There’s a popular saying in the US, “good things come in small packages,” which is generally a statement about gifts of jewelry. My team and I find this saying can apply to the investment world, too, as we often find companies that are small in size, but which may have big long-term potential.

Emerging-market country indices are often dominated by a handful of large businesses, typically from the energy, banking, telecommunications, heavy industry and mining sectors. Political or global macroeconomic factors often influence such businesses more than their local economies. Our team doesn’t base its decisions on benchmarks—we take a bottom-up approach to investing. As such, we often find attractive opportunities in individual smaller and mid-sized companies, which tend to be found in more entrepreneurial sectors such as consumer discretionary and light industrials. Many of these companies are more domestically oriented than their larger counterparts, and thus can be better aligned with the factors driving economic growth in the individual country or market in which they operate.

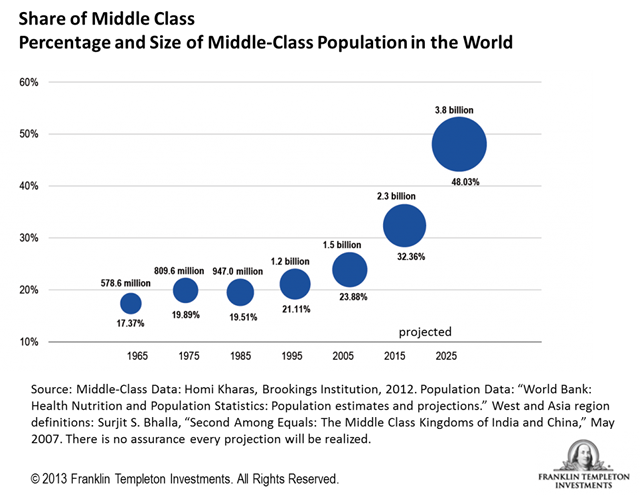

Middle-Class Influence

Typically, such companies are also more consumer-focused than their larger peers, exposing them to what we see as a key potential driver of emerging-market company profitability—the ongoing pivot in a number of emerging markets away from export- and investment-oriented growth toward growth based on rising consumer demand. The middle class around the world is growing, and it’s having a dramatic impact on consumer behavior in emerging markets. With more money to spend, many people in emerging markets are clamoring for consumer goods, from beer to clothing to cell phones. Additionally, as people gain more status, they often gain more clout to influence politics and policy—for the better.

The definition of “middle class” may differ from country to country, and according to whether the country is an emerging or a developed market. In the case of Africa in particular, the African Development Bank defines “middle class” largely in terms of higher income relative to the average; that average is, of course, lower in Africa than in developed countries. The bank estimates that more than 34% of the African population (nearly 350 million people) fit the description of middle class in 2011, up from 27% in 20001. It’s clear the consumer culture is growing there, along with discretionary income—something I’ve witnessed first-hand.

Filling a Niche

Many smaller companies are also often at an earlier stage in their life cycle, and thus can offer the potential to experience faster growth than the broader equity market. For example, we have identified several relatively small companies in markets such as South Korea and Hong Kong that have come to dominate a number of local consumer sector niches through strong manufacturing, marketing and management systems, but they remain small in a global context. As these businesses use skills honed in their local market to expand into neighboring emerging markets, they have often enjoyed accelerating growth.

Exploration of the smaller-companies segment is an important part of our overall research effort as some small-capitalization stocks can potentially grow to be the giants of the future. Some businesses first identified within our smaller-companies research, for example in pharmaceuticals and consumer staples, have evolved into large-capitalization companies. Furthermore, data uncovered by research into smaller companies can add significantly to our understanding of underlying conditions in emerging-market economies.

We feel the potentially negative aspects of smaller-company investment are manageable. These include a costlier research effort, information shortfalls, increased volatility (particularly over the short-term) and limited liquidity. Investing can sometimes require patience, but we think our long-term focus helps to manage these risk factors.

Moreover, the sheer number and variety of opportunities permits diversification2; our research team (as of September 2013) has identified approximately 21,500 companies within our emerging-markets, smaller-company universe. We see the information deficit as more of a potential advantage than a problem. When knowledge is scarce and hard to access, valuation anomalies can arise, and we believe our research methodology leaves us well placed to uncover such opportunities. We think the strong local presence of our emerging-markets team is also a big asset, with members currently located in 18 cities across Asia, Central and South America, Europe, the Middle East and Africa.

With these factors in mind, we believe investors concentrating only on larger-market constituents may miss out on some of the most dynamic areas of emerging-market economies. Detailed, stock-focused research aimed at identifying the drivers of company performance and profitability is a crucial investment process in this environment, in our view. Thus, we believe smaller companies represent a distinct investment opportunity, particularly for long-term investors seeking to capitalize on the dynamic growth in many emerging markets.

1. Source: African Development Bank, “The Middle of the Pyramid, Dynamics of the Middle Class in Africa,” April, 2011.

2. Diversification does not guarantee profit or protect against loss.

The information provided in this posting is not a complete analysis of every material fact regarding any country, region, or market. Comments, opinions and analyses contained herein are those of Dr. Mobius and are for informational purposes only. Because market and economic conditions are subject to change, his comments, opinions and analyses are rendered as of the date of this posting and may change without notice. His opinions are intended to provide insight as to how he analyzes securities and his commentary is not intended as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. Reliance upon information in this posting is at the sole discretion of the viewer. Please consult your own professional adviser before investing.

All investments involve risks, including the possible loss of principal. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging market countries involve heightened risks related to the same factors, in addition to those associated with these markets' smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Such investments could experience significant price volatility in any given year. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

Data from third party sources may have been used in the preparation of this commentary and neither Dr. Mobius nor Franklin Templeton Investments has independently verified, validated or audited such data. We do not guarantee its accuracy.

Franklin Templeton Investments and Dr. Mobius accept no liability whatsoever for any loss arising from use of this posting or any information, opinion or estimate herein.

Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton Investments’ US registered products, which are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable legislation. Products, services and information may not be available in all jurisdictions and are offered outside the US by other Franklin Templeton Investments affiliates and/or their distributors as local legislation permits. Please consult your professional adviser for information on availability of products and services in your jurisdiction.

Copyright © 2013. Franklin Templeton Investments. All rights reserved.

mobius.blog.franklintempleton.com

© Franklin Templeton Investments