Investors can be as greedy for yield as they can be for capital appreciation, and so far this cycle has fit that historical norm. Despite the perceived safety of income-producing securities, investors have begun to stretch for higher yields and, in doing so, seem to be taking substantial and unanticipated risks.

At RBA, we search for gaps between perception and reality, and this seems to be the case for emerging market debt. Investors have been lured to these securities by their higher yields, yet the underlying economic and currency fundamentals are deteriorating without commensurate widening of spreads.

Investors seem to be ignoring growing warning signs for emerging market debt. The signs include:

- Emerging markets’ high rates of money growth

- Rising inflation

- Increasing political instability

- Currency instability

We remain ardent fans of US assets, and still believe that fixed-income investors searching for higher yields should look within the United States. The ongoing deflation of the global credit bubble will likely prove to be a significant and secular hindrance to emerging market growth, and investors still appear to be underpricing the risks associated with emerging market assets.

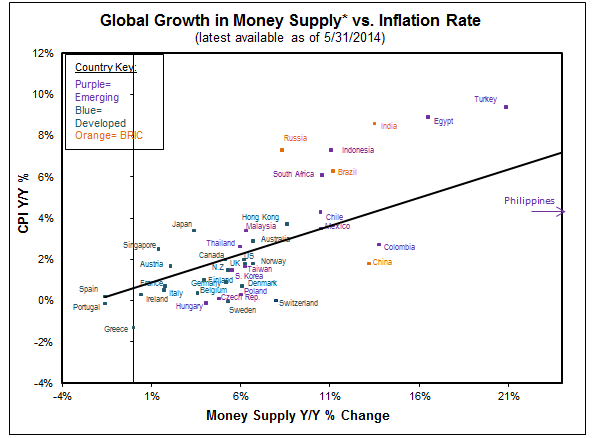

EM Inflation and money growth quite high.

The emerging markets have had for the last several years the highest rates of money growth and the highest rates of inflation in the world. Chart 1 shows the latest money supply growth rates and inflation rates for forty-one countries, and emerging markets comprise all the countries with substantial money growth and inflation. In fact, many of the major emerging markets now have inflation rates between 5% and 10%.

One should not be fooled by small numbers. Five percent inflation is two-and-a-half times the current US inflation rate, and ten percent is five times the US inflation rate. The global economy is in the midst of a credit deflation, and today’s five to ten percent inflation could have the same detrimental effects on an emerging economy as did prior cycles’ higher absolute rates of inflation.

Investors’ certainty regarding an inevitable increase in US inflation is somewhat puzzling because the US data has been remarkably benign. The current US M2 growth rate of 6.2% is below the long-term average of 6.9%. It is hard for us to envision abnormal rates of US inflation with the supply of money growing below average.

Chart 1:

Source: Richard Bernstein Advisors LLC, Bloomberg *Money Supply defined as M2 (or M3, if M2 not available, or IMF Currency Issued by Monetary Authority in National Currency, for EMU countries).

EM currencies under pressure

Currency is critically important when investing in non-dollar bonds regardless of whether the bonds are issues in dollars or in local currency. The question is whether the issuer or the investor takes currency risk. Regardless, weakening emerging market currencies are not favorable for emerging market debt investing.

The emerging market issuer accepts the currency risk when issuing a US-dollar denominated bond. The risk of default tends to increase as the dollar appreciates because it takes a larger amount of local currency to pay the dollar-denominated coupon.

The investor accepts the currency risk when buying a local-currency emerging market bond. Nothing changes for the issuer if the local currency depreciates, and the issuer continues to pay the local currency coupon (assuming the issuer’s cash flow or tax revenues still support the local currency coupon). However, the local-currency coupon becomes smaller when translated into dollars, and the US-dollar coupon effectively decreases.

Bond yields typically increase when an issuer becomes riskier. That would not be the case for a local-currency bond held by a US-dollar investor when the local currency is depreciating. The dollar value of the coupon would be decreasing despite the bond’s increasing risk. If the risk of the bond were indeed increasing, then the bond’s price would have to depreciate at an accelerating rate to more than offset the smaller coupon. This price reaction to a decreasing coupon is called “negative convexity”.

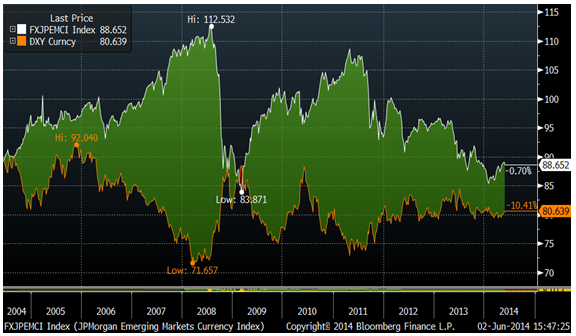

Negative convexity isn’t an issue so long as the US dollar depreciates. Chart 2 shows the relationship between the tradable dollar index (DXY) and the JP Morgan Emerging Market Currency Index (FXJPEMCI). The US dollar has generally been stable for six years, whereas the emerging market currency index has been falling. That implies the hedging costs associated with emerging market local currency debt has been increasing.

Chart 2:

Source: Bloomberg

Political instability rising – “Coup Count” up to three

The “coup count” is up to three. Certainly, the coups in Egypt, Ukraine, and Thailand are extreme, but we think the growing civil unrest in many emerging markets is a symptom of deteriorating economic conditions. Coups, riots, protests, etc. tend to occur when citizens are unhappy. Civil unrest occurs when citizens’ standard of living is deteriorating and they feel they have no recourse.

The high rates of inflation in some emerging markets have existed for so long that the standard of living is decreasing. The spreading civil unrest is a symptom of those falling standards of living. Yet, investors remain enamored with the emerging market consumer investment theme, and continue to ignore the deteriorating standard of living in a growing number of emerging market economies.

High yield munis seem attractive to us

It seems ironic that investors are stretching for yield in risky emerging market debt despite the growing warning signs, but they won’t invest in higher yielding securities within the US even though fundamentals are improving. We continue to prefer high yield municipal bonds, and have sizeable positions in our portfolios. In our view, these bonds provide excellent yield, good total return prospects, and very attractive spreads versus riskier emerging market debt.

© Copyright 2014 Richard Bernstein Advisors LLC. All rights reserved.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment's value. Past performance is, of course, no guarantee of future results. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.

About Richard Bernstein Advisors:

Richard Bernstein Advisors LLC is an independent investment adviser. RBA partners with several firms including Eaton Vance Corporation and First Trust Portfolios LP, and currently has $3.2 billion collectively under management and advisement as of May 31, 2014. RBA acts as sub‐advisor for the Eaton Vance Richard Bernstein Equity Strategy Fund and the Eaton Vance Richard Bernstein All‐Asset Strategy Fund and also offers income and unique theme‐oriented unit trusts through First Trust. RBA is also the index provider for the First Trust RBA American Industrial RenaissanceTM ETF and the First Trust RBA Quality Income ETF. Additionally, RBA runs ETF asset allocation SMA portfolios at UBS and Merrill Lynch and on select RIA platforms. RBA's investment insights as well as further information about the firm and products can be found at www.RBAdvisors.com.