Market share: the next secular investment theme

It is well known that corporate profit margins are at record highs.US margins, developed market margins, and even emerging market margins are generally either at or close to record highs.Most bearish market observers cite the inevitability of margins contracting as a prime reason for caution.

We don’t dispute that the probabilities favor margin contraction.It seems reasonable to forecast margin contraction given the combination of a stable-to-stronger US dollar and growing political pressures to better reward labor.However, the expansion or contraction of profit margins has historically had a relatively weak relationship with the direction of the stock market.

A myopic focus on profit margins may miss an important investment consideration.Whereas most investors remain fearful of margin compression, we prefer to search for an investment theme that could emerge if margins do indeed compress.

Market share

Basic economics states that profits are not solely a function of margins, but also of the number of units sold.Companies often fight for market share (i.e., a greater number of units sold) when margins contract.Accordingly, our investment focus has shifted toward themes based on companies who might gain market share.

Our major secular positions are all market share stories: American Industrial Renaissance, Japan, and small US banks are just three examples.

American Industrial Renaissance

Small and mid-cap US-focused industrial and manufacturing companies are gaining market share.There are many factors contributing to this shift:

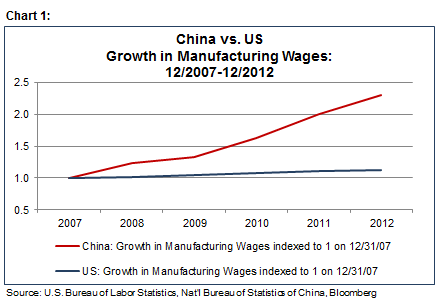

Currency wars: emerging markets lose market share

In our recent year-ahead report “10 for ‘14”, we mentioned the increasing probability of currency wars.The global credit bubble has left the global economy with significant overcapacity, and production in many parts of the world is becoming a commodity.Commodities tend to compete on price.

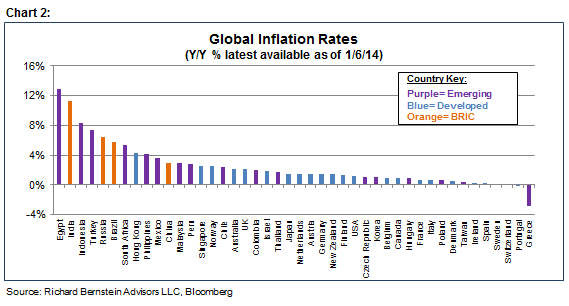

Productivity is critical to compete globally, and many emerging markets offered manufacturers greater profitability through productivity.However, productivity growth is now slowing meaningfully in most emerging markets, and the emerging markets now have the highest inflation rates in the world (see Chart 2).

When productivity fails to be a competitive advantage, then countries have to compete purely on price and devalue their currencies.Devaluing a currency often results in higher inflation rates because the prices of imported goods, both input raw materials and consumer goods, go up.Emerging markets’ current high inflation rates will likely limit emerging market countries’ exchange rate flexibility.Some EM countries are already starting to lose market share as a result.

We strongly doubt that the idea of market share has been factored into forecasts for emerging market economic or profits growth.Despite that the emerging markets have been leading the world in negative earnings surprises for nearly two years, growth forecasts have been remarkably downward sticky.

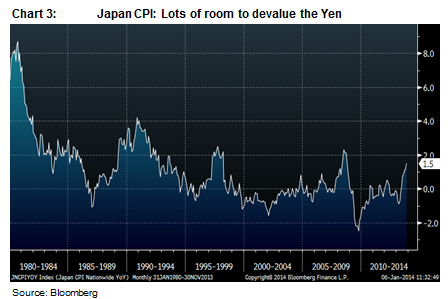

Japan – “blessed” with deflation

Our interest in Japan is based on the country’s new-found competitive advantage versus the emerging markets.Whereas the emerging markets have among the highest inflation rates in the world, deflation has been the dominant theme within the Japanese economy.Because the Japanese economy is in need of some inflation, Japan seems to have plenty of flexibility to manage a lower exchange rate without risking abnormally high inflation.

Japan’s productivity growth, like most of the world’s, has been slowing, and the Japanese government has decided to depreciate the Yen as a result.We think the odds are that Japanese manufacturing will gain market share because Japan has the flexibility to manage a lower exchange rate and Japanese production will become more competitive.

This competitive advantage is unlikely to occur quickly.Rather, we see Japan gaining market share as a secular investment theme, and not one that is likely to occur quickly in a matter of months.

Small US banks

The history of bubbles shows that bubbles create capacity that is typically not needed after the bubble deflates.For example, the California gold rush in the 1800s created many towns that became ghost towns once the gold rush subsided.Some have suggested that the recent increase in North Dakota’s population as a result of the shale boom is oddly similar to that of the California gold rush.

Capacity expansion during a credit bubble is not physical capacity as it would be during a bubble in the real economy.Rather, the expansion of capacity during a credit bubble is represented by the expansion of bank balance sheets, i.e., banks’ increased ability to lend.We have argued for many years that the history of post-bubble overcapacity meant that bank balance sheets would inevitably shrink as the credit bubble subsided.

Larger banks around the world have tried to fight the rationalization of balance sheet capacity.The arguments against increased regulation and against stricter capital requirements are attempts by the banks to delay the inevitable downsizing of their balance sheets.

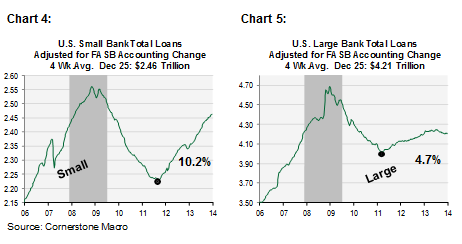

Smaller US banks, however, have already re-sized their balance sheets and are gaining market share as a result.Whereas large bank lending in the US is contracting, smaller bank lending is accelerating (See Charts4 & 5 below, courtesy of Cornerstone Macro).Growth expectations for larger banks still seem overly optimistic, whereas those for smaller banks may be too conservative.

Market share is the story

Concerns regarding profit margin contraction might be well founded.The key question for us is not whether they will contract or not, but rather how should one invest if they do.We think that market share, rather than profit margins, will be a major investment theme over the next several years.

Our portfolios are positioned accordingly.

© Copyright 2014 Richard Bernstein Advisors LLC. All rights reserved.

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in, any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Specifically, and without limiting the generality of the foregoing, before acquiring the shares of any mutual fund, it is your responsibility to read the fund’s prospectus. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is an inherently risky activity, and investors must always be prepared to potentially lose some or all of an investment's value. Past performance is, of course, no guarantee of future results.

© Richard Bernstein Advisors