Some 800 million voters in India are heading to the polls this month in an election process that will take several weeks to complete. India’s stock market has recently reflected the optimism investors feel in India. After a stretch of policy logjams and years of unmet potential in India, we’re also optimistic.

While we aren’t in the business of predicting elections, this one could prove historic for India. The Congress party has dominated the country since India gained independence from colonial rule in 1947, but there is a possibility that an unprecedented change could take place when the results are in. A win for the Narendra Modi-led Bharatiya Janata Party (BJP) and its allies would result in the National Democratic Alliance (NDA) coming to power at the country’s center of influence. While not without controversy, Modi’s achievements in the western state of Gujarat, where he has been chief minister for 11 years, have been viewed positively by many. Recent opinion polls suggest India’s people want that type of progress for the rest of the country.

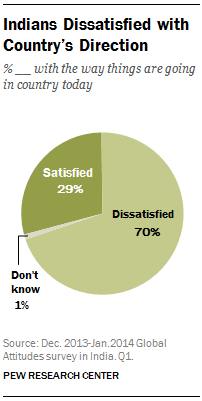

According to a recent Pew Research survey, the majority of Indians reported dissatisfaction with the way things have been going in their country and less than 30% were satisfied.1 This discontent swept across all generations, income levels and genders. We’ll see how this dissatisfaction plays out as the votes are counted. Interestingly, despite this general dissatisfaction, the Pew survey showed most Indians were upbeat about the economy’s prospects. That seems to fall in line with expectations for India’s GDP growth to outpace that of the last few years, projected to grow 5.4% in 2014 and 6.4% in 2015.2

Great Expectations in India

Indian investors were particularly optimistic about their stock market’s prospects, as well as their own financial prospects. The Franklin Templeton 2014 Global Investor Sentiment Survey (GISS)3 revealed that, out of the 22 countries surveyed, investors in India were the most optimistic about prospects for their local market, with 82% of Indian investors anticipating their local stock market to be up in 2014. Of those surveyed in the GISS, over half of Indian investors reported plans to increase their exposure to domestic (Indian) equities. And, for a second year in a row, Indian investors emerged as being the most optimistic about reaching their financial goals.

As investors, we are certainly hopeful these market predictions play out although obviously there is no guarantee. As we see it, the crux of the problems in India is that the current government hasn’t moved fast enough to make the reforms that many believe need to be made to propel the country as a whole forward. We’ve seen progress at the state level but not at the national level. In our view, what India needs is reform, plain and simple: less corruption and more action. This isn’t uniquely our view. According to the Pew Research survey, more than 80% of Indians say corrupt politicians and business people are a big problem in India. They lament the political gridlock that is holding back progress in fixing the nation’s economic problems.4

Two Areas for Reform: Bureaucracy and Education

There are two main areas we think are in need of reform. The first is the barriers to foreign investment in India, which are tremendously high. There is an excess of bureaucracy. The red tape needs to come down. The second is education. We believe the educational level of the entire population needs to be lifted. Of course, there are great universities and many well-trained, educated people in India. But, in our opinion, there are segments of the population that are missing out on the opportunities an education can provide, and that means the country is missing out on the full potential of its human resources.

As investors, we are focused on companies and industries that utilize or take advantage of the tremendous brainpower of the population. We focus on companies that can essentially export this brain power, and which are more isolated from some of the investment barriers that have impacted other industries, such as mining.

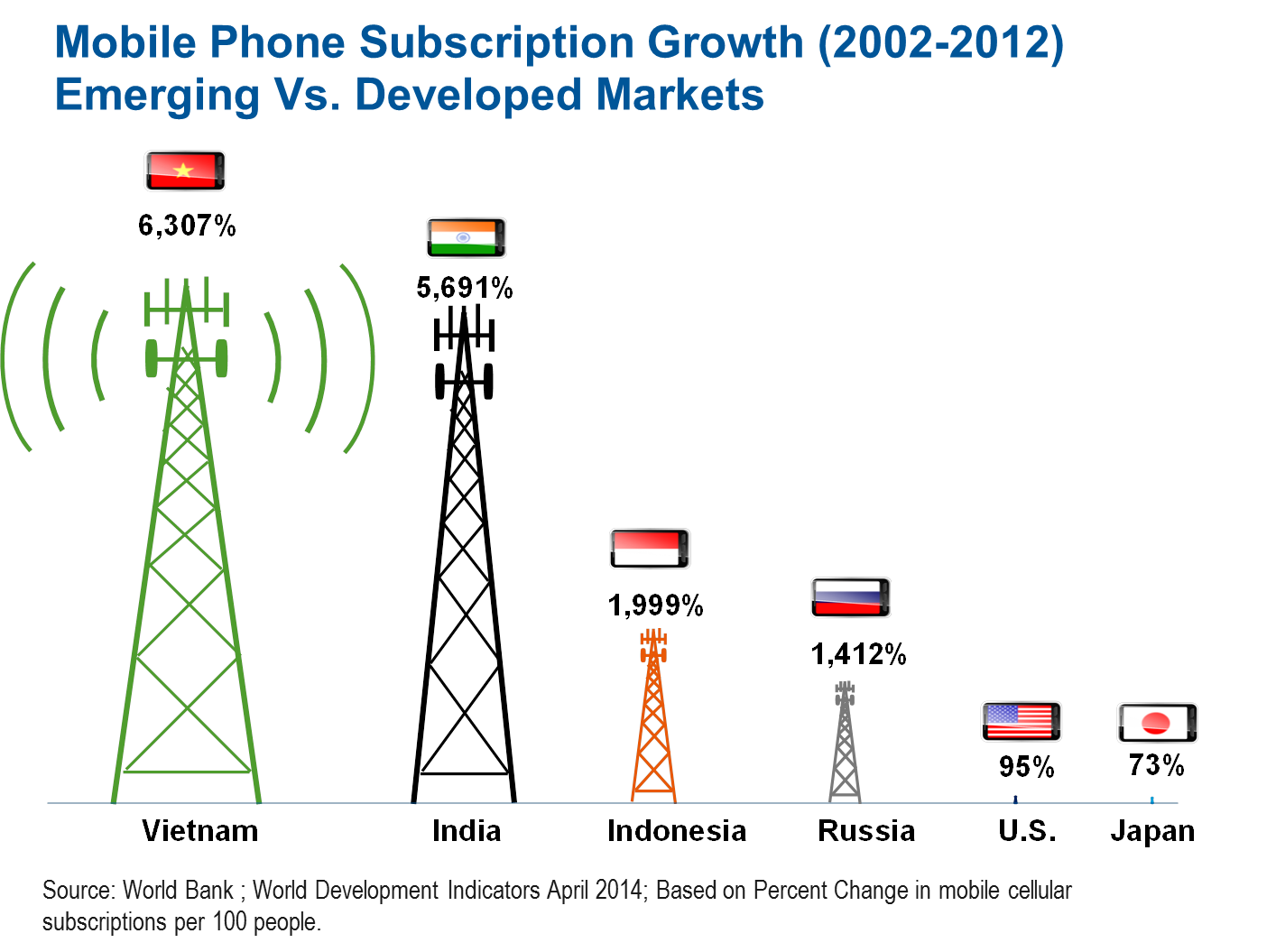

In our view, there are certainly a lot of positives for India that can bode well for its future. Its people have a relatively high savings rate, its youthful population creates a positive demographic with a lower dependency ratio than many other developed countries, and its economy is fairly diversified with a strong service sector. India’s middle class also has the potential to grow significantly, which means that it could become an even greater consumer market. Given the current economic growth rates, within 20 years it is expected that some 291 million people will move out of poverty and into the ranks of the middle class.5 With this type of growth typically comes greater spending on consumer goods and services. For example, wireless communications has been growing by leaps and bounds in India.

A Final Note

One more note I’d like to make about the Franklin Templeton Global Investor Sentiment Survey. Interestingly, more than half of all investors surveyed in all countries planned to become more conservative this year with their investments, despite the fact they also had some optimistic hopes regarding returns this year. Of course, people should evaluate their hopes in light of the actions they take—that applies to life in general, and not just investing!

Mark Mobius’ comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

1. Source: “Indians Reflect on Their Country and the World,” Pew Research Center, Washington, D.C. (March 31, 2014).

2. Source: © by International Monetary Fund. “World Economic Outlook Update,” January 2014.

3. Franklin Templeton’s 2014 Global Investor Sentiment Survey was conducted online by ORC International in January 2014. The survey polled 11,113 investors across 22 countries.

4.Source: “Indians Reflect on Their Country and the World,” Pew Research Center, Washington, D.C. (March 31, 2014).

5. Source: McKinsey Global Institute, “Next Big Spenders: India’s Middle Class.” May 2007. © 2014 McKinsey & Company.

The information provided in this posting is not a complete analysis of every material fact regarding any country, region, or market. Comments, opinions and analyses contained herein are those of Dr. Mobius and are for informational purposes only. Because market and economic conditions are subject to change, his comments, opinions and analyses are rendered as of the date of this posting and may change without notice. His opinions are intended to provide insight as to how he analyzes securities and his commentary is not intended as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. Reliance upon information in this posting is at the sole discretion of the viewer. Please consult your own professional adviser before investing.

All investments involve risks, including the possible loss of principal. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets' smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

Data from third party sources may have been used in the preparation of this commentary and neither Dr. Mobius nor Franklin Templeton Investments has independently verified, validated or audited such data. We do not guarantee its accuracy.

Franklin Templeton Investments and Dr. Mobius accept no liability whatsoever for any loss arising from use of this posting or any information, opinion or estimate herein.

Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton Investments’ US registered products, which are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable legislation. Products, services and information may not be available in all jurisdictions and are offered outside the US by other Franklin Templeton Investments affiliates and/or their distributors as local legislation permits. Please consult your professional adviser for information on availability of products and services in your jurisdiction.

© Franklin Templeton Investments