We remain very concerned about emerging market stocks and bonds.The recent outperformance of EM stocks is again luring investors to once again touch the hot stove.Emerging markets seem to have some significant structural and cyclical issues about which investors seem unaware or seem to be ignoring.

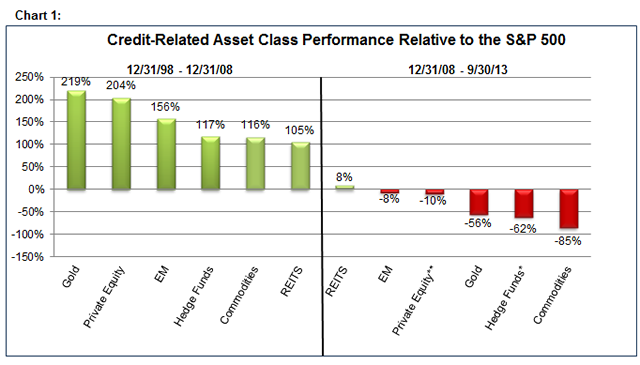

Volatility always signals a change in leadership within the equity markets.The growth stories going into a period of volatility are rarely the growth stories afterward.2008’s bear market has so far mirrored that historical precedent.Prior to 2008, credit-related asset classes outperformed traditional US stocks as the global credit bubble inflated.Since 2008, however, credit-related asset classes, including emerging markets, have underperformed traditional US stocks (see Chart 1).

It’s profits growth not economic growth that matters

Our analyses through the years have clearly demonstrated that stock market performance is more closely tied to profits cycles than to economic cycles.Markets care more about corporate profits than about GDP, but most emerging market investors nonetheless focus on GDP growth.

Investors’ expectations of profits growth, both cyclically and secularly, for the emerging markets, have consistently been too optimistic.The profits outlook in the emerging markets is actually poor and appears to be deteriorating further.

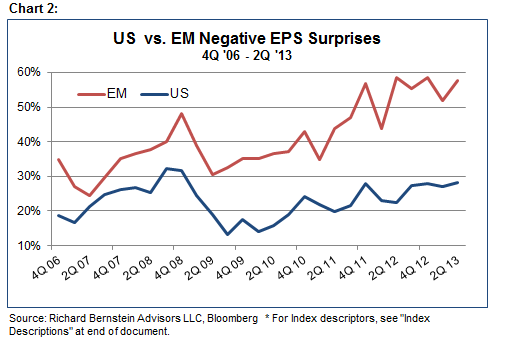

The majority of emerging market companies has been reporting negative earnings surprises for more than a year.Chart 2 shows the proportion of emerging market companies that have reported negative earnings surprises versus the same tally for S&P 500 companies.Whereas about 25-30% of US companies have been reporting negative earnings surprises during the past year, about 55-60% of EM companies have reported negative surprises.

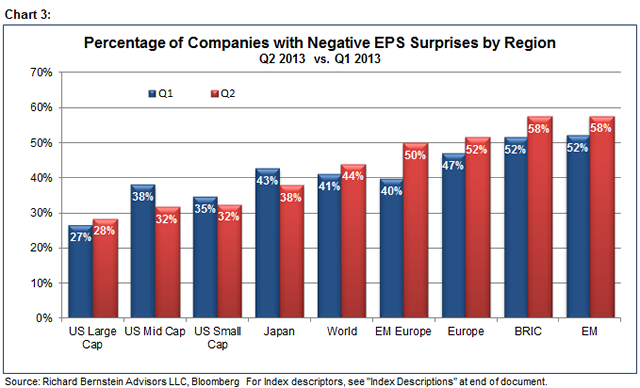

These statistics are even more powerful when compared to other regions’ negative earnings surprises.Chart 3 shows the proportion during the past two quarters of each region’s companies that have reported negative earnings surprises.Note that EM is among the worst.

The consistent trend of negative earnings surprises suggests to us that investors refuse to believe that the global economy is changing.Analysts refuse to significantly alter their growth projections because they apparently believe that the problems in the emerging markets are only temporary.

The US is a better growth story…

Because analysts generally believe that the problems in the emerging markets are temporary, long-term growth projections have been similarly downward-sticky.However, even despite that hesitancy to accept that emerging market companies’ profits growth is changing, EM companies’ long-term growth projections are not superior.

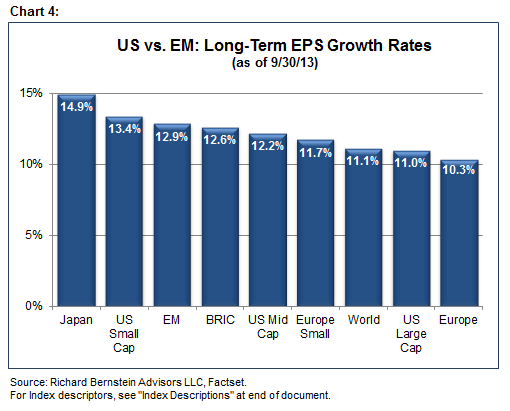

Chart 4 shows bottom-up, long-term earnings growth projections by region.Contrary to what many might assert, the emerging markets are not the world’s best growth story.As we have pointed out many times, US small cap companies offer superior growth to that offered by the emerging markets.

The US is now a better growth story than are the emerging markets!!

…but no one believes it.

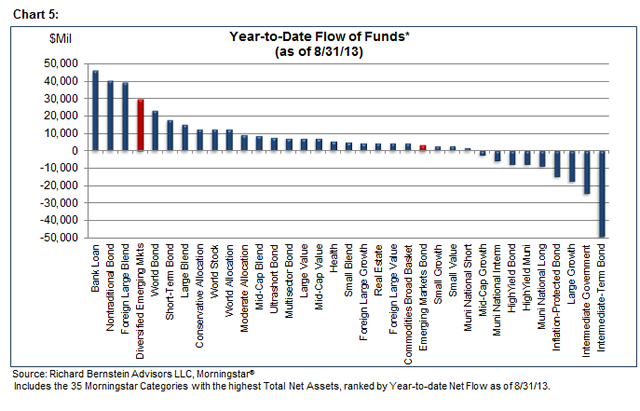

Mutual fund flows suggest that investors still do not believe the US growth story.Rather, they continue to invest heavily in emerging market equities as shown on Chart 5.To us, this seems very similar to the early-2000s when investors were waiting for technology shares to lead the market, and ignored the opportunities in emerging markets, gold, commodities, real estate, etc.

Our bullishness regarding US equities has lasted for more than four years, and we see little to dissuade us from our current position.Admittedly, equities are not as attractive as they were four years ago, but the standard warning signs that typically suggest a higher probability of a bear market are nowhere to be seen.We’ll likely change our tune when the yield curve inverts, when investors are certain and valuations are rich, or when US equities are widely considered to be core holdings.None of those characteristics are true today in the US.

In the emerging markets, however, inflation is high and some yield curves are inverted or close to inverting.Valuations seem quite rich to us when one takes into account these countries’ inflation rates.Fund flows suggest that investors still consider emerging markets the world’s best growth story.It’s that last point we are particularly worried about.Emerging markets are the growth story that isn’t.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends.An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results.Indices are not actively managed and investors cannot invest directly in the indices.

US Large Cap:Standard & Poor’s (S&P) 500®Index.The S&P 500®Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

US Mid Cap: Standard and Poor'sMidCap 400®Index:The S&PMidCap 400® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the mid-sized companies of the U.S. stock market

US Small Cap: Standard and Poor'sSmallCap 600®Index:The S&PSmallcap 600® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the small cap segment of the U.S. stock market.

World:MSCI All Country World Index (ACWI®).The MSCI ACWI®is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of global developed and emerging markets.

EM: MSCI Emerging Markets (EM) Index.The MSCI EM Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of emerging markets.

BRIC: MSCI BRIC Index.The MSCI BRIC Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of Brazil, Russia, India and China.

EM Europe: MSCI Emerging EuropeIndex.The MSCI EM Europe Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of emerging markets in Europe.

MSCI Japan: MSCI Japan Index.The MSCI Japan Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of Japan.

Private Equity:The Cambridge Associates LLC U.S. Private Equity Index®is an end-to-end calculation based on data compiled from 1,052 U.S. private equity funds (buyout, growth equity, private equity energy and mezzanine funds), including fully liquidated partnerships, formed between 1986 and 2013. Pooled end-to-end return, net of fees, expenses, and carried interest. Historic quarterly returns are updated in each year-end report to adjust for changes in the index sample.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

© Richard Bernstein Advisors