Defining the EM Corporate Bond Opportunity

Finance is a numbers business. Investors study prices, yields, rates of return. However, when it comes to sizing up emerging markets, we think they should also pay attention to semantics. In the past, terming a country “emerging” made it synonymous with low credit quality and higher risk. But today, many emerging markets boast strong credit profiles while parts of the developed world buckle under heavy debt loads.

Consider that Chile and China are rated AA-, but Italy and Spain are rated BBB and BBB-, respectively.i With a combination of generally sound fundamentals and enviable growth prospects relative to the developed world, emerging markets have taken on new meaning.

So, too, have emerging market (EM) corporate bonds. Many investors consider EM corporates markedly riskier than EM sovereigns or purely a substitute for high yield bonds.ii We disagree. According to our definition, the US-dollar-denominated (“hard currency”) EM corporate universe is a growing, varied opportunity set that offers diversification across credit quality, geography and industry. And, in today’s low interest rate environment, many EM corporates are yielding more than EM sovereigns and developed market corporates, while offering stronger credit fundamentals. We believe these enticing characteristics create significant opportunity and should continue to draw investors to EM corporates.

The Changing Role of Emerging Markets

Global economic developments underpin the EM corporate story. Emerging markets have assumed increased significance in the global economy, representing 36% of global GDP as of the second quarter of 2013, up from only about 20% ten years ago.iii Four EM countries rank among the ten largest contributors to global GDP (China, Brazil, Russia and India). And though some market watchers lament slowing GDP growth in emerging economies, we continue to see a meaningful difference between EM and developed market (DM) growth rates. J.P. Morgan anticipates 4.6% GDP growth in emerging markets for 2013, relative to 1% GDP growth in developed markets.iv Longer term, we expect industrialization, urbanization and a growing middle class to continue to fuel EM growth. By 2025, nearly half of total global consumption is expected to come from emerging markets.v

A Growing Opportunity Set

Not surprisingly, an increased corporate presence in the emerging world has accompanied this economic transformation. In addition to regional and niche players, emerging markets are home to many strong global enterprises, some of which are world leaders in their respective industries. EM companies are assuming a more significant role in global corporate consolidation, often acquiring DM competitors. Record low borrowing costs, as well as investment and refinancing needs, are fueling the expansion of the EM corporate bond universe. As banks globally have continued to scale back term lending in the face of capital adequacy tests, more and more EM corporations are tapping the capital markets.

These dynamics are fostering a diverse opportunity set for investors. The J.P. Morgan Corporate Emerging Market Bond Index Broad Diversified (CEMBI BD), the common benchmark for EM corporate strategies, includes over three dozen countries and over 460 issuers across 12 broadly defined industry sectors.vi In the last 12 months alone, the number of issuers in the Index increased by more than 35%, and the market capitalization expanded by close to 15%.vii

Within the broadly diversified EM corporate universe, subsegments and individual issuers assume very different idiosyncratic risks and characteristics. As a result, we believe fundamental investors have an opportunity to identify potential sources of uncorrelated alpha and excess return. The chart at right, which shows the distribution of annual excess returns for EM corporate issuers versus US and global credits, highlights the breadth of opportunity. While US and global issuer returns are closely related, the EM return distribution is much wider.

EM vs. DM Corporates: Looks Can Be Deceiving

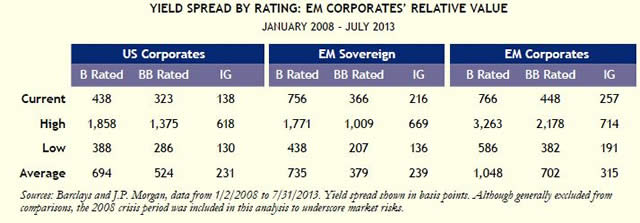

Though it is a predominantly investment grade asset class (the CEMBI BD is 68% investment grade), the burgeoning EM corporate debt universe retains a broad reputation as a high yield debt substitute. We do not think this characterization is accurate. EM corporates do tend to have higher yields than their comparably rated DM counterparts, as reflected by the major indices shown in the table below. However, these yields are not necessarily compensation for increased credit risk. EM corporates have been, on average, less leveraged than US corporates across the credit spectrum, as shown in the chart on the following page. What’s more, EM corporate credit grades often belie underlying business metrics because, according to ratings agency methodology, companies generally cannot be rated above their sovereign. When a sovereign is upgraded, many firms with constrained ratings automatically follow suit and enjoy meaningful price appreciation—particularly when the home country earns investment grade status. Thus, the additional yield in the EM corporate sector can be considered compensation for factors such as sovereign and liquidity risk. In view of these and other risks, the importance of fundamental credit research cannot be overstated. We think investors should look for EM companies with strong market positions and solid cash flow, the same qualities they would seek in DM corporates, while recognizing that there are more unknown variables in the emerging markets.

As the EM corporate debt asset class has matured, this combination of yield and increasingly strong fundamentals has contributed to attractive double-digit average returns with relatively low volatility. For the period January 2009 through July 2013, the CEMBI BD earned a Sharpe ratioviii comparable to other major fixed income asset classes, as shown in the table below. This volatility-adjusted performance measure signifies solid return per unit of risk, particularly given EM corporates’ investment grade bias.

Diversification

In addition to a potential yield advantage, the EM corporate sector can offer diversification benefits, including regional diversity and market structure. Companies from Mexico, China or Poland are not likely to move perfectly in sync with US markets. And, in general, EM corporate bonds have shorter duration than US corporate bonds. We believe this feature of the EM corporate market will be attractive in rising rate environments. On the following page, we show the one- and ten-year correlation of EM investment grade corporates to the 10-year US Treasury, as well as the US corporate bond space and risk assets such as equities and commodities.

Some investors attracted to the diversification and growth attributes of EM might ask, “Why not focus on EM sovereigns without worrying about corporate risk?” To be sure, investing in EM companies rather than sovereign debt adds an additional dimension to the analysis; however, as described below, we like the diversification, higher credit quality, incremental spread and shorter duration EM corporates have delivered relative to the EM sovereign universe (represented by the J.P. Morgan Emerging Market Bond Index Global Diversified (EMBIGD)).

• Issuer Diversification: As previously noted, the fast-growing CEMBI BD includes over 460 issuers. The EMBIGD, by contrast, contains 105 issuers and is largely constrained by the number of emerging countries globally.ix Additionally, as more and more emerging countries issue bonds in their home currency to mitigate currency risk, the opportunity set in this US-dollar-denominated sovereign Index has been shrinking. Over time, the EM corporate market should also see increased local-currency issues; however, this market is in its infancy and remains fairly limited.

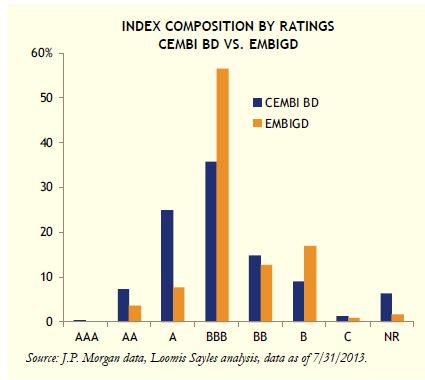

• Ccredit Quality: The CEMBI BD and EMBIGD vary significantly in terms of composition, as shown in the chart below. Though both indices are 68% investment grade, the CEMBI BD is distributed across ratings AA to C, while the EMBIGD is clustered heavily in the BBB to B space. These clusters mask the bifurcated risk/return profile of the EMBIGD’s constituent sovereigns. Brazil, the EMBIGD’s largest weight, is rated BBB and currently offers 241 basis points of spread, while B rated Venezuela, the seventh-largest weight in the Index, currently offers 966 basis points of spread.x

• Spread: In aggregate, the CEMBI BD currently offers spread levels similar to the EMBIGD. However, when comparing the investment grade components of each Index, the CEMBI BD’s investment grade constituents points relative to the EMBIGD’s investment grade holdings.xi

• Duration: The CEMBI BD’s duration is almost 1.25 years shorter than that of the EMBIGD.xii EMBIGD performance has benefited from longer duration in recent years, outperforming the CEMBI BD. However, in the face of rising rate concerns, we view the CEMBI BD’s shorter duration positively.

While we like the current risk/return profile of EM corporates relative to EM sovereigns, analysis of corporate issuers must start with the sovereign. A good company in a bad neighborhood is a difficult investment bet at best. Examining a country’s financial picture and governance practices is a critical component of credit research. Is there respect for the rule of law? How are shareholders treated? How are bankruptcies resolved? Loomis Sayles assesses these and other factors through in-depth, independent investment analysis.

Improving Market Liquidity

With such attractive relative valuations, it is no surprise that money has been flowing into the EM corporate sector, as measured in part by net flows into EM corporate debt mutual funds. According to J.P. Morgan, assets under management benchmarked against the EMBIG group of indices grew by 57% from the end of 2010 through June 2013. Over the same period, assets benchmarked against the CEMBI group of indices almost tripled, reaching $63 billion (albeit from a smaller base).xiii We believe demand for the EM corporate asset class will remain strong. Investors appear to have somewhat shifted focus from the sovereign markets in recent years, as ratings upgrades have narrowed EM sovereign yields and fewer US-dollar-denominated issues have come to market.

Importantly for EM corporates, investors such as EM sovereign wealth funds, insurance and pension funds have become larger players in the sector. J.P. Morgan reports that from 2005 to 2011, pension fund and insurance company assets in EM regions doubled, reaching a combined $4.3 trillion.xiv These sophisticated investors are generally more familiar with EM corporates, understanding the drivers of these issuers, particularly in their respective regions. The ongoing inflow of funds from sophisticated investors appears

to support the asset class, as “real money” buyers can help reduce volatility. For example, according to our trading desk, anecdotal evidence suggests local investors in the Middle East area have stepped in to buy local issuers when headline risks in the region have dislocated corporate bond spreads. We believe liquidity in the EM corporate markets will continue to improve as the investor base broadens and the markets mature.

Conclusion

As we have argued, EM corporates have generally been offering incremental value over comparably rated EM sovereigns and DM corporates (US corporate bonds represent DM corporates in the table below). In addition to this historic risk-adjusted spread advantage, we believe investors attracted to EM corporates should consider the sector’s favorable credit fundamentals, potential for growth and diversification. However, they must be cognizant of the risks and do their homework, carefully judging the relative merits of a company’s debt offering to the political and financial risks associated with the home country. Market risks should also be considered. When markets move into “risk off” mode, many frightened investors seek perceived safe havens such as US Treasurys. At times, emerging markets have been one of the sectors to sell off when this happens. Part of this might be for fundamental reasons like a slowing global or regional economy. But another element, in our view, has to do with investors moving in and out of the sector opportunistically. As the market for EM corporates matures, we believe investors could see the benefit of maintaining exposures, and the impact of “hot money” should be diminished.

Index Definitions

J.P. Morgan Corporate Emerging Markets Bond Index Broad Diversified (CEMBI BD) is a market capitalization weighted index consisting of US-dollar-denominated emerging market corporate bonds. According to J.P. Morgan, this index limits the weights of those index countries with larger corporate debt stocks by only including a specified portion of these countries’ eligible current face amounts of debt outstanding.

J.P. Morgan Emerging Markets Bond Index Global Diversified (EMBIGD) measures the market for US- dollar-denominated Brady bonds, Eurobonds, and traded loans issued by sovereign and quasi-sovereign entities of qualifying emerging market countries. According to J.P. Morgan, this index uses only a certain portion of the current face amount outstanding for instruments from countries with larger debt stocks.

Endnotes

i Standard & Poor’s. All ratings as of July 9, 2013.

ii The term “high yield bonds” refers to below investment grade bonds.

iii BofA Merrill Lynch Macroeconomic Data & Forecasts August 2, 2013.

iv J.P. Morgan, “Emerging Markets Corporates Reference Presentation, Maintain defensive positioning amidst volatility,” July 2013, by Yang-Myung Hong.

v McKinsey Quarterly, “Winning the $30 trillion decathalon: Going for the gold in emerging markets,” August 2012.

vi J.P. Morgan, CEMBI BD regional and country composition statistics, July 31, 2013.

vii J.P. Morgan, CEMBI BD instrument level composition and statistics, July 31, 2013.

viii Sharpe Ratio: Calculated by dividing the average of the index total return by the standard deviation of the index total return. The greater a fund’s Sharpe ratio, the better its risk-adjusted performance has been.

ix J.P. Morgan, CEMBI BD and EMBIGD regional and country composition statistics, July 31, 2013.

x J.P. Morgan, CEMBI BD and EMBIGD regional and country composition statistics, July 31, 2013. Standard & Poor’s ratings reflect the average of the issuers for the given country.

xi J.P. Morgan, CEMBI BD and EMBIGD regional and country composition statistics, July 31, 2013.

xii J.P. Morgan, CEMBI BD and EMBIGD regional and country composition statistics, July 31, 2013.

xiii J.P. Morgan, “The Mid-Year 2013 Emerging Markets Outlook,” July 12, 2013, by Joyce Chang.

xiv J.P. Morgan, “EM Fixed Income Rerates as an Asset Class,” September 2012, by Joyce Chang, Tejal Ray, and Camryn Collins.

Diversification does not ensure a profit or guarantee against loss.

Indexes are unmanaged and do not incur fees. It is not possible to invest directly in an index.

“Credit Quality” reflects a bond’s or bond portfolio’s credit worthiness, or risk of default, and refers to the highest credit rating assigned to individual holdings of

the security among Moody’s, S&P or Fitch; ratings are subject to change.

The value of non-US investments can fall as a result of political, social, economic or currency factors or other issues relating to non-US investing generally. Among other things, nationalization, expropriation, or confiscatory taxation, currency blockage, political changes or diplomatic developments can negatively impact the value of investments. Non-US securities markets may be relatively small or underdeveloped, and non-US companies may not be subject to the same degree of regulation or reporting requirements as comparable US companies. This risk is heightened for underdeveloped or emerging markets, which may be more likely to experience political or economic stability than larger, more established countries. Settlement issues may occur.

Below investment grade (also known as high yield) securities are subject to a high degree of market and credit risk. In addition, the secondary market for these securities may lack liquidity, which in turn may adversely affect the value of these securities and that of a portfolio.

S&P 500® is a registered service mark of McGraw-Hill Companies, Inc.

Russell Investment Group is the source and owner of the trademarks, service marks and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group.

This material is provided for informational purposes and is not intended to constitute legal, tax, or investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Investment recommendations may be inconsistent with these opinions. There is no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis does not represent the actual or expected future performance of any investment product. We believe the information, including that obtained from outside sources, to be correct, but we cannot guarantee its accuracy. The information is subject to change at any time without notice.

Past performance is no guarantee of future results.

LS Loomis | Sayles is a trademark of Loomis, Sayles & Company, L.P. registered in the US Patent and Trademark Office. MALR010743 LEGREV073114

© Loomis Sayles