Hopes for a pick-up in the housing recovery just got a little higher.

A series of economic data released last week suggests we’re seeing a small but significant comeback in the housing market. This is welcome news given that housing hit a speed bump last summer, when mortgage rates jumped in anticipation of the start of Fed tapering.

More recently, mortgage rates have moved slightly lower at the same time the economy is bouncing back from a harsh winter. It now looks like the housing recovery that we saw prior to mid-2013 is back on track, albeit more tempered.

The biggest driver of the recent housing surge has been new homes, which experienced an 18.6% increase in sales and a 4.6% increase in prices in May. The number of new homes on the market hasn’t increased, and so the increase in sales reduced the supply-relative-to-sales ratio to 4.5 months from 5.3 months in April.

But new homes are only a small portion of the total housing market. And existing homes have been experiencing a far more muted recovery. The April S&P Case-Shiller Home Price Index rose just 0.2% on a seasonally adjusted basis, resulting in a year-on-year price rise of 10.8%. That’s down from a 12.4% annual pace in March and less than the 11.4% economists were expecting.

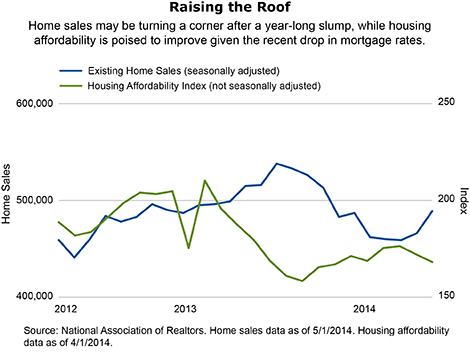

Rising Demand?

However, the picture for existing home sales may be getting brighter. Existing home sales rose 4.9% in May, much better than expectations and the previous month’s growth, suggesting an acceleration in improvement. While the number of existing homes on the market rose, sales increased at an even faster pace. That caused the supply to drop slightly. The median existing-home price climbed substantially, from $201,500 to $213,400, in just a month. In addition, all regions saw an increase in sales.

From our vantage point, it appears that lower mortgage rates and the late spring thaw have combined to improve the housing situation. The recovery should continue, but at a moderate pace. In fact, we see four key catalysts powering the housing recovery from here:

1. Interest rates—including mortgage rates—should remain lower for longer. The Fed has said it plans to keep its target interest rate low long after it ends its bond-buying program.

2. We see demand outpacing supply in the near term. The MBA National Delinquency Survey for the first quarter of 2014 showed that the foreclosure situation is improving, which translates into less supply. New foreclosures have fallen to pre-crisis levels while foreclosure inventory has decreased substantially. In addition, fewer homes are being built than are needed. For example, there were 1.1 million housing starts in April, well below the level seen in a more normal environment.

3. We’ve seen a recent improvement in consumer sentiment, which we expect to continue. The Thomson Reuters/University of Michigan consumer sentiment index for June rose to 82.5 from 81.9 in May. With consumers more positive, they are more likely to make all kinds of purchases, including homes.

4. The employment situation should continue to improve. Labor-market conditions are improving slowly. At some point, we expect to see some long-awaited wage growth, which should help make homes more affordable and appealing to consumers. While we don’t expect to see this wage growth reflected in Thursday’s jobs report, we do think it will happen over time. And that’s important because wage growth is a necessity for a sustainable housing recovery.

As we celebrate Independence Day and all that we love about America later this week, it seems fitting that a very American ideal—home ownership—appears to be on the mend. And that, in turn, should be good for America.

Kristina Hooper, CFP, CAIA, CIMA, ChFC, is US head of investment and client strategies for Allianz Global Investors.She has a B.A. from Wellesley College, a J.D. from Pace Law and an M.B.A. in finance from NYU, where she was a teaching fellow in macroeconomics.

The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Past performance of the markets is no guarantee of future results. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities.

A Word About Risk: Equities have tended to be volatile, involve risk to principal and, unlike bonds, do not offer a fixed rate of return. Foreign markets may be more volatile, less liquid, less transparent and subject to less oversight, and values may fluctuate with currency exchange rates; these risks may be greater in emerging markets.

Unless otherwise noted, index returns reflect the reinvestment of income dividends and capital gains, if any, but do not reflect fees, brokerage commissions or other expenses of investing. It is not possible to invest directly in an index.

The S&P/Case-Shiller Home Price Indices are the leading measures for the US residential housing market, tracking changes in the value of residential real estate both nationally as well as in 20 metropolitan regions.

Allianz Global Investors Distributors LLC, 1633 Broadway, New York NY, 10019-7585, 1-800-926-4456.

AGI-2014-06-30-9945