (the Fed), with the real federal funds rate remaining below

zero for nearly five years. In addition to low policy rates, the Fed has also been using unconventional monetary policies, like Treasury and mortgage-backed security purchases, to stimulate economic growth. While the Fed may begin to wind down its more unconventional policies, we expect the real federal funds rate to remain negative for a few more years. Yields may rise modestly, but the “search for yield” is likely to continue against the backdrop of easy monetary policy for some time.

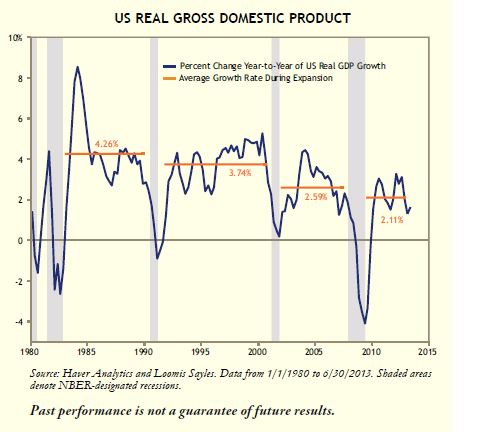

We expect this credit cycle to end in a typical fashion with tightening monetary policy, and we suggest credit spreads have a long time to run before they start widening. First, credit spreads typically do not begin to widen until the real federal funds rate reaches at least 2%, a threshold we are well below, which gives us some comfort in the durability of this credit cycle phase. Second, credit spreads can tighten fairly consistently even while Treasury yields are swiftly rising, as illustrated in the top chart, supporting our view that spreads will continue to move tighter even if Treasury rates begin to rise. Finally, and most specific to this cycle, if growth remains in the 3% range, we believe it could take around four years before US monetary policy becomes tight. Also, the economy’s peak level of real growth has declined with each previous cycle, as shown in the bottom chart. We expect this trend will continue and that the real federal funds rate will peak significantly lower than the prior cycle high of 3%.

Conversely, if this credit cycle progresses to slowdown then recession sooner than we expect, spread widening would likely be modest. First, the demand for yield fostered by easy money has allowed even marginal companies to come to the market to refinance their debt into longer maturities. With fewer bonds maturing in the near term, there is less risk of a maturity payment coming due at a time when the market is not willing to provide funding for new issuance. Second, we expect to see fewer defaults than in recent cycles because of the current strength of corporate health.

Corporate Health

With risk aversion high and demand weak, companies have been reluctant to expand investments in capital projects and employees. Over the last several years, our corporate health monitor reveals that companies have strengthened their balance sheets instead of focusing on business investment. Cash flows remain larger than capital expenditures, meaning that companies can still self-finance their investment needs while continuing to build up cash reserves. Short-term debt is now only 20% of all debt outstanding, a level not seen in the last 60 years. In total, the corporate ability to pay interest and dividends is stronger than we have seen in years, and return on investment remains strong.

More recently, the pace of balance sheet improvement has stalled, and signs of companies moving toward more shareholder-friendly activities have emerged. For example, corporate bond net new issuance surged in tandem with a burst of leveraged buyout and merger and acquisition activity in late 2012. Usually, a gradual shift from activities like stockpiling cash to activities like issuing debt to buy back stock is a fundamental signal that the credit environment has begun to change. While this activity proved to be a bit spurious, we are alert to the risk that this activity may emerge once again since cheap money can warp a company’s incentives. With interest rates artificially low, leveraged buyouts have become easier to justify, and the temptation to issue new debt to buy back outstanding equity shares has increased. The main force behind the current divergence of the credit and business cycles is this dynamic of an extended economic recovery and low interest rates.

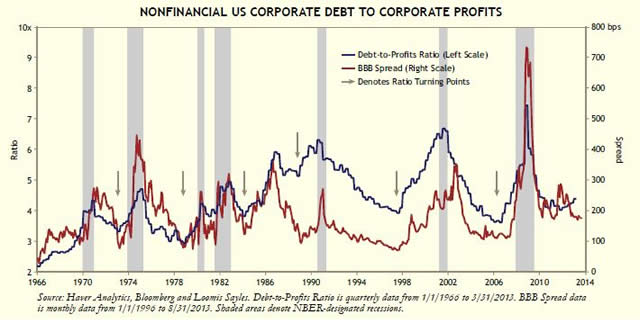

The corporate debt-to-profits ratio, shown below, illustrates the recent slowing improvement of corporate balance sheets. This ratio also represents the intersection of the business and credit cycles, so there are a lot of moving parts under the hood. When debt is growing faster than profits, this ratio will rise, signaling deterioration in corporate health. Not surprisingly, the ratio is highly correlated with credit spreads, as represented by the BBB spread in the chart. Over the last year, the ratio has been rising moderately, primarily due to slowing profits. Going forward, we expect this uptrend to stabilize as global growth improves and corporate profits strengthen.

While corporate behavior may be showing a few signs of late-cycle activity, we believe companies will begin to see better opportunities to expand investments in capital projects and workforce as the business cycle moves further into expansion and interest rates move higher. Corporations should also become less inclined to use easy credit to bolster earnings. We remain cautious about the global recovery, but we are quite optimistic on the resilience of the US expansion. We expect the higher rate of US nominal GDP growth to coincide with a pickup in business investment, gradually stronger productivity, profits and, eventually, wage growth.

US Growth Should Continue To Lead Global Growth

We believe the US economy will progressively gain strength and resilience through the later part of this year and into 2014. The pace of growth may not seem momentous, but it should improve incrementally nonetheless. For instance, we expect the pace of job growth to push through 200,000 net new jobs per month, which will help keep the unemployment rate declining. Income inequality will likely persist, but on average, incomes and the breadth of the economic growth will continue to expand. The US economic recovery has now moved into expansion, with every sector of the economy growing except federal government spending. Going forward, we expect the housing recovery, the improving health of banks and the developing shale revolution to help push the economy forward; the increasing diversity of the expansion should add resiliency to US economic growth. On the margin, acceleration of the US economy should help the rest of the world grow.

A global economic expansion may take several years to come together as headwinds are still present in several major economies. Notably, China is just beginning what we expect to be a structural downshift in growth as policymakers work to restrain rapid credit growth and enact structural reforms. A slower China would have the greatest impact on commodity-linked and emerging market economies. Europe continues to face many challenges. We are cautiously constructive on Europe in the near term, but we continue to expect economic improvement to be compromised by political and financial setbacks. And while Japan’s “Abenomics” may be a risky venture, it has provided a potential path to growth particularly likely to impress investors in the near future. On the whole, our outlook is for the global economy to improve, but we expect a synchronized global expansion will take some time to develop.

Our Outlook for Credit

When we step back to observe the global economic and financial landscape, we see some similar patterns across advanced economies: monetary policy should remain easy for an extended period, the push for tighter fiscal policy is fading, corporate balance sheets are unusually strong, credit spreads remain wider than is typical for this stage in the credit cycle, and there is a growing appetite for taking risk. It’s a pretty rosy picture if you step back far enough, but of course, the devil is in the details. Slow growth is often associated with higher asset price volatility since it is more fragile than strong growth by nature. So, we do worry about the economic transitions occurring in Europe, China and Japan, and financial spillovers could emanate from any of these regions. We believe these economies will at least muddle along with some growth as these countries manage their transitions. The anticipated resiliency of US growth should also provide some support for these economies.

Given the importance of corporate health to this credit cycle, we spend considerable effort assessing its future path. Low interest rates should spur capital investment in the corporate sector and housing investment in the private sector. But a policy of setting interest rate expectations low for an extended period comes with unwanted side effects, mainly the creation of leverage in many forms. We are closely monitoring decisions by corporate managements to see whether they use low interest rates to invest in future growth or to squeeze out more profits by restructuring balance sheets. Since an improving global economy should eventually present attractive opportunities, we believe the immense financial resources of the corporate sector will likely be directed toward investment in future growth.

In conclusion, our assessment is that this credit cycle is early in its expansion stage. As a result, we expect that it will have considerable time to mature and spreads should continue to tighten, typical of this phase of the credit cycle. Bond yields should rise as the global economy improves, but the rise may occur in fits and starts.

The pace of global growth will also likely be inconsistent over time. Credit spreads may widen in response to rising rates or slowing growth, but the longer-term trajectory for spreads should be to tighten as global growth improves. Rising risk appetites should also reinforce credit spread tightening. We remain sensitive to the possibility this credit cycle may not progress exactly as we expect, but we believe credit spreads should grind tighter over the next two years, and corporate bonds will continue to outperform Treasurys.

This paper is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not reflect the views of Loomis, Sayles & Company, L.P., or any portfolio manager. Investment recommendations may be inconsistent with these opinions. There can be no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis does not represent the actual or expected future performance of any investment product. We believe the information, including that obtained from outside sources, to be correct, but we cannot guarantee its accuracy. The information is subject to change at any time without notice.

Indexes are unmanaged. It is not possible to directly invest in an index.

LS Loomis| Sayles is a trademark of Loomis, Sayles & Company, L.P. registered in the US Patent and Trademark Office.

MALR010978 LEGREV022814

© Loomis Sayles