Seven Reasons Why Industrial Commodity Prices are Headed Higher

Between December 2008 and April 2011 commodity prices, as reflected by the CRB Spot Raw Industrials, doubled. In the ensuing 2-years they have retraced 20% of that rally but are now showing signs of wanting to head higher. In the interest of fair disclosure our commodity model went bullish just under a year ago but prices remained range bound instead of experiencing their normal strength. So what’s so different now that makes us bullish on commodities? Here are seven reasons.

Chart 1 Commodity Prices and the Global Economy

1. Commodity prices are very much influenced by the level of global economic activity, which acts as a proxy on the demand side. The shaded areas in Chart 1, for instance, show that when the OECD (normalized) Composite Leading Indicator is rising commodity prices typically move higher. The red dashed arrows show the few exceptions to this rule. So far the latest rally in global business activity has not fed back into to higher commodity prices, but as long as this indicator continues to advance upward pressure on commodity prices will continue to grow.

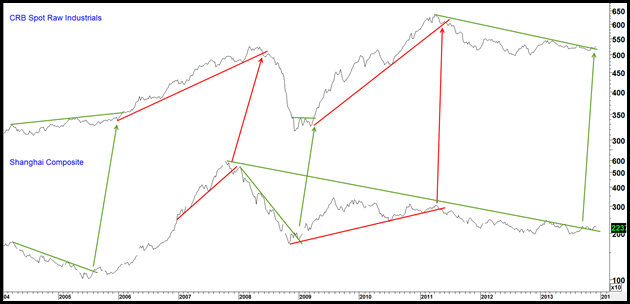

Chart 2 The Chinese Stock Market versus US Dollar Based Industrial Commodity Prices

2. It is a well-known fact that the Chinese economy is a major source of commodity demand. We also know that equity markets have a strong tendency to lead business activity. Bearing that in mind, Chart 2 compares the Shanghai Index with the CRB Spot Raw Industrials. Whenever it’s been possible to observe joint trendline violations such action has reliably signaled an important reversal in trend for both series. Note that in most cases the Shanghai Index leads the CRB Spot Raw Industrials. Late November witnessed another set of joint breakouts, as two key down trendlines were successfully assaulted on the upside. If past is prolog these signals are most likely a forerunner of higher commodity prices come 2014.

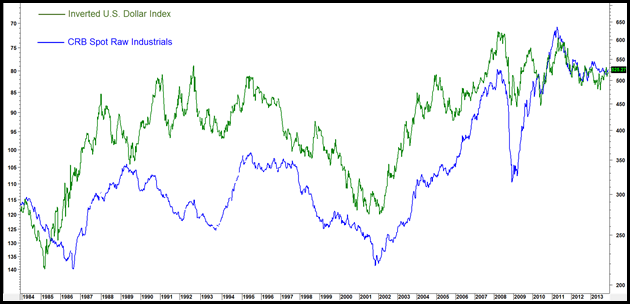

Chart 3 The Inverted US Dollar Index versus The CRB Spot Raw Industrials

3. Commodity prices usually move in the opposite direction to the dollar. Chart 3 compares an inversely plotted Dollar Index to the commodity series for the last couple of decades. It’s certainly not a tick by tick relationship. Nevertheless, the correlation is strong enough that a rising dollar provides a strong headwind for commodity prices and vice versa.

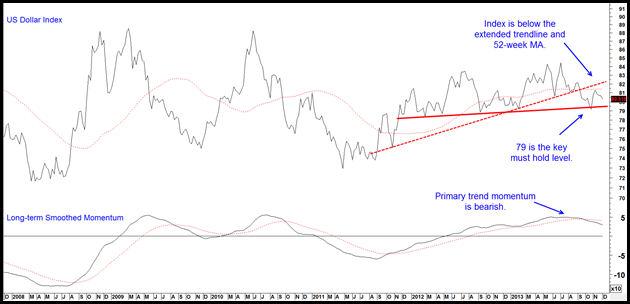

Chart 4 US Dollar Index and Long-term Smoothed Momentum

Chart 4 shows that the Dollar Index recently violated an important up trendline and its long-term smoothed momentum began to roll over. That suggests that the Index will move lower in the period ahead. The really important juncture point lies at the thick red line at 79. If that is breeched in a decisive way we would expect to see a substantially lower dollar and, presumably, the higher commodity prices that typically go with it.

Chart 5 Inflation Protected versus Regular Bonds Compared to Commodity Prices

4. The bond market also has an opinion concerning inflation and that’s expressed by the preference of market participants between inflation protected and regular bonds. This relationship is represented by the ratio between the Barclays Inflation Protected Treasury ETF, the TIP and regular long-term bonds in the form of the Barclays 20-year Trust, the TLT. The arrows in Chart 5 show that broad movements in this series track those of the CRB Composite. Several weeks ago the bond market cast its vote for higher commodity inflation by breaking above a major trading range. Note that its long-term smoothed momentum is in a positive (for inflation) trajectory.

Chart 6 A Stock Market Inflation/Deflation Ratio versus Commodity Prices

5. Not to be left out, the stock market also has an opinion. It’s expressed again between two ETF’s, the inflation bet reflected by the Goldman Sachs Natural Resource ETF, the IGE, and the deflationary one represented by the Spider Consumer Staples, the XLP. This relationship is again compared to a commodity series, this time the Dow Jones UBS Commodity ETN, the DJP. Recently the ratio violated a major down trendline and its momentum has moved decisively to the upside, two conditions that have traditionally been associated with rising commodity prices.

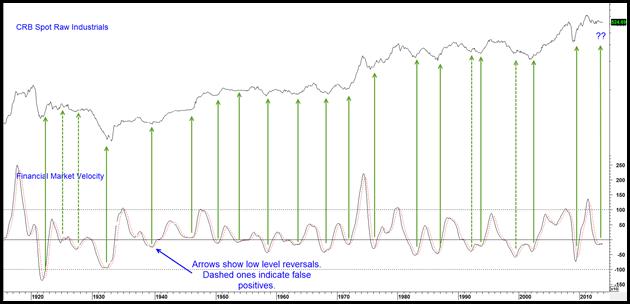

Chart 7 CRB Spot Raw Industrials versus a Financial Market Velocity Indicator

6. That’s also the outlook suggested by Chart 7, which compares US Industrial commodity prices with a momentum measure constructed from the three financial markets, bonds, stocks and commodities. The arrows point up low level upside reversals. The solid ones indicate successful signals and the four dashed ones false positives. It looks as though the indicator has bottomed for the current cycle and is now in a position to accelerate to the upside. Close to one hundred years of commodity history suggests that, if that proves to be the case, commodity prices will experience some form of primary trend advance.

7. Sentiment is also constructive for commodity prices. It’s often observed that major institutional commodity players exit or cut back on departments when things go sour. From a contrary point of view such thin reed indicators represent a positive backdrop. In that respect Bloomberg recently reported that JPMorgan Chase & Co., the biggest U.S. lender by assets, is seeking to sell its physical commodity business. Bloomberg also reported in early December that Deutsche Bank AG is in the process of exiting dedicated energy, agriculture, dry bulk and base metals trading. We can’t say that commitment of traders and sentiment indicators for commodities are universally bullish for commodities. However, current readings from this data show that the attitude of market participants is certainly not inconsistent with a major price low. Bank of America’s Merrill Lynch's recent survey of global managers sums it all up, as they report that commodity allocations by these managers has slumped close to a decade low. That takes us back near to the start of the secular bull market, not a bad place to be if you want to get bullish on commodities!

Martin J Pring

© Pring Turner Capital Group