Shakespearean plays follow a pattern.The underlying plots and storylines change from play to play, but the five-act construction is a common overlap.One should expect an introduction to the characters in Act I, the climax in Act III, and resolution in Act V.

Market cycles tend to follow a similar pattern cycle after cycle.Like the different plots in various Shakespearean plays, the catalysts that begin and end each cycle, and the events during the cycle are always different.However, market cycles seem to follow a script and, so far, this cycle seems to be following the script almost perfectly.

Investors seem to believe that market cycles no longer exist.2008’s near-collapse of the financial system and the associated bear market scared both institutional and individual investors so much that they can’t believe something normal might come out of something so horrible.A unique and horrible event, like 2008, must lead to a unique outcome, no?

Since March 2009, though, the bull market has followed the typical market cycle script.In an almost uncanny fashion, observers during this cycle are even using some of the same phrases used during past cycles to describe the current cycle.

Cycles are not about absolutes

Economists and politicians worry about the absolutes of good or bad.Investors, however, must worry about better or worse.Cycles are about better or worse.They tend to start from depressed levels of growth, improve, strengthen, expand, then deflate back to depressed levels.

Economists often debate whether a country will have a “hard landing” (meaning recession) or a “soft landing” (meaning a slowdown in growth without a recession).We have often argued that the adjective “hard” or “soft” is meaningless.The market simply cares that a country’s growth is landing.

The US economy certainly isn’t strong on an absolute basis, but it does continue to improve through time.High-frequency data may hide that gradual improvement, but the US economy has indeed improved.Is the US economy a jet taking off or is it a slow single-engine plane?The market doesn’t care about the aircraft, but rather simply cares that the economy is experiencing lift-off.

The early cycle

The early cycle is typically the best time to invest, but investors are typically too scared from their poor portfolio returns during the prior recession to consider investing.The early cycle tends to present the best opportunities because monetary and fiscal policies typically focus on stimulating the economy, valuations are depressed, and fundamentals tend to improve.Financials and Consumer Cyclicals are the typical leadership sectors during the early cycle phase because they are the most sensitive to lower interest rates and credit creation.

During this period, investors tend to ignore the improvement in the economy and focus more on the gap between weak current statistics and the previous cycle’s extremes.It is common for investors to worry whether the economy and stock market will ever return to where it was prior to the recession.

History suggests that the early cycle should be viewed as a period of investment opportunity, but fear tends to dominate investors’ emotions.This cycle has been quite similar.Institutional investors have rushed to hedge funds that offer downside protection and that hedge “tail risk”.Individual investors have fled stocks in search of income in the bond market.Meanwhile, the S&P 500® has had a compound annual return over 21% (from 3/31/09 to 10/31/13).

Mid-cycle

The middle portion of the cycle is a bit more challenging.Whereas the early cycle was dominated by fiscal and monetary stimulus, the mid-cycle becomes more of a tug-of-war between rising interest rates and improving fundamentals.The Fed begins to sense that the extreme monetary stimulus of the early-cycle period is no longer needed, and investors begin to worry whether the economy and the stock market can survive without the Fed’s support.

Mid-cycle performance tends to be dominated by capital spending-oriented stocks like Industrials and Technology.As the mid-cycle progresses, inventories that were built up during the recession are fully depleted and companies begin to invest.Admittedly, we have questioned whether there will be a normal capital spending cycle or whether merger and acquisition activity will pick up as larger companies rush to buy growth rather than build it.

The market may be entering the mid-cycle.Investors are indeed worried about the Fed’s “taper” of monetary policy, and some believe that the only reason the stock market has appreciated is because of the Fed’s stimulus.These are common fears for the early-portion of the mid-cycle.At the same time, investors’ hesitancy to invest tends to dissipate, and that is happening as well.

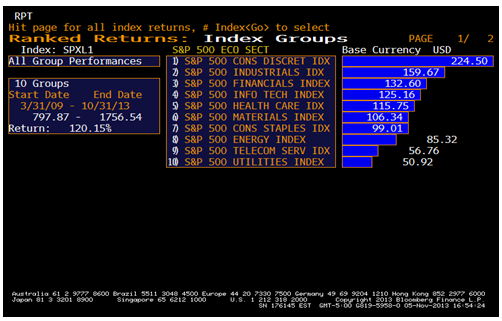

Chart 1 demonstrates that the current market cycle does appear to be dominated by the performance of early- and mid-cycle sectors.The best performing sectors since March 2009 have been Consumer Discretionary and Financials (early cycle sectors) and Industrials and Technology (mid-cycle sectors).

Chart 1:

Source: BloombergFor Index descriptors, see "Index Descriptions" at end of document.

Late-cycle

The late cycle is characterized by a vigorous economy and strong profits that investors believe will never end.Inflation tends to pick up, and that forces the Fed to try to win the tug-of-war between rising rates and improving fundamentals.It has historically been a sign that the Fed won the battle when the yield curve inverts.

Despite the warning signals of an inverted yield curve and waning profits growth, investors believe that “this time is different” and often ignore the warnings.For example, the yield curve inverted in late-2006/2007, but bulls argued at the time that the curve was inverting only because of“technical reasons”, and that the historical warning sign didn’t apply.

This part of the cycle seems to be far off in the future.The economy is hardly robust enough to generate worrisome inflation, and the yield curve remains extraordinarily steep.Late-cycle sectors, such as Energy and Materials, continue to largely underperform.

Recession

History suggests that it is only a matter of time before the next recession once the Fed wins the tug-of-war between rising rates and fundamentals.During recessions, defensive sectors perform the best: Consumer Staples, Health Care, Telecom, and Utilities.These were indeed the leaders during the 2008 recession.

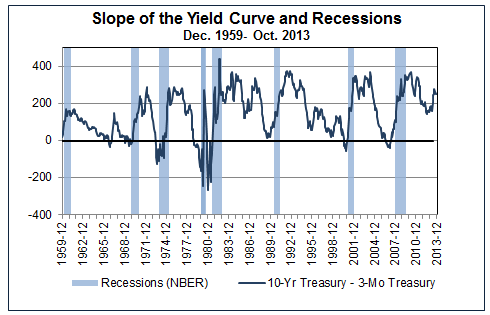

It seems terribly premature to worry about the next recession when the Fed is still erring on the side of stimulus, when the yield curve is extremely steep as Chart 2 highlights, and valuations and sentiment remain generally favorable.

Chart 2:

Source: Richard Bernstein Advisors LLC., National Bureau of Economic Research (NBER), FederalReserve Board, Bloomberg

Read the script

If someone suggests “this time is different” and the person is bullish, people think the speaker to be foolish.However, if someone suggests “this time is different” and the person is bearish, people think the speaker to be very insightful.

The reality is that cycles follow a script.It’s never different.The characters and the story changes, but there are always five acts in a Shakespearean drama.There has always been an early-cycle, a mid-cycle, and a late-cycle that preceded a bear market and a recession.

If we are correct, and the market is entering the mid-cycle, then it likely isn’t yet intermission during the show.

We continue to believe that the stock market is experiencing one of the biggest bull markets of our careers.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends.An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results.Indices are not actively managed and investors cannot invest directly in the indices.

S&P 500®:Standard & Poor’s (S&P) 500®Index.The S&P 500®Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

S&P 500®Sector/Industries:Sector/industry references in this report are in accordance with the Global Industry Classification Standard (GICS®) developed by MSCIBarraand Standard & Poor’s. The GICS structure consists of 10 sectors, 24 industry groups, 68 industries and 154 sub-industries.

© Copyright 2013 Richard Bernstein Advisors LLC. All rights reserved.

The views expressed are those of Richard Bernstein Advisors LLC, not necessarily those of UBS or any of its affiliates, and may in some cases be different from, or inconsistent with, views expressed or taken by UBS.Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in, any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Specifically, and without limiting the generality of the foregoing, before acquiring the shares of any mutual fund, it is your responsibility to read the fund’s prospectus. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is an inherently risky activity, and investors must always be prepared to potentially lose some or all of an investment's value. Past performance is, of course, no guarantee of future results.