Tabulating the costs of a college education can be overwhelming for new parents, so overwhelming, in fact, that many choose not to think about it at all, assuming the situation will resolve itself in time. Many parents wind up turning to student loans as the solution to finance a college education, often resulting in a shiny new diploma accompanied by a mountain of debt. There might be a way out, even if you don’t have the secret to picking winning lottery numbers. For many college-bound children and their parents, one real-world option for avoiding potential future college debt lies in these three numbers: 529.

What Is a 529 Plan?

So what exactly is a “529 plan?” The name stems from a section in the Internal Revenue Code. A 529 plan, legally known as a “qualified tuition plan,” can be sponsored by states, state agencies or educational institutions. These programs allow parents, grandparents and even other family members and friends to help a designated beneficiary (child) save for college costs. One of the appealing features of a 529 savings plan is that money invested grows free of federal income tax when withdrawn for qualified higher education expenses such as tuition, books, room and board. Depending on where you live, you may be able to take advantage of state tax benefits, too.1

Tax benefits of 529 plans are conditioned on meeting certain requirements. Federal income tax, a 10% federal tax penalty and state income tax penalties apply to non-qualified withdrawals of earnings. Generation-skipping tax may apply to substantial transfers to a beneficiary at least two generations below the contributor. See a 529 plan disclosure document for complete information.

Spring marks a time of graduations and also a time for those with younger children to think about ways to start saving now for the future. Designated as “529 Day,” May 29 (5/29) marks an appropriate juncture to explore the potential benefits of 529 college savings plans.

It’s never too early to think about saving for college, according to Roger Michaud, senior vice president of North American Advisory Services and Director of College Saving Plans at Franklin Templeton and also chair Savings Foundation chair emeritus.

“Parents and grandparents who can squeeze even a few extra dollars out of their budgets for college savings plans will help their children set off toward a brighter future, possibly even one free, or mostly free, of debt. Total US student loan debt is estimated at over $1 trillion and eclipses credit card debt,2 a crushing amount. It makes sense to plan as early as possible to help reduce this burden in the future,” said Michaud.

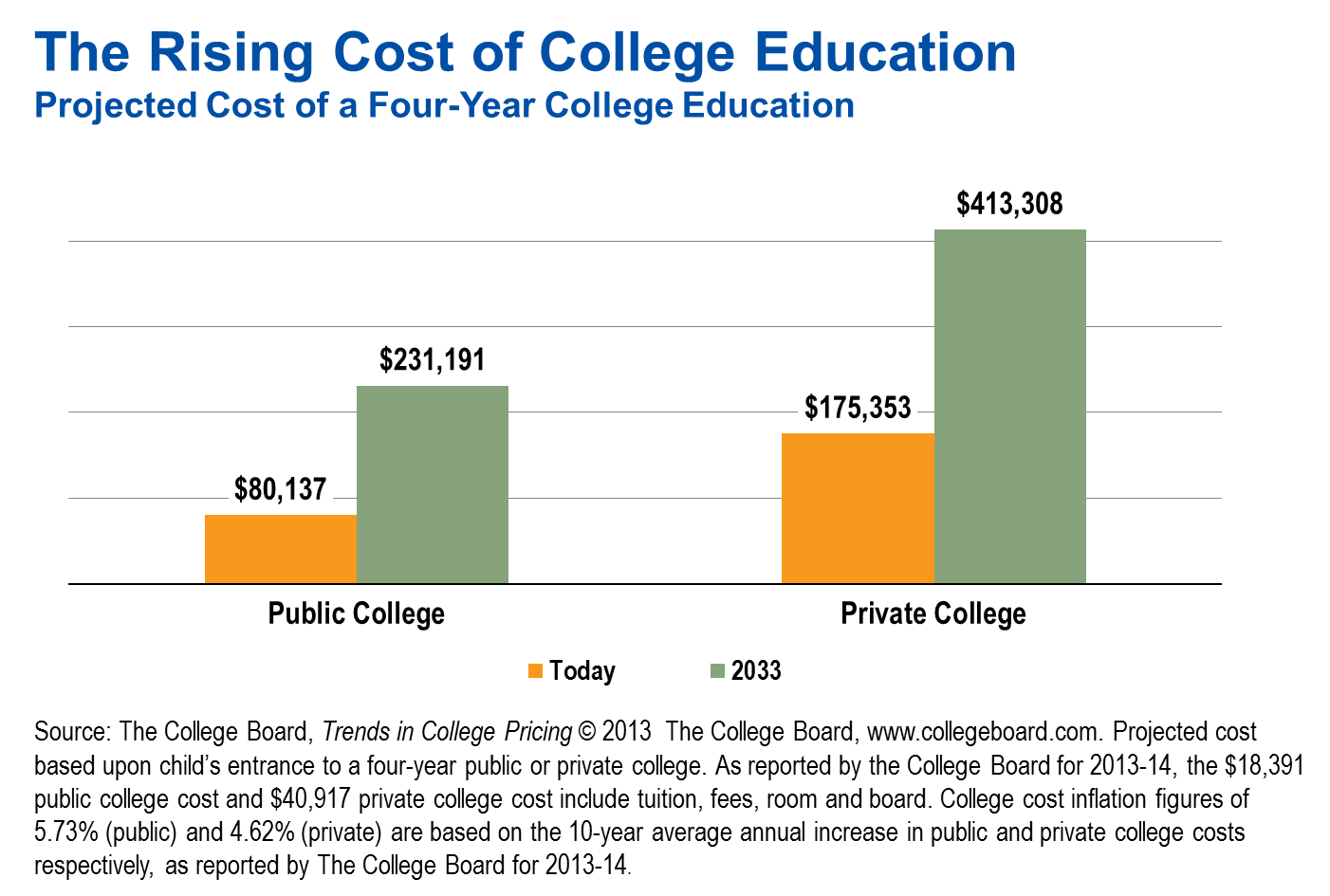

The cost of college has been escalating faster than inflation, and beyond the reach of many American parents who hope to fund a child’s higher education. Including tuition, room, board and expenses, the average total cost in 2013–2014 for an in-state student at a four-year public college is $18,391 per year, and for a four-year private college, it is $40,917 per year.3

Says Michaud, “Imagine what your children could do if they did not have the burden of student loan debt. Buy a house. Start a family. Save for their retirement. And, maybe, not move back in with you after they graduate!”

Parents Getting the Message

The good news is that many parents are getting the message that it pays to save. The College Savings Foundation’s 2013–2014 State of College Savings Survey saw the highest percentage of parents saving (55%) since the survey was first launched in 2007. At the same time, parents are saving greater amounts: 53% have saved at least $5,000 per child for college, up 8% from last year and the highest level in seven years.4 Savvy habits—like starting early and saving consistently—seem to be contributing to this increase, according to the Foundation.

“Parents are becoming more aware of the need to save, and more are making 529s their preferred vehicle,” according to Michaud. “Successful savers know starting early is key. And, working with an advisor can be a valuable exercise to help parents better understand different college funding options, as well as helping them stay on track in reaching their goals.”

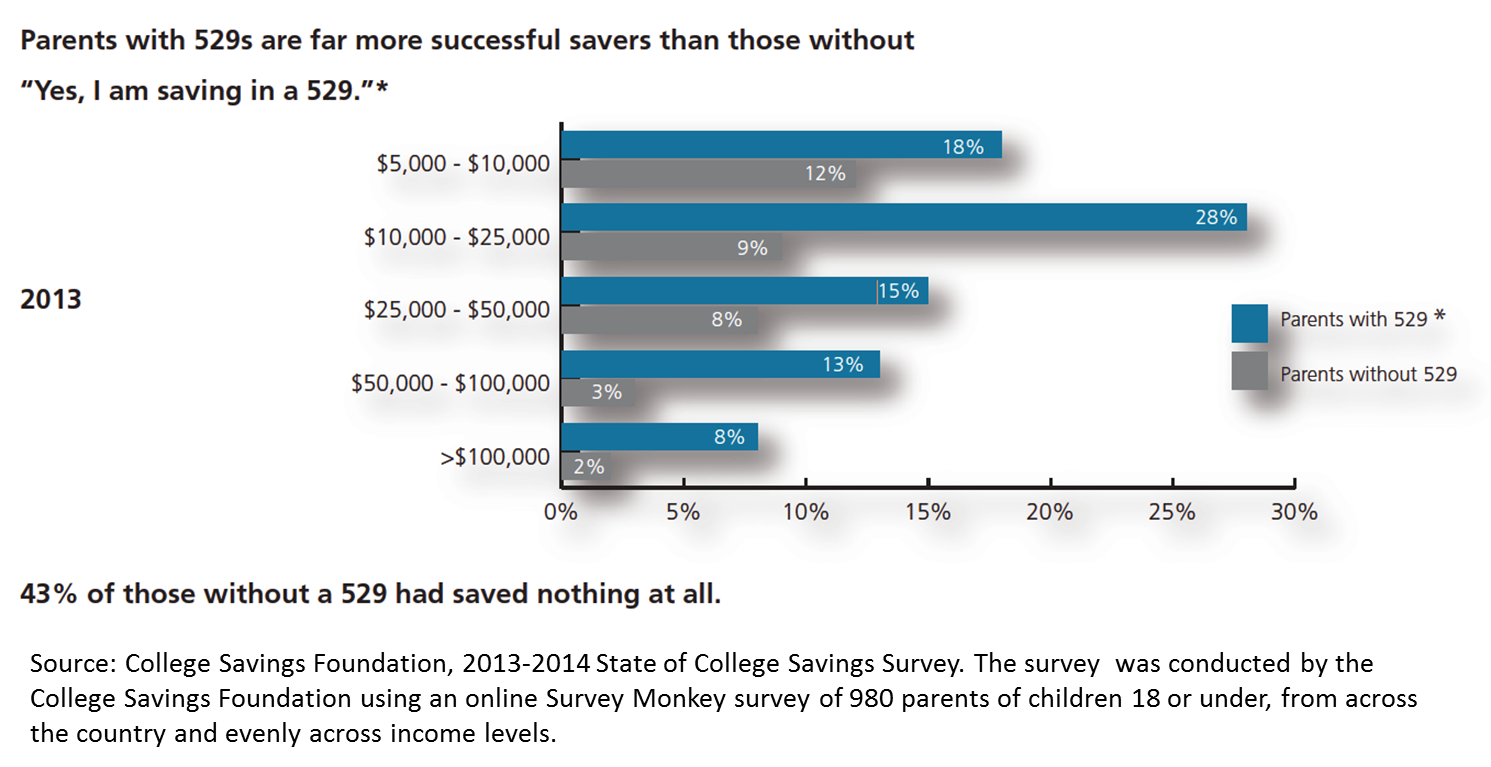

The College Savings Foundation’s survey showed that knowledge—at least about 529s—is savings power. When asked if they knew what a 529 was, parents who said that they were saving in a 529 were more successful savers than those who didn’t know about them or use them. You can see in the graphic below that 28% of 529 owners had saved between $10,000 and $25,000, compared to only 9% who saved that much without one. And, 43% of parents without a 529 plan had saved nothing at all5

The bottom line? Financing a college education doesn’t have to result in leveraging a student’s future.

What Are the Risks?

All investments involve risks, including potential loss of principal.

Investors should carefully consider 529 Plan investment goals, risks, charges and expenses before investing. To obtain an Investor Handbook, which contains this and other information, talk to your financial advisor or call Franklin Templeton Distributors, Inc., the manager and underwriter for the Plan at 1-800-818-4030. You should read the Investor Handbook carefully before investing and consider whether your, or the beneficiary’s, home state offers any state tax or other benefits that are only available for investments in its qualified tuition program.

© Franklin Templeton Investments