2008’s bear market has led investors to increasingly focus on absolute returns rather than relative returns. However, investors continue to judge manager performance based on relative performance despite the change in their performance goals. That seems inconsistent and self-defeating to us.

A manager might have outperformed his or her benchmark by several hundred basis points, but that relative outperformance is somewhat meaningless if the manager’s benchmark was down 20% or more. Outperforming one’s benchmark is, of course, quite admirable, but investment goals cannot be achieved based on relative performance. Relative performance does not help an endowment build a new science building and fund research, or parents who want to grow savings for their child’s future college expenses.

The two main drivers of equity returns are commonly called “alpha” (a measure of a manager’s relative performance versus a benchmark stock index) and “beta” (a measure of a portfolio’s sensitivity to the movements of the overall stock market). Because all stocks are part of the stock market, beta is the primary driver of equity returns. Alpha may be the icing on the cake, but beta is the cake itself.

Investors tend to choose funds based on alpha but, as mentioned, it seems odd to us that investors would pick funds based on relative performance when their investment goal is actually absolute performance. Investors interested in absolute returns should focus more on beta, which is an absolute performance concept.

Our strategies focus on managing beta through a market cycle, rather than on alpha. High beta investments are likely to outperform the overall market during bull markets, but are also likely to underperform the market during bear markets. Our goal, therefore, is to be more aggressive during bull markets (i.e., our portfolios will tend to have a higher beta), and more conservative during bear markets (i.e., our portfolio beta will tend to be lower). Rather than picking individual stocks (the icing on the cake), we try to focus on allocating beta effectively among the primary factors of stock returns such as size, style, geography, and economic sector.

Style boxes give a false sense of security

The introduction of investment style boxes (large growth, large value, small growth, small value, etc.) seems to have been a mixed blessing. On the one hand, style-box analyses allow investors to better compare the skills of a particular manager relative to other managers with similar investment philosophies (alpha). However, style boxes effectively limit beta and remove managers’ ability to manage for absolute returns across styles.

It has been generally thought that constraining a manager to a particular style box while at the same time managing one’s own equity allocation (i.e., beta management) was a better combination than was allowing managers the freedom to roam from style to style looking for opportunities. This theory increasingly looks flawed to us.

The general perception that there has been a “lost decade” of poor equity returns seems to starkly demonstrate that investors have managed beta poorly. Overall global equity returns have not suffered during the past decade, and buy-and-hold strategies certainly are not dead. At the beginning of the decade of the 2000s, investors were encouraged to invest in technology shares by the excitement of the technology bubble, and in S&P 500® index funds by the “insight” that stocks outperformed over the long-term and that index funds were the most cost-efficient way to obtain those returns. As it turned out, at the end of the decade, the technology-laden NASDAQ Composite’s ten-year annualized total return was -5%, and the S&P 500®’s was -1%.

One’s portfolio would have performed quite well, though, if one had bought and held emerging-market stocks, energy stocks, gold stocks, and many other segments of the global equity markets. “Buy and hold” wasn’t dead. Rather, investors needed to realize that the success of buy-and-hold strategies largely depends on buying and holding the correct securities.

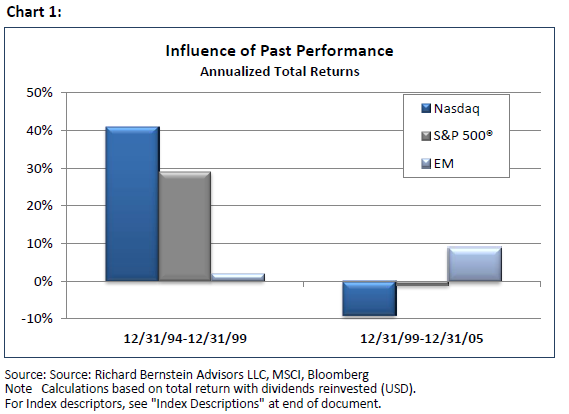

Most investors are quite familiar with the disclaimer that “past performance is not necessarily indicative of future returns”, yet investors’ allocations continue to be heavily influenced by past performance. Chart 1 gives some insight as to how past performance influenced investors to favor technology stocks and S&P 500® index funds at the beginning of the “lost decade”. Investors generally thought that emerging-market stocks were too risky because of events like the “Asian crisis” and the “Russian crisis” which dominated the headlines of the late 1990s.

Volatility signals a change in leadership

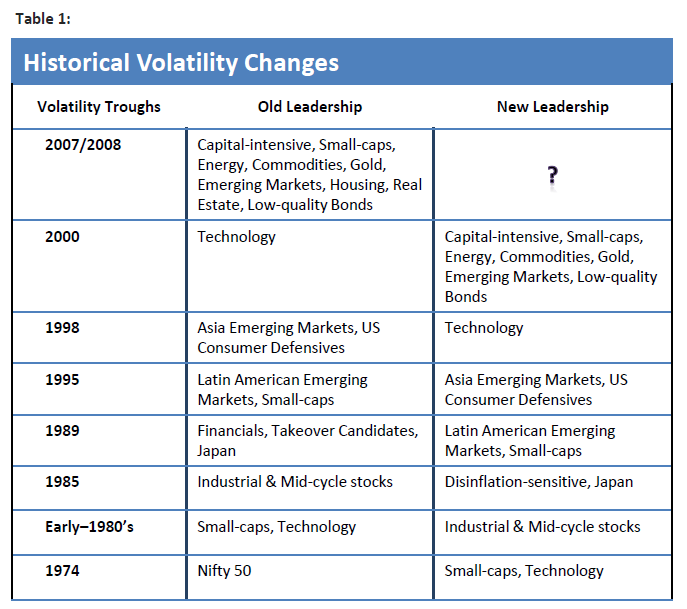

Historically, periods of extreme equity-market volatility have consistently signaled a change in market leadership. The growth stories going into a period of volatility are rarely, if ever, the growth stories coming out.

Volatility occurs because of a change in the underlying economy. The old growth stories were geared to the previous economic environment, and volatility occurs because those leaders are no longer appropriate for the newer economic conditions. New growth stories begin to emerge. Table 1 shows this historical effect.

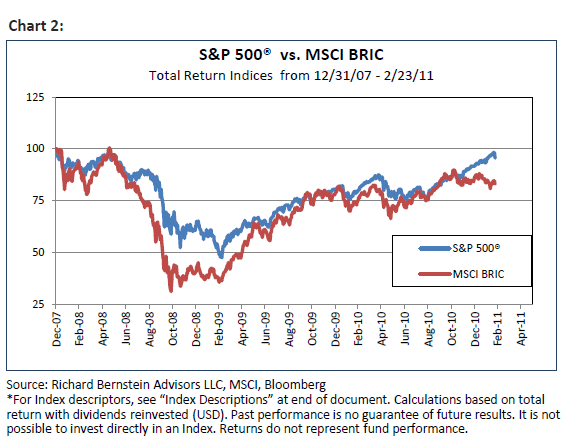

The current cycle has so far fit that historical precedent. 2008’s dramatic market volatility has signaled a change in leadership, although few investors seem to realize that a change is underway. As Chart 2 highlights, the S&P 500® has now outperformed the BRIC markets (Brazil, Russia, India, and China) for more than three years! Leadership again appears to be changing.

Fund flows appear backward-looking

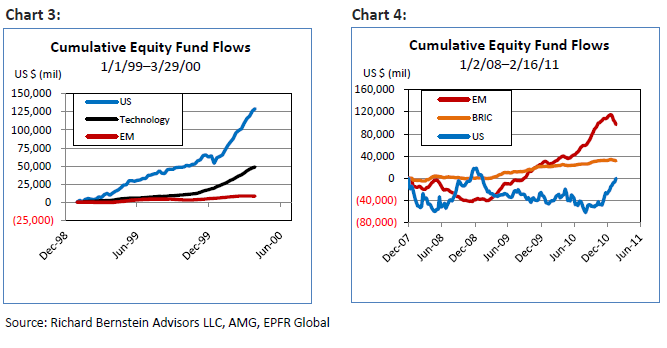

In 1999/2000, flows into technology funds eclipsed those into EM and international funds just as the technology bubble neared its peak, as shown in Chart 3. Fund flows today appear to be mimicking those of 1999/2000 with respect to EM as shown in Chart 4. In fact, recent EM flows have been larger than those into dedicated tech funds in 1999/2000.

Investors seem to be making the same mistake they made ten years ago by looking backward at old growth stories and expecting those investment themes to perpetuate into the future. Another period of poor beta management might be upon us.

Why hedge funds??

We find it particularly odd that investors have increasingly restricted their equity managers to style boxes and relative returns, but are willing to pay higher fees to hedge funds to focus on absolute returns. This makes little sense to us.

Instead of paying lower fees and giving long-only managers the flexibility to roam, investors are paying higher fees to hedge fund managers. Even odder, 2008 clearly demonstrated that hedge fund managers generally haven’t shown any more skill at managing beta and absolute returns than have long-only managers given the latters’ constraints. Rather than paying exorbitant fees for dubious skill, it makes more sense to us to remove style box constraints, pay lower fees, and allow traditional equity managers the flexibility to manage beta.

The importance of beta management

We feel it may be time to return to the past, when style boxes were used for analysis and not for constraint. Those limitations have not generally led to better overall portfolio performance for investors, have distortedly focused investors’ attention on relative returns rather than on absolute returns, and have led investors to less transparent, less liquid, and more expensive hedge funds in search of the absolute returns that style boxes specifically attempt to constrain.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

S&P 500® : Standard & Poor’s (S&P) 500® Index. The S&P 500® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

EM: MSCI Emerging Markets (EM) Index. The MSCI EM Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of emerging markets.

BRIC: MSCI BRIC Index. The MSCI BRIC Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of the following four emerging-market country indices: Brazil, Russia, India and China.

Nasdaq: NASDAQ Composite Index. The NASDAQ Composite Index is a broad-based, market-capitalization-weighted index of all common stocks and similar securities (e.g., ADRs) listed on the NASDAQ stock market, including those of both US and non-US companies.

© Copyright 2014 Richard Bernstein Advisors LLC. All rights reserved.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in, any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Specifically, and without limiting the generality of the foregoing, before acquiring the shares of any mutual fund, it is your responsibility to read the fund’s prospectus. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is an inherently risky activity, and investors must always be prepared to potentially lose some or all of an investment's value. Past performance is, of course, no guarantee of future results.

About Richard Bernstein Advisors:

Richard Bernstein Advisors LLC is an independent investment adviser. RBA partners with several firms including Eaton Vance Corporation, First Trust Portfolios LP, and BNP Paribas, and currently has $2.7 billion collectively under management and advisement as of February 28, 2014. RBA acts as sub‐advisor for the Eaton Vance Richard Bernstein Equity Strategy Fund and the Eaton Vance Richard Bernstein All‐Asset Strategy Fund and also offers income and unique theme‐oriented unit trusts through First Trust. Additionally, RBA runs ETF asset allocation SMA portfolios at UBS and Merrill Lynch and on select RIA platforms.