No matter where we invest, there’s always some sort of risk. This includes not only geopolitical or macroeconomic factors in a given country, but also issues that are unique to a specific sector or individual security. As bottom-up stock pickers, my team and I must assess the potential risks and returns related to each and every company we invest in. One area that warrants closer examination is environmental, social, and governance (ESG) risks and opportunities, which can play a big role in our stock selection and valuation process.

As part of our research process, the Templeton Emerging Markets Group evaluates a company’s market opportunity, competitive position, management strength, financial profitability and valuation. ESG issues can influence several of these factors. ESG does not typically incorporate strict screens that would automatically exclude any particular investment. Issues are considered if and when they impact the risk and return profile of an investment opportunity, similar to other company or industry investment considerations such as future growth prospects and market demand.

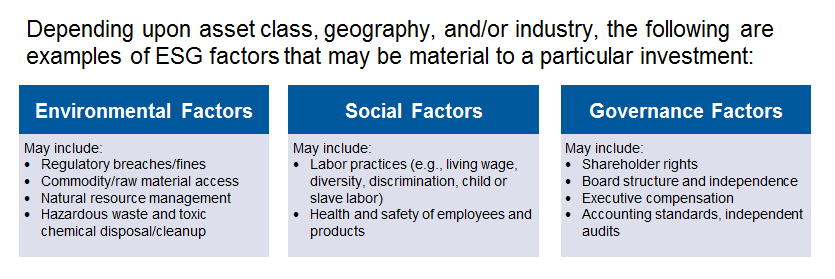

What might these ESG issues be? They might include natural resource scarcity, hazardous waste disposal, product safety, employee health and safety practices, or shareholder rights, to name a few.

Some of the overall aspects we evaluate when analyzing individual companies include quality of company management, corporate governance, competitive position relative to peers, ownership structure and commitment to creating shareholder value. These dovetail with ESG factors. Our analysts typically conduct some 2,500 to 3,000 research meetings every year, meeting with company management, touring facilities, and meeting suppliers, clients and competitors. These meetings allow us to look at a company from many different perspectives and provide both broader and more detailed information across many factors (including ESG) which may otherwise not be captured.

In emerging markets, regulation and enforcement of issues pertaining to corruption, corporate governance, the environment and other social issues may be still evolving. However, as a country develops, generally these safeguards tend to become both more comprehensive and more stringently enforced. Thus, we believe companies with strong records of governance today (which can impact management of environmental and social issues) may be better prepared for the future, and thus, may provide a better investment case. For example, in our view, a company with inadequate environmental policies not only reflects badly on existing corporate governance, it may also bode poorly for the future competitiveness of that company.

Given the importance of corporate governance in evaluating investment opportunities, one of the key aspects we look for in company management is a strong culture and history of ethical business conduct. We conduct analyses of ownership structures, the management team’s track record, the company’s corporate governance history and its commitment to creating shareholder value. Additionally, we look for managers who know the business well, with experience in a given field, who are properly motivated through incentives such as stock options on company shares. We also pay attention to management’s ability to cope with a rapidly changing business environment. For example, in Thailand during the mid-to-late 1990s, when markets crashed and investor confidence was bleak, we could see the importance of strong company management and the steps these companies took to survive the crisis.

As part of our research process, we pay close attention to potential corporate governance concerns, and will not hesitate to actively oppose management at times if it is in the best interests of our investments. Not only do we take a proactive approach to monitoring corporate governance practices, we also scrutinize issues including the relationship between a company and its auditor, and related-party transactions, as these matters can uncover potential poor corporate governance practices.

Quality of management is a key consideration for us, as incompetence can potentially be extremely damaging. Accordingly, when researching a company, we seek not only to meet with management and tour facilities, but we also try to meet with competitors, suppliers, customers and regulators. The information gleaned from these meetings can be crucial in understanding the company and its management quality. For example, a business regularly in arrears with its suppliers may have poor cash flow management.

Risks are everywhere and in many forms, but with proper examination, knowledge and a broad team research effort, we can better determine which we think are worth taking—and which are not.

Dr. Mobius’ comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or a recommendation to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. This material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

All investments involve risks, including possible loss of principal. Foreign securities involve special risks, including currency fluctuations and economic and political uncertainties. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated withemerging markets are magnified in frontier markets.

Links can take you to third party sites/media, directly or through new browser windows. We urge you to review the privacy, security, terms of use, and other policies of each site you visit. You use any third-party site, software, and materials at your own risk. Franklin Templeton does not control, adopt, endorse or accept responsibility for content, tools, products, or services (including any software, links, advertising, opinions or comments) available on or through third party sites or software. Franklin Templeton Investments and the author accept no liability whatsoever for any loss arising from use of this posting or any information, opinion or estimate herein.

The information provided in this posting is not a complete analysis of every material fact regarding any country, region, or market. Comments, opinions and analyses contained herein are those of Dr. Mobius and are for informational purposes only. Because market and economic conditions are subject to change, his comments, opinions and analyses are rendered as of the date of this posting and may change without notice. His opinions are intended to provide insight as to how he analyzes securities and his commentary is not intended as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. Reliance upon information in this posting is at the sole discretion of the viewer. Please consult your own professional adviser before investing.

All investments involve risks, including the possible loss of principal. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets' smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

Data from third party sources may have been used in the preparation of this commentary and neither Dr. Mobius nor Franklin Templeton Investments has independently verified, validated or audited such data. We do not guarantee its accuracy.

Franklin Templeton Investments and Dr. Mobius accept no liability whatsoever for any loss arising from use of this posting or any information, opinion or estimate herein.

Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton Investments’ US registered products, which are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable legislation. Products, services and information may not be available in all jurisdictions and are offered outside the US by other Franklin Templeton Investments affiliates and/or their distributors as local legislation permits. Please consult your professional adviser for information on availability of products and services in your jurisdiction.

© Franklin Templeton Investments