The straight “risk-on/risk-off” play where investors flee assets perceived as risky en masse in times of uncertainty seems to be becoming a bit more nuanced this year. As a bottom-up stockpicker, Peter Langerman, chairman, president and chief executive officer, Mutual Series®, takes the short-term emotional response out of the equation as he looks for opportunities for his portfolios where other investors may have jumped ship. Langerman discusses where he’s finding value today, why he thinks the markets are probably “right where they should be” and why some investors may need to take a few risks to meet their long-term financial goals.

Many people seemed scared out of their minds after the financial crisis five years ago. We’ve seen the lingering effects of this distress reflected in the results of this year’s Franklin Templeton Global Investor Sentiment Survey(GISS). The majority of surveyed investors globally (62%) indicated they believe their local stock market will be up this year, but more than half (52%) also expect to follow a more conservative investment strategy.1

Why are investors optimistic, yet reluctant to take on risk? Many investors lost money during the financial crisis, and were not only scared, but also scarred. In some cases, they felt so burned that encouraging them to tiptoe back into equities even after the market started to recover was a tough sell. Because of that fear, some investors missed out on the equity market bull run over the past several years in the United States and in many other markets. Now there is a sense of concern, of thinking: “Am I too late? Have I missed all the potential appreciation? Has the so-called ‘easy money’ been made?”

From our perspective at Mutual Series, we don’t get emotional about difficult situations in the market, and we strive to maintain a balanced view. We look at the markets and at company specifics from a long-term perspective. While valuations have moved up considerably from where they were a couple of years ago, and the global economy has improved since then as well, I think right now is a reasonable time to be in the market with a balanced approach, but not necessarily to throw all your chips down at once and buy every high flier out there.

We encourage investors to likewise take a balanced approach, to be in it for the long-term, to bear the ups and downs and to not buy something just because you think it will make you a ton of money in the next two months.

Finding Value in Europe

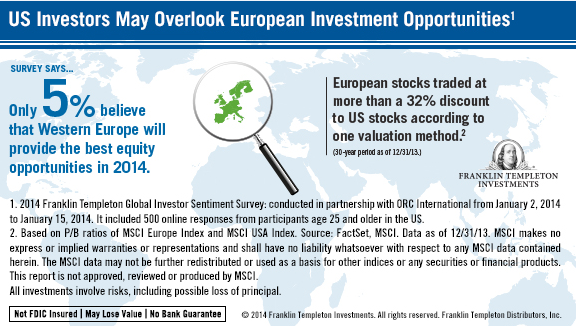

According to our GISS survey, 62% of investors globally ranked the “eurozone debt crisis” among their top three concerns about investing in Europe this year. And among US investors, only 5% believed that Western Europe would provide the best equity opportunities in 2014. Europe is an area we’ve been interested in not only this year, but for quite a while. It has been our view, again from a bottom-up perspective as well as looking at the overall macrodynamics, Europe would continue to recover at a reasonably slow pace, but remain in recovery mode nonetheless.

Over the last year or more, we have been able to find a number of investments in Europe that looked attractive to us, including companies that are more “euro-centric”—that is, doing business in Europe as well as being located in Europe. We’ve been especially interested in retail businesses and other consumer-oriented businesses that we thought were undervalued. Our opinions are based on modest assumptions that are neither particularly optimistic nor particularly pessimistic. More recently, some of those names have recovered and certainly some of the geographies in Europe have recovered as well, including a number of countries in the southern periphery.

But overall, Europe in many cases still remains a bit behind the United States in terms of the economic recovery and the stock market recovery, so there are still some selective bargains there.

A couple of years ago, and even perhaps a little more recently, there still was a lot of concern about whether Europe would be able to recover from a very, very deep crisis. I think there was a general view that the United States was a bit ahead of the game in terms of recovering, albeit at a slow pace, but had taken the medicine more dramatically, especially in the banking sector, and therefore was better prepared to recover.

What we have continued to hear and see is an absolute commitment on the part of the powers that be in Europe to do what is necessary to help prevent Europe from regressing into the kind of situation it was in a couple of years ago.

Should people looking to invest in Europe be concerned about the debt crisis? Sure. And there’s also been some concern about deflation. But do I think the issues are as troublesome as they were several years ago? No. I think when you see what’s going on at the individual-company level with CEOs and boards as well as at the macro level in Europe, there is a reasonable balance we can see reflected in the overall valuations and the overall investment case, which to us look solid.

Having said that, whether it’s in Europe or whether it’s somewhere else in the world, the Middle East or Ukraine or elsewhere, there are always unknowns. There are always issues that are very hard to predict at any given point in time. When market dislocations happen, it’s often time to think, “this too shall pass.” That’s just the world we live in.

Peter Langerman’s comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

What Are the Risks?

All investments involve risks, including possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Value securities may not increase in price as anticipated or may decline further in value. Investments in foreign securities involve certain risks including currency fluctuations, and economic and political uncertainties. . Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets.

(c) Franklin Templeton Investments

© Franklin Templeton Investments