We first wrote about the “American Industrial Renaissance” in 2012, and it remains one of our favorite investment themes. We continue to implement this theme through small US-centric industrial companies and small financial institutions that lend to public and private industrial firms.

It remains unlikely that the United States will be the manufacturing powerhouse that it was during the 1950s and 1960s, but many factors are suggesting that the US industrial sector will continue to gain market share.

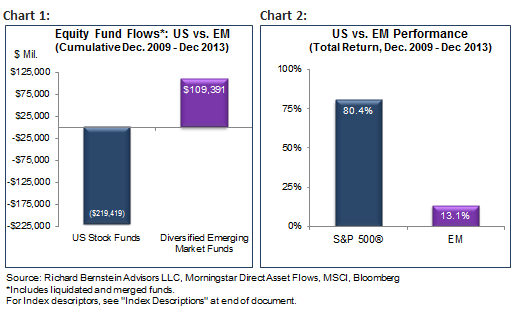

Investors have been slow to adapt to the global sea change. Global growth has slowed more than investors had previously anticipated and political risk has risen; yet over the past four years flows into emerging markets funds have remained very strong despite their underperformance. (see charts 1 and 2).

More recently, investors have apparently begun to recognize the economic and political headwinds facing companies that operate within the emerging markets. In 2013, US equity funds had an annual inflow for the first time in a number of years, but also had slightly stronger inflows than did EM equity funds.

Because of the lack of sustained interest in US stocks, the American Industrial Renaissance investment theme appears to still be in its early stages. While recognition of this theme has begun to grow, it has not yet become mainstream.

There are many reasons why the US manufacturing sector seems likely to gain market share. Our three main reasons remain wages and productivity, energy costs, and political stability.

Wages and Productivity

Markets do not value assets on the absolutes of good or bad. Rather, markets price on whether fundamentals are getting better or worse. Investors, therefore, should generally ignore analyses that don’t highlight measures of marginal improvement or deterioration.

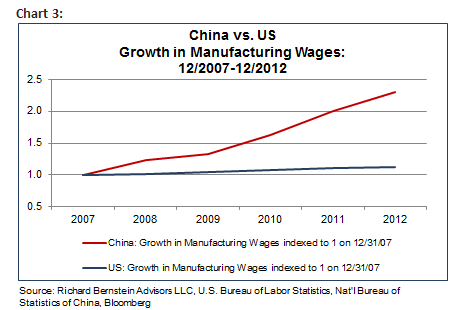

With that in mind, wages within the US industrial sector seem to be increasingly competitive. For example, manufacturing wages in China increased 18% per year over the 5 years from December 2007 through Dec. 2012, whereas US manufacturing wages rose 2.3% per year (see Chart 3).

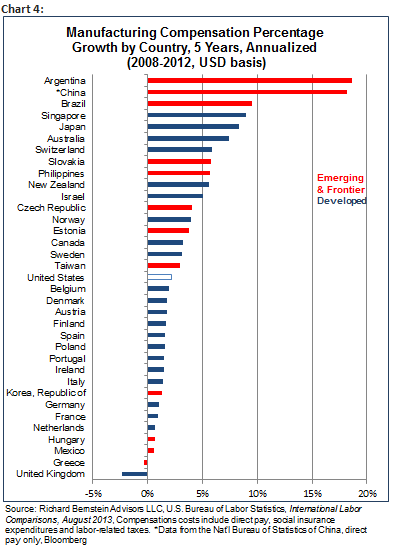

US manufacturing wage growth has not only lagged Chinese wage growth, it has lagged wage growth in much of the world. Chart 4 compares the compound wage growth for five years (2008 through 2012) for a broad range of countries. US wage growth remains tepid particularly in comparison to countries in Asia and Latin America, whose comparative wage advantage continues to decline.

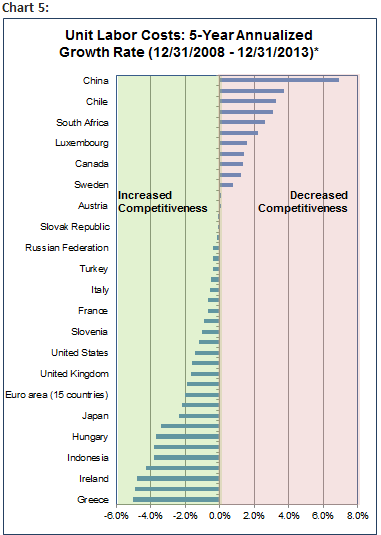

Unit Labor Costs are the link between productivity and the cost of labor. When unit labor costs are rising, wages are increasing faster than productivity, which suggests decreased competiveness. Conversely, when unit labor costs are falling, productivity is rising faster than wages, which suggests increased competitiveness.

China’s global competitiveness has begun to deteriorate on this measure. Chart 5 below highlights that despite its well-known productivity growth, unit labor costs are on the rise as wage growth has outpaced that of productivity.

Source: Richard Bernstein Advisors LLC, OECD Economic Outlook Database, Competitiveness Indices, *2013 final data is estimated.

Energy Costs

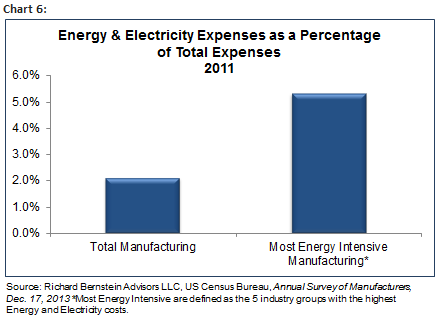

Energy is not as large of a factor input to manufacturing as many might expect. Chart 6 highlights that energy costs are generally less than 6% of total expenses for US manufacturers.

Materials costs are the most significant expense for manufacturing. Commodities are generally denominated in US dollars, and the fall in many emerging market currencies has accordingly further increased input costs to manufacturers in these countries.

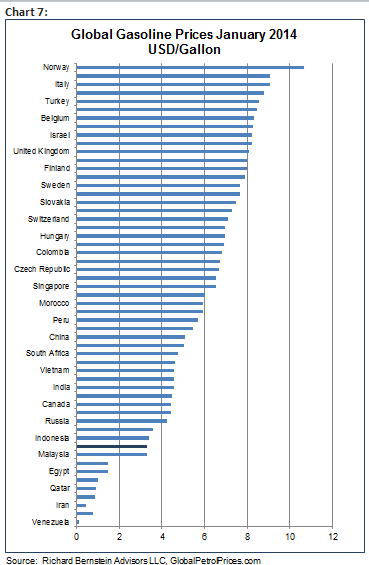

Energy is a more significant component of supply chain and distribution costs, and in this respect the United States is also becoming increasingly competitive. The following chart, shows gasoline costs around the world. Middle East countries have relatively cheaper gasoline prices, but gasoline in the US is inexpensive relative to its cost in most countries outside of the Middle East. US gasoline is cheaper than is gasoline in most of the major emerging market manufacturing countries like China, Brazil, India, and South Korea.

Political Stability

Academic studies have cited various relationships between economic growth and political stability. Governments tend to be more stable when an economy is healthy, but significant deterioration in economic growth can increase political risk. Countries sometimes resent when foreigners’ local operations are profitable while the domestic economy suffers. When this occurs, politicians sometimes take drastic actions, such as nationalizing foreign companies’ facilities, to appear as though they are rectifying their domestic economy’s problems.

Egypt’s coup was an extreme case, but an increasing number of emerging markets are experiencing some increased level of civil unrest. Political uncertainty appears to be increasing, and companies seem to be considering such risks when locating manufacturing plants.

Geopolitical and geo-economic risks, in general, may become a larger consideration for companies searching for locations for new plant and equipment. The US is an extremely safe place for corporations to do business.

The American Industrial Renaissance – a secular theme

The US is unlikely to be the industrial leader that it was in the 1950s and 1960s. However, it seems very likely that the US industrial sector will continue to gain global market share over the next decade. Narrowing wage differentials, lower energy and logistical costs, and political stability are just some of the factors that investors should consider.

We continue to believe that investors are over-estimating the risks within the United States and under-estimating the risks in the emerging markets. If we are correct in that assessment, then the American Industrial Renaissance could be an investment theme for many years.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

S&P 500® : Standard & Poor’s (S&P) 500® Index. The S&P 500® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

EM: MSCI Emerging Markets (EM) Index. The MSCI EM Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of emerging markets.

Unit labor costs: OECD Economic outlook database. Unit labour costs measure the average cost of labour per unit of output. They are calculated as the ratio of total labour costs to real output, or equivalently, as the ratio of mean labour costs per hour to labour productivity (output per hour. The OECD System of Unit Labour Cost Indicators compiles annual and quarterly ULC and related indicators according to a specific methodology to ensure data are comparable across countries. This system is principally based on national accounts concepts and data, but also brings together a wide range of proxy sources for quarterly data.

© Copyright 2014 Richard Bernstein Advisors LLC. All rights reserved.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in, any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Specifically, and without limiting the generality of the foregoing, before acquiring the shares of any mutual fund, it is your responsibility to read the fund’s prospectus. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is an inherently risky activity, and investors must always be prepared to potentially lose some or all of an investment's value. Past performance is, of course, no guarantee of future results.