As we approach yet another self-induced “the sky is falling and the other guy is to blame” environment, recall that this situation is not uncommon. We have had 17 of these budget debt ceiling deadlines and yet we have unbelievably (said with extreme rolling of the eyes) been able to overcome our elected officials’ calls for the end of the world. The most recent time when the U.S. government shutdown was in November 1995 concluding in January 1996, when arguably the animosity and polarization was as pronounced as it is today. One slight difference is the shutdown occurred during President Clinton’s first term, while this is occurring during a potential lame duck period for President Obama considering the balance of power in the House of Representatives.

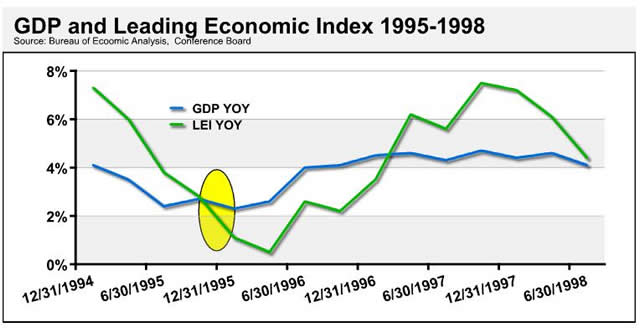

Now, just as we have learned from the recent sequestration, there seems to be a silver lining. Consider that the federal budget actually showed several large surpluses this calendar year that have caused the Congressional Budget Office (CBO) to estimate much lower budget deficits than previously thought. Now look at what happened to two economic metrics during the 1995-1998 timeframe as well as some sentiment numbers.

For comparisons sake, consider that during the 1995-1998 stretch, GDP averaged 3.79% per year, while the Leading Economic Index (LEI) averaged 4.45. To better put this in perspective, the average during this entire economic expansion (April 1991 – February 2001) was 3.60% for GDP and 3.7 for the LEI. The yellow bubble in the charts above and below denotes the period of temporary shutdowns where two briefly occurred in two months.

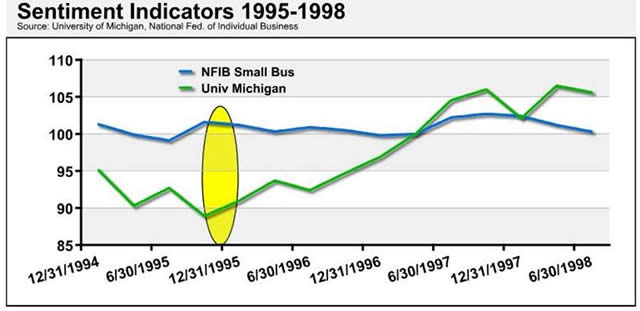

As we compared above, during the 1995-1998 stretch, the National Federation of Individual Business (NFIB) optimism index averaged 100.00 while the University of Michigan consumer sentiment number averaged 94.1. The average for the economic cycle (April 1991 – February 2001) was 100.89 for the NFIB optimism index and 97.36 for the University of Michigan consumer sentiment.

What we see is that while the sentiment numbers reacted negatively to the shutdown, the economic metrics were above the cycles’ averages. However, most telling was that the S&P 500 averaged 31% annually during this timeframe and never really had a steep correction during this three-plus-year timeframe.

While we recognize that the current game of “chicken” feels a bit more dramatic, the trend is still very positive for the economic metrics. It also helps with those concerned with tapering…at least for the very short run, as tapering will occur at some point.

One other positive that came out last week was the Fed flow of funds report showing some more significant growth in households and non-profits’ (NPO) balance sheets. Net worth for households and NPO increased to $74.82 trillion, and total cash deposits stood over $9 trillion.

To better bolster the potentially negative short-term impacts from a shutdown, consider that cash held at commercial banks stands at $2.44 trillion. This is not only significant in the totality of the number, but also as a percentage of total assets.

As we gear up for a potential shutdown, we must also recognize that the liquidity in the system is significantly higher than it was at the point of the previous government shutdown. History has also shown that the economy and markets recover quite quickly even if sentiment feels direr about the potential outcome. We would treat any selloff from the government shutdown as a buying opportunity in domestic equities with a focus on energy, basic materials, consumer discretionary and technology. We also continue to favor certain European markets (German DAX, French CAC 40 and the FTSE) as well as Asian emerging markets and China.

This commentary is for informational purposes only. All investments are subject to risk and past performance is no guarantee of future results. Please see thedisclosureswebpage for additional risk information. For additional commentary or financial resources, please visitwww.aamlive.com/blog.

© Advisors Asset Management