A classic barometer says US ok; EM not.

Investors seem a bit too eager to tout emerging market equities. Much as they did with technology stocks during the early-2000s, investors today are looking for the best re-entry point. Data clearly do not support anymore the notion that emerging markets are a superior growth story, yet investors seem to be ignoring the classic warnings signs for fear of missing out.

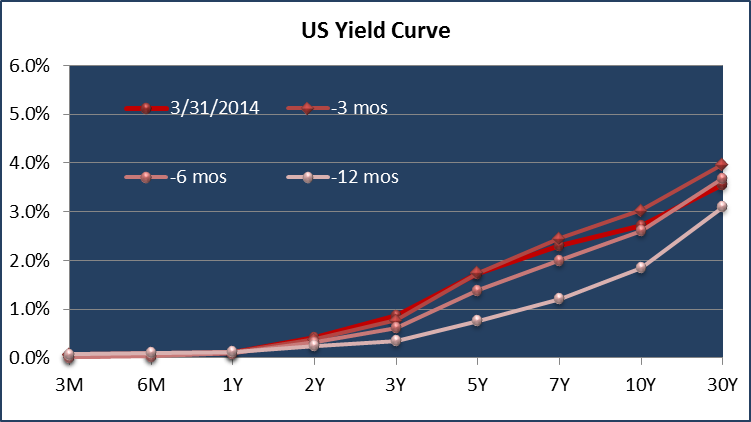

One such classic warning sign is the slope of the yield curve. Historically, steeper yield curves (i.e., wider 10-year to 2-year spread) have been reliable forecasters of stronger overall nominal economic growth and stronger profits growth. Bigger yield differentials encourage banks to lend and investors to take more risk. Inverted yield curves, however, have historically been good predictors of recessions. An inverted yield curve signals the central bank may have tightened monetary policy too much, and it may be wiser to hoard funds than to lend them. The economy tends to slow after the yield curve inverts, and the probability of a recession significantly increases.

US yield curves remain extraordinarily steep. Currently the slope of the 10 year to 2 year yield curve is around 230 basis points, which is about 1½ standard deviations* above its normal steepness (roughly 95 basis points based on data from January 1979 through March 2014). This suggests there is ample liquidity in the economy, and bank lending has indeed begun to accelerate. The US curve is not as steep as it was, but it remains very steep by historical standards (see Chart 1).

Chart 1:

Source: Richard Bernstein Advisors LLC, Bloomberg

*Standard Deviation: Statistical measure of the degree to which an individual value in a probability distribution tends to vary from the mean of the distribution.

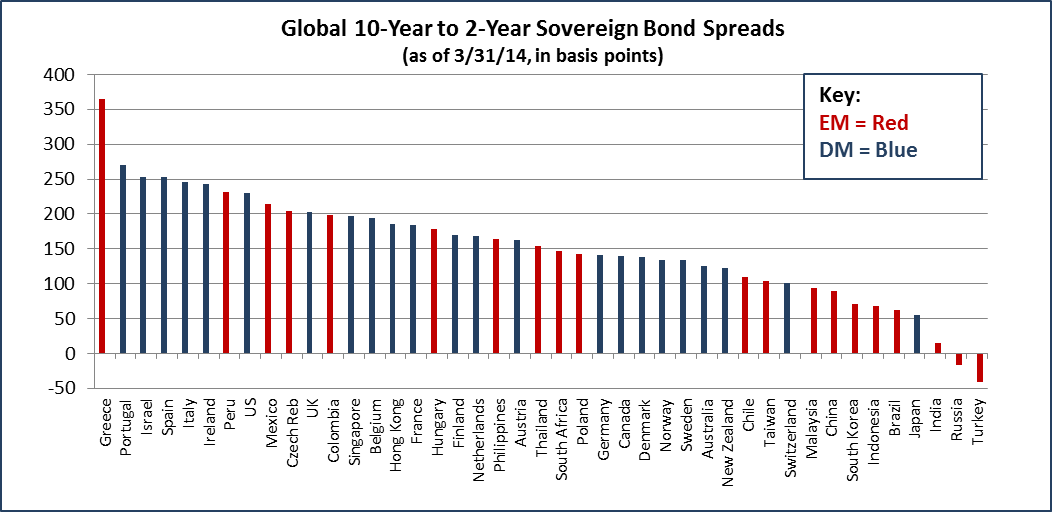

Emerging market yield curves tell a very different and disconcerting story. There is plenty of liquidity presently in the global financial markets, and there are not many flat or inverted yield curves around the world. However, with the exception of Japan and Switzerland, the emerging markets are home to all the world’s flat or inverted yield curves (see Chart 2).

Chart 2:

Source: Richard Bernstein Advisors LLC, Bloomberg

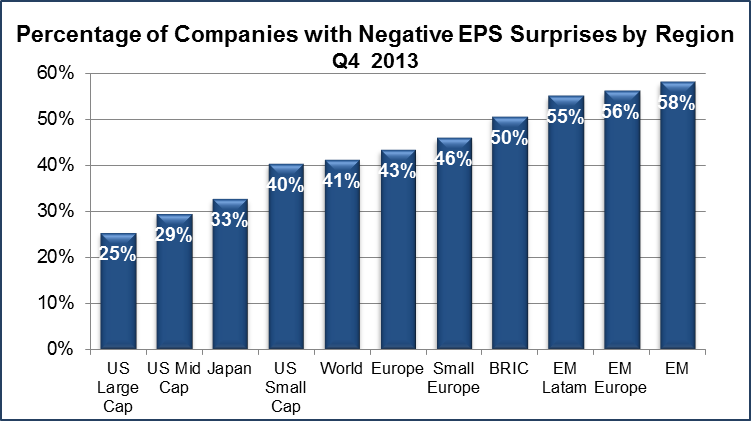

Thus, the liquidity backdrop in many emerging markets still appears to be deteriorating rather than improving as many investors suggest. Earnings growth in these markets is not strong enough to offset increasingly poor liquidity. Emerging market earnings growth continues to disappoint. As we’ve highlighted many times, emerging market companies continue to lead the world in negative earnings surprises (See Chart 3). It is hard for us to imagine that emerging market stocks will outperform when liquidity conditions are tightening and earnings continue to disappoint.

Chart 3:

Source: Source: Richard Bernstein Advisors LLC, MSCI, Bloomberg; For Index descriptors, see "Index Descriptions" at end of document.

More than four years ago we began to think the US was entering one of the biggest bull markets in our careers, but investors should be very wary of emerging markets. Nothing in our indicators suggests a change in that position. If liquidity was abundant and earnings growth was healthy, we’d readily invest in the emerging markets. Unfortunately, those characteristics are in the US and other developed markets and definitively not in emerging markets.

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

US Large Cap: Standard & Poor’s (S&P) 500® Index. The S&P 500® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

US Mid Cap : Standard and Poor's MidCap 400® Index: The S&P MidCap 400® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the mid-sized companies of the U.S. stock market.

US Small Cap: Standard and Poor's SmallCap 600® Index: The S&P Smallcap 600® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the small cap segment of the U.S. stock market.

World: MSCI All Country World Index (ACWI®). The MSCI ACWI® is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of global developed and emerging markets.

EM: MSCI Emerging Markets (EM) Index. The MSCI EM Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of emerging markets.

EM Europe: MSCI Emerging Europe Index. The MSCI EM Europe Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of emerging markets in Europe.

EM LATAM: MSCI Emerging Latin America Index. The MSCI EM LATAM Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of emerging markets in Latin America .

Japan: Nikkei: The Nikkei 225 (NKY) Index: The Nikkei-225 Stock Average is a price-weighted average of 225 top-rated Japanese companies listed in the First Section of the Tokyo Stock Exchange. The Nikkei Stock Average was first published on May 16, 1949.

BRIC: MSCI BRIC Index. The MSCI BRIC Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of the following four emerging-market country indices: Brazil, Russia, India and China.

© Copyright 2014 Richard Bernstein Advisors LLC. All rights reserved.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in, any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is an inherently risky activity, and investors must always be prepared to potentially lose some or all of an investment's value. Past performance is, of course, no guarantee of future results.

About Richard Bernstein Advisors:

Richard Bernstein Advisors LLC is an independent investment adviser. RBA partners with several firms including Eaton Vance Corporation, First Trust Portfolios LP, and BNP Paribas, and currently has $2.9 billion collectively under management and advisement as of March 31, 2014. RBA acts as sub‐advisor for the Eaton Vance Richard Bernstein Equity Strategy Fund and the Eaton Vance Richard Bernstein All‐Asset Strategy Fund and also offers income and unique theme‐oriented equity unit investment trusts through First Trust. RBA provides two indexes, the RBA American Industrial RenaissanceTM Index and the RBA Quality Income Index. RBA is the index provider for the First Trust RBA American Industrial RenaissanceTM ETF. Additionally, RBA runs ETF asset allocation SMA portfolios at UBS and Merrill Lynch and on select RIA platforms. RBA's investment insights as well as further information about the firm and products can be found at www.RBAdvisors.com.