Flip-flopping Federal Reserve (Fed) policy defined the third quarter. Last quarter, the Fed threw the markets a curve ball by announcing possible tapering of its large-scale asset purchases beginning this year. That “taper talk” set off a mini-riot in global bond markets. Many emerging market (EM) countries, like Brazil, India, Indonesia and South Africa, were the biggest victims, as their bond yields rose and their currencies crashed.

A THIRD MANDATE?

The Fed’s mandate is twofold—to provide maximum sustainable employment subject to price stability. Currently, it is failing to meet both targets because measured inflation is almost a full 1% below its 2% target, and the 7.3% unemployment rate is well above its 6.5% easy-money threshold. If the Fed had its eyes on a third goal, moderating excessive risk-taking, and wanted to shake up investor’s complacency, it succeeded.

We may be critical of the Fed’s communication efforts and the unexpected goal of reducing excessive risk- taking when the economy is failing to meet the central bank’s targets, but in the end, the Fed took prudent action and delayed tapering its asset purchases until sometime in the future. It was prudent because inflation is low and nominal US GDP growth is only 3.1%. The Fed was also cognizant of the impending debt ceiling debate and the potential negative impact on confidence that might occur if it was dragged out as painfully

as in 2011. The market’s response to taper talk added economic headwinds: mortgage rates shot up by over 1%, oil spiked on geopolitical concerns and the US dollar rallied against a large number of emerging market currencies. These factors combined to tighten monetary conditions, so the Fed elected to assess the overall impact on the economy before tapering.

Fed rhetoric caused several recent trends to reverse. For example, emerging markets posted some of the worst performance in the second quarter mostly due to the Fed, which is not unusual since several EM crises have been precipitated by tighter Fed policy. During the third quarter, many EM bond, currency and equity markets were the best-performing assets. Another unusual phenomenon from the second quarter was rising Treasury yields with widening credit spreads, which caused investment grade credit and high yield bonds to underperform our expectations but led to more attractive valuations. During the third quarter, spreads tightened resulting in solid excess returns for these sectors.

PLANNING FOR A QE EXIT

Rising Treasury yields with widening spreads in the second quarter and the turmoil in emerging markets indicate that exiting from quantitative easing (QE) could be challenging for many asset classes. As we have written many times previously, QE works through portfolio rebalancing and has the effect of pushing investors out the risk spectrum. Investors may move into higher-risk asset classes, where they may be uncomfortable with the additional risk, simply because they are searching for yield. As QE reverses, it is expected that some of those yield-seeking capital flows also reverse. In such an environment, investors need to sharpen their pencils and do their fundamental valuation work. Investors need a good valuation cushion to help deal with the potential volatility accompanying the ending of QE.

We still believe many credit spread sectors can offer value relative to Treasurys. The absolute returns for fixed income in the months ahead should be low, as we expect a gradual rise in yields. However, areas of fixed income that could provide positive absolute returns in a rising rate environment include bank loans, convertible bonds and residential mortgage-backed securities (RMBS). We also believe emerging markets offer better value at a time when we do not believe this is anywhere near a crisis environment that has hit EM in the past, such as the Asian crisis of 1997-1998 or the less developed country (LDC) crisis of the 1980s.

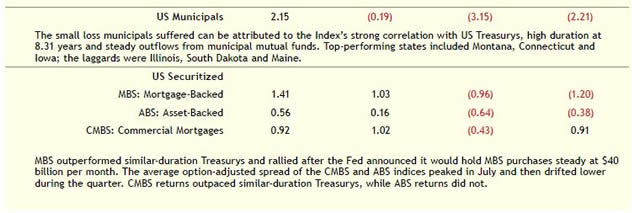

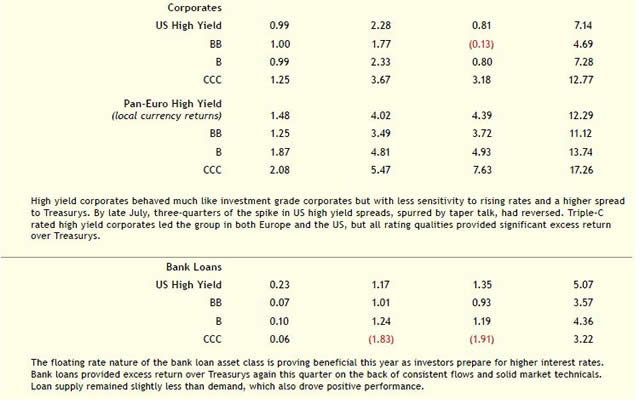

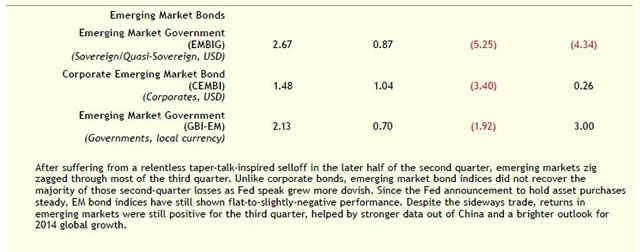

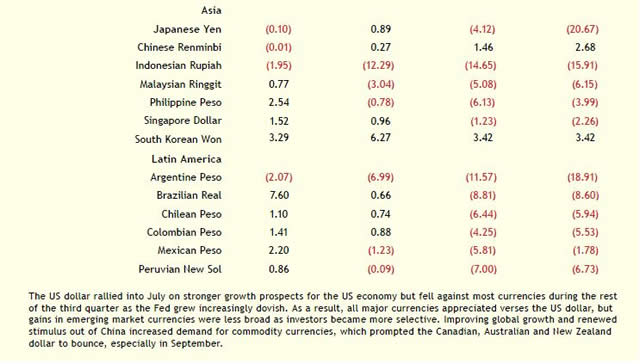

THIRD QUARTER REVIEW

1All returns sourced from Barclays Indices except: currency returns (Bloomberg), World Government Bond (Citigroup), Emerging Market Bond (JPMorganChase), and S&P 500 (FactSet and Ned Davis Research).

2Currency returns are relative to the US dollar.

Past performance is no guarantee of future results.

Indexes are unmanaged and do not incur fees. It is not possible to invest directly in an index.

This commentary is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P., or any portfolio manager. Investment recommendations may be inconsistent with these opinions. There can be no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis do not represent the actual or expected future performance of any investment product. We believe the information, including that obtained from outside sources, to be correct, but we cannot guarantee its accuracy. The information is subject to change at any time without notice.

INDEX DEFINITIONS

Barclays US Aggregate Bond Index is a broad-based benchmark that measures the investment grade, US-dollar-denominated, fixed-rate taxable bond market including Treasurys, government-related and corporate securities, MBS (agency fixed-rate and hybrid AR M pass-throughs), ABS, and CMBS.

Barclays US Government/Credit Index includes Treasurys (i.e., public obligations of the US Treasury that have remaining maturities of more than one year), government-related issues (i.e., agency, sovereign, supranational, and local authority debt), and corporates.

Barclays US Treasury Index includes public obligations of the US Treasury with at least one year until final maturity, excluding certain special issues such as state and local government series bonds (SLGs), US Treasury TIPS and STRIPS.

Barclays US Treasury Inflation Potected Securities Index is an unmanaged index that tracks inflation-protected securities issued by the US Treasury.

Barclays US Agency Index includes agency securities that are publicly issued by US government agencies, quasi-federal corporations, and corporate or foreign debt guaranteed by the US government (such as USAID securities).

Barclays US Municipal Index covers the US-dollar-denominated long-term tax exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and prerefunded bonds.

Barclays US Securitized Index consists of the US MBS Index, the Erisa-eligible CMBS Index, and the fixed-rate ABS Index. The US Mortgage- Backed Securities (MBS) Index covers agency mortgage-backed pass-through securities (both fixed-rate and hybrid AR M) issued by Ginnie Mae (GNMA), Fannie Mae (FNMA), and Freddie Mac (FHLMC). The US CMBS Investment Grade Index measures the market of conduit and fusion CMBS deals with a minimum current deal size of $300mn. The fixed-rate ABS Index includes securities backed by assets in three sectors: credit and charge card, auto and utility.

Barclays US Corporate Index is a broad-based benchmark that measures the investment grade, fixed-rate, taxable, corporate bond market. It includes US-dollar-denominated securities publicly issued by US and non-US industrial, utility, and financial issuers that meet specified maturity, liquidity, and quality requirements.

Barclays Euro Corporate Index tracks the fixed-rate, investment-grade euro-denominated corporate bond market. Inclusion is based on the currency of the issue, not the domicile of the issuer. The index includes publicly issued securities from industrial, utility, and financial companies that meet specified maturity, liquidity and quality requirements.

Barclays Sterling Aggregate Corporate Index is a broad-based benchmark that measures the investment grade, fixed-rate, taxable, corporate sterling-denominated bond market. Inclusion is based on the currency of the issue, not the domicile of the issuer. The Index includes publicly issued securities from industrial, utility, and financial companies that meet specified maturity, liquidity and quality requirements.

Barclays US Corporate High-Yield Index measures the market of US-dollar-denominated, non-investment grade, fixed-rate, taxable corporate bonds. Securities are classified as high yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below, excluding emerging market debt.

Barclays Pan-European High-Yield Index covers the universe of fixed-rate, sub-investment grade debt denominated in euros or other European currencies (except Swiss francs). Must be rated high-yield (Ba1/BB+ or lower) by at least two of the following rating agencies: Moody’s, S&P, Fitch. Excludes emerging markets.

Barclays US High Yield Loan Index covers syndicated term loans which are US-dollar denominated, with at least $150 million funded loans, a minimum term of one year, and a minimum initial spread of LIBOR +125. Standard & Poor’s 500 (S&P 500®) Index is a market capitalization-weighted Index of 500 common stocks chosen for market size, liquidity, and industry group representation to measure broad US equity performance.

S&P 500® is a registered service mark of McGraw-Hill Companies, Inc. Citigroup World Government Bond Index (WGBI) measures the market for the US and most developed nation government bond markets. Countries must have a minimum rating of A3/A- by both Moodys’ and S&P to enter the index and will be removed from the index if the ratings fall below Baa3/BBB-.

JPMorgan Emerging Markets Bond Index Global (EMBIG) measures the market for US-dollar-denominated Brady bonds, Eurobonds, and traded loans issued by sovereign and quasi-sovereign entities of qualifying emerging market countries.

JPMorgan Corporate Emerging Markets Bond Index (CEMBI) is a market capitalization weighted index consisting of US-dollar-denominated emerging market corporate bonds.

JPMorgan Government Bond Index-Emerging Markets (GBI-EM) tracks local currency bonds issued by emerging market governments.

MALR011122

© Loomis Sayles