Our long-standing theme has been that the US stock market is again a growth market. Whereas investors generally still believe that the emerging markets are a growth story, the data increasingly suggest that growth is now predominantly in the developed markets. When it comes to quality, transparency, and consistency of growth, the US seems to stand above other markets.

Investors during the early-2000s waited for the old growth story to re-emerge (i.e., the technology bubble), and generally ignored the sea change that was underway that favored credit-based assets such as emerging markets, commodities, gold, real estate, hedge funds, and the like.

Today’s environment seems quite similar in that investors are again looking backward and hoping that the old, credit-based leadership re-emerges, while ignoring the major changes within the global economy. Most investors will readily agree that the global credit bubble is deflating. Yet, they continue to favor credit-based asset classes within their portfolios.

The global sea change we have repeatedly mentioned seems well underway. If a US investor today wants growth, one needs to look only in one’s back yard.

Who exactly is “printing money”? It’s the emerging markets.

Although it is very popular to say the US is “printing money”, the reality is that US money growth, at roughly 7%, is spot on the long-term average. The broad base of inflation figures beyond the much-maligned CPI consistently show that US inflation remains well under control. Not so in the emerging markets.

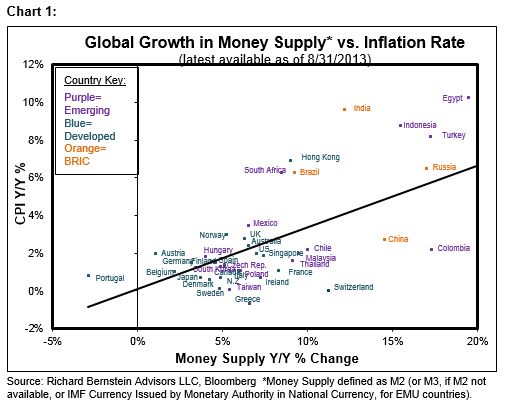

Chart 1 shows the current relationship between money growth and inflation among both developed and emerging countries. One can see that the highest rates of money growth and inflation are clearly in the emerging markets, and not in the developed markets.

It is curious that many investors still believe that the “emerging market consumer” is a viable investment theme despite the growing number of protests and riots in the emerging markets. One would think that protests and, in some cases widespread civil unrest, in Brazil, Turkey, Egypt, Indonesia, China, India, and other countries would highlight that inflation is increasingly cramping emerging market consumers’ purchasing power. How does one buy a toaster when one can’t afford the bread? The odds of the emerging market consumer being a source for growth seem to be waning. Nonetheless, many investors remain enthusiastic about the EM consumer investment theme.

Blind to the sea change

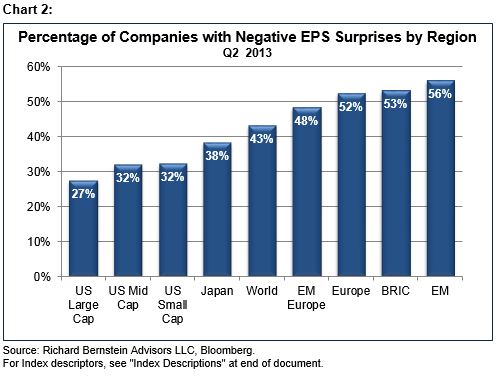

Earning surprise data strongly suggest that analysts refuse to believe that the global sea change is underway. For more than a year, the majority of emerging market companies have produced negative earnings surprises. 56% of emerging market companies and 53% of BRIC (Brazil, Russia, India, and China) companies produced negative earnings surprises in the latest reporting period.

The persistence of these negative earnings surprises suggests that analysts have been very slow to recognize the global sea change. Estimate revision data show analysts have been lowering estimates for emerging market companies, but they clearly have not been pessimistic enough.

Chart 2 highlights the proportion of companies by region that have reported negative EPS surprises during the last quarter. One can see that the data for emerging markets is quite poor, especially relative to US results.

Where is growth?

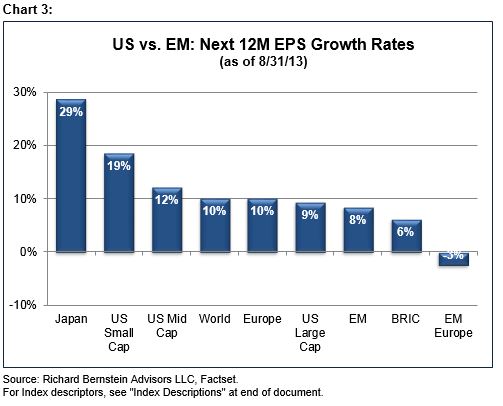

Although it might be hard to believe, the US and the developed markets are where the growth is today. Chart 3 shows 12-month projected earnings growth rates by region. Suffice it to say that the emerging markets’ growth is inferior.

We have previously highlighted that small cap US stocks were forecasted to grow faster than emerging markets, but one can see that even large cap US stocks are now expected to be faster growers than emerging market companies.

Contrarians might conclude Chart 3 demonstrates that expectations for the emerging markets are very low. However, Chart 2 suggests that “low” expectations could go “lower”

The global sea change continues

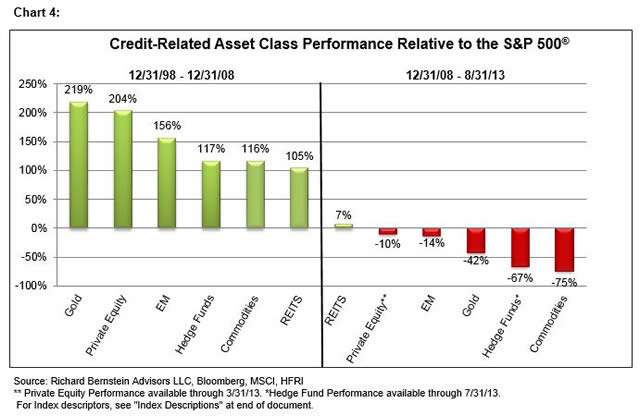

Significant market volatility has historically always signaled a change in market leadership. The growth stories going into a period of volatility are rarely the growth stories exiting such a period.

2008’s stock market volatility has so far been a typical signal that growth stories were changing. Going into 2008, credit-related assets outperformed US stocks because of the global credit bubble. The deflation of the global credit bubble since 2008 has led credit-related investments to underperform US stocks.

As Chart 4 points out, a global sea change is well underway, and our positioning will continue to reflect this new secular trend.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

US Large Cap: Standard & Poor’s (S&P) 500® Index. The S&P 500® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

US Mid Cap : Standard and Poor's MidCap 400® Index: The S&P MidCap 400® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the mid-sized companies of the U.S. stock market.

US Small Cap: Standard and Poor's SmallCap 600® Index: The S&P Smallcap 600® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the small cap segment of the U.S. stock market.

World: MSCI All Country World Index (ACWI®). The MSCI ACWI® is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of global developed and emerging markets.

EM: MSCI Emerging Markets (EM) Index. The MSCI EM Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of emerging markets.

EM Europe: MSCI Emerging Europe Index. The MSCI EM Europe Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of emerging markets in Europe.

Japan: Nikkei: The Nikkei 225 (NKY) Index: The Nikkei-225 Stock Average is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. The Nikkei Stock Average was first published on May 16, 1949.

Private Equity: The Cambridge Associates LLC U.S. Private Equity Index® is an end-to-end calculation based on data compiled from 1,052 U.S. private equity funds (buyout, growth equity, private equity energy and mezzanine funds), including fully liquidated partnerships, formed between 1986 and 2013. Pooled end-to-end return, net of fees, expenses, and carried interest. Historic quarterly returns are updated in each year-end report to adjust for changes in the index sample.

Gold: Gold Spot USD/oz Bloomberg GOLDS Commodity. The Gold Spot price is quoted as US Dollars per Troy Ounce.

Commodities: S&P GSCI® Index. The S&P GSCI® seeks to provide investors with a reliable and publicly available benchmark for investment performance in the commodity markets, and is designed to be a “tradable” index. The index is calculated primarily on a world production-weighted basis and is comprised of the principal physical commodities that are the subject of active, liquid futures markets.

Hedge Fund Index: HFRI Fund Weighted Composite Index. The HFRI Fund Weighted Composite Index is a global, equal-weighted index of over 2,000 single-manager funds that report to the HFR (Hedge Fund Research) database. Constituent funds report monthly net-of-all-fees performance in USD and have a minimum of $50 million under management or a twelve (12)-month track record of active performance. The Index includes both domestic (US) and offshore funds, and does not include any funds of funds.

REITS: THE FTSE NAREIT Composite Index. The FTSE NAREIT Composite Index is a free-float-adjusted, market-capitalization-weighted index that includes all tax qualified REITs listed in the NYSE, AMEX, and NASDAQ National Market.

© Copyright 2013 Richard Bernstein Advisors LLC. All rights reserved.

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in, any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Specifically, and without limiting the generality of the foregoing, before acquiring the shares of any mutual fund, it is your responsibility to read the fund’s prospectus. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is an inherently risky activity, and investors must always be prepared to potentially lose some or all of an investment's value. Past performance is, of course, no guarantee of future results.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS