Over the past few years, various prosecutorial arms of U.S. government entities have brought charges against foreign banks that have violated U.S. sanctions that were placed on different countries. The most recent situation involved BNP Paribas SA (BNP, €48.37),[1] which was hit with an $8.97 billion fine, the largest of its kind for this type of violation. At present, Bloomberg is reporting that other banks are under investigation, including Commerzbank AG (CBK, €11.05), which is reportedly near a settlement with U.S. officials. According to the same report, Credit Agricole SA (ACA, €10.21), Societe Generale SA (GLE, €57.50), Deutsche Bank AG (DBK, €26.03) and UniCredit SpA (UCG, €5.95) are also under investigation.[2]

The U.S. has placed economic and financial sanctions on a number of countries over recent decades. Cuban sanctions were first implemented in 1960, and Iran has been under some form of sanction since 1979. However, the U.S. government placed much more sophisticated sanctions on the financial system after 9/11. In a bid to cut off the financial support system for al Qaeda, Treasury officials developed systems to better track money flows. These new programs have reduced the ability of rogue elements to use the banking system to manage their fund flows.

However, there is another important element to this story. Because the U.S. dollar is the global reserve currency, there are numerous transactions that occur using dollars that don’t involve U.S. citizens. The U.S. government takes the position that these transactions which occur in dollars and almost always require the use of the U.S. financial system means that U.S. law applies to the financial firms that engage in these transactions. And so, a foreign bank can be charged under U.S. law for transferring U.S. dollars for a regime under sanction, even if there is no foreign law against the bank’s activity.

For the most part, foreign banks have faced the majority of the sanctions for this behavior. Until the recent fine on BNP Paribas, during the Obama administration, fines totaling $4.9 billion were levied; only $88.3 million were against a U.S. bank, J.P. Morgan Chase.[3] Thus, “sanctions busting” would appear to be a mostly foreign bank crime.

Using the U.S. financial system and the dollar’s reserve currency role to implement sanctions gives America a powerful tool in exercising foreign policy. Needless to say, other nations are chafing at this extension of America’s superpower status.

In this report, we will discuss the general nature of U.S. sanctions and how these banks violated American law. From there, we will reiterate the dollar’s reserve currency role from both a historic and theoretical perspective and show how this role makes the currency and the U.S. financial system pivotal in the global economy. We will conclude with market ramifications.

The Case

As noted above, the U.S. has, for various reasons, placed financial and economic sanctions on certain countries. Such measures are generally considered hostile acts that are short of open warfare. The threat that Castro’s Cuba posed to the U.S., best seen by the Cuban Missile Crisis in 1962, required a response. However, since the Soviets treated Cuba as a satellite state, the U.S. couldn’t conduct open warfare on Castro for fear of triggering WWIII. In fact, the world flirted with this outcome in 1962. So, as a substitute, the U.S. implemented trade and financial sanctions against the Castro regime. This did not prevent other nations from trading with Cuba; Spain and Canada, along with the Soviet Union, regularly conducted trade with the island nation. However, as was common with communist states, most of the trade was countertrade, which is a form of international barter. Using countertrade allowed the parties to avoid using dollars in the transaction. However, it also limited the scope of trading to items that could be bartered.

After the 1979 Iranian Revolution and the Hostage Crisis, Iran has been under varying degrees of sanctions. In response to the Mullah’s nuclear program, sanctions were tightened further (see WGR, Iran and S.W.I.F.T., 3/5/2012). The financial sanctions have made it nearly impossible for Iran to export oil and receive payment in dollars.

Other nations have also come under sanctions. Sudan is a case in point. It harbored Osama bin Laden and al Qaeda leaders for a while and has been under some sort of U.S. sanction since 1997. The recent civil war and genocide that led to the creation of South Sudan was cause célèbre among numerous celebrities.

BNP Paribas did business with Iran and was heavily involved with the Sudanese regime. The French bank facilitated the sale of Sudanese oil that bankrolled the massacre of thousands of civilians. In 2006, BNP’s Swiss branch held nearly 50% of Sudan’s foreign reserves.[4] Despite numerous warnings, and a 2004 Memorandum of Understanding the bank signed agreeing to improve its compliance, the bank continued to do business with rogue regimes.

And so, U.S. prosecutors threatened massive fines and felony arrests. In a plea agreement, BNP accepted the aforementioned fine, two guilty pleas and an unprecedented one-year suspension of dollar clearing rights for its oil and gas financing arm. This is the harshest penalty for a foreign sanctions violation in history.

Needless to say, foreign governments are upset by America’s extension of its sanctions laws. French political figures pressed the U.S. hard to reduce or eliminate sanctions. However, President Obama made it clear in public comments that he would not interfere with the activities of the Department of Justice. The Economist noted that due to the perception of overly zealous prosecution, the U.S. has managed to make the financial facilitator of genocide a sympathetic figure,[5] but, in reality, without a world government or a universally accepted world judicial system and method of enforcement, the world has no other choice than to either submit to a reigning superpower or live with the chaos of a world without one.

The History of the Dollar’s Reserve Currency Role

In July 1944, while the Second World War was raging, 44 nations met at a resort in Bretton Woods, New Hampshire to sketch out the post-war financial system. Their goal was to avoid a depression after the war. After World War I ended, the global economy fell into a slump. There was great fear that the pre-war depression would resume once the war ended. After all, the U.S. economy had been bolstered by the war effort and when the industrial sector no longer needed to produce war materials, a slowdown seemed likely.

The delegates believed that one of the reasons for the Great Depression was widespread trade protection. With most of the developed world on the gold standard, there was a raft of devaluations against gold during the 1930s. These “beggar thy neighbor” policies tended to help the devaluing economy in the short run, but usually prompted other nations to respond with their own devaluations or block trade with other countries through tariffs and quotas.

The Bretton Woods agreement was designed to discourage anti-trade policies by linking the developed world’s currencies to the U.S. dollar. The dollar was pegged to gold and foreign central banks could redeem their dollars for gold upon request. In effect, after this agreement, the United States was firmly in control of free world international trade.

After WWII, with Europe and Asia severely damaged by the conflict, the United States dominated world trade. In fact, in the early 1950s, there was great concern about a global “dollar shortage.” But over time, as the devastated nations rebuilt, the flows began to reverse and the United States began to run persistent trade deficits. For the global financial system to operate, the United States must act as the “importer of last resort” to ensure ample global liquidity. This meant that the United States would need to run persistent trade deficits to ensure sufficient global liquidity.

With the dollar’s reserve currency status, the United States could avoid the devaluations and economic contractions that other nations would have faced with persistent trade deficits. Other nations were willing to hold dollar balances because of the deep U.S. financial markets (allowing these dollars to be easily invested in the United States) and for its easy convertibility into other currencies. In addition, dollars could be used to buy commodities. In effect, a reserve currency nation gets to “submit checks for purchases that nobody cashes.”

Perhaps the best way to understand the dollar’s role is to consider the following example. Let’s assume that a Paraguayan chocolatier wanted to buy cocoa beans from the Ivory Coast. They agree on a price of $3,110 a ton. However, the Paraguayan wants to pay for the beans in his local currency, the guarani. The dealer in the Ivory Coast now has a problem; unless he has something from Paraguay that he wants to import or feels confident in the country’s financial system, there is little the dealer can do with a payment in guarani. Thus, the dealer will demand payment in U.S. dollars; the dollar can buy a plethora of goods in the U.S. or elsewhere, or can be invested in America’s deep and safe financial markets. Of course, this condition means that virtually all the nations of the world have an interest in running trade surpluses with the U.S. to acquire dollars for global trading and reserve purposes.

In the late 1960s, a number of European nations, concerned about their rapidly expanding reserve balances, began to convert their dollar balances into gold. In response, the Nixon Administration, on August 15, 1971, ended the convertibility of the dollar into gold, effectively ending the period of fixed exchange rates. Since then, the world has operated with a non-fixed currency system. It isn’t a pure “float” because many governments actively intervene to manipulate their currency exchange rates.

The Reserve Currency’s Public Good

Economists define a public good as a product or service that must be provided by governments because the private market won’t provide the good, or will provide the good in less than optimal amounts. There are seven public goods a reserve currency nation should provide:

1. Act as a consumer (importer) of last resort;

2. Coordinate global macroeconomic policies;

3. Support a stable system of exchange rates;

4. Act as lender of last resort;

5. Provide counter-cyclical long-term lending;

6. Provide a truly riskless AAA asset for benchmarking purposes; and

7. Supply deep and predictable financial markets.

Charles Kindleberger, an economist who studied asset bubbles, provided the first five, and Mohamad El-Erian, the former co-CEO of PIMCO, provided the last two.

Because the reserve currency provides global liquidity, the reserve currency country must run a persistent current account (trade) deficit. If this nation ran a surplus, it would act as a global monetary policy tightening. However, this deficit would need to be “manageable.” If it became too large, it could weaken foreign investors’ confidence that the risk-free asset is truly risk free.

This chart shows net exports as a percentage of GDP. Initially, after World War II, the U.S. ran a large trade surplus. However, this rapidly contracted as the U.S. carried out its role as importer of last resort. Although the trade balance tended to be positive for most of the 1960s, the U.S. was running persistent deficits with Europe, the first region to recover after the war. In the 1970s, trade deficits became more common after President Nixon closed the gold window.

However, from the 1980s forward, deficits became larger and more persistent. In addition to Europe running export promotion policies, Japan and other nations in Asia followed the same path. Over time, the U.S. has been required to take on larger levels of debt in order to supply the world with enough dollars to maintain global liquidity.

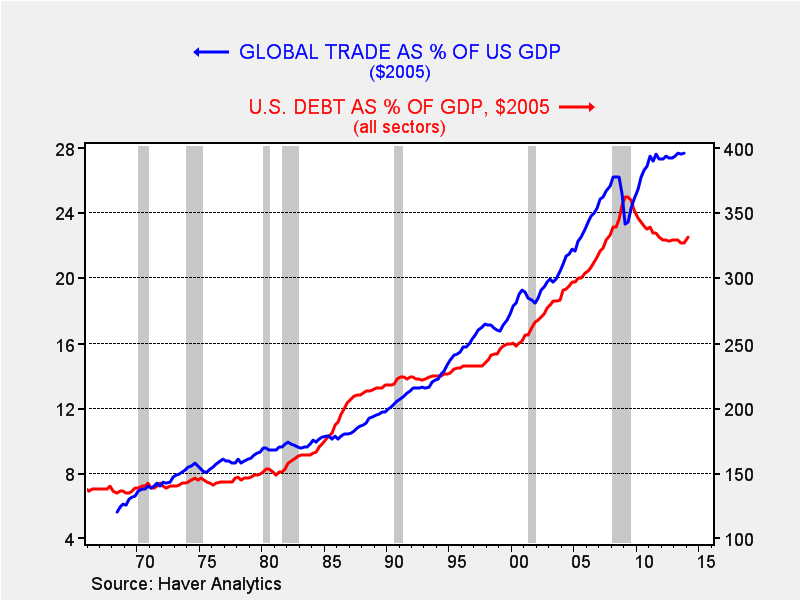

This chart shows the relationship of U.S. debt levels to the level of global trade to U.S. GDP. Note that as global trade has increased, the U.S. has taken on higher levels of debt to facilitate this growth. It is also important to notice that as the U.S. has engaged in deleveraging since the 2008 Financial Crisis, the growth in global trade has slowed significantly.

“No One Cheered for Goliath”

This quote, ascribed to Wilt Chamberlain, describes the U.S. position. There is no global governance. No non-sovereign currency exists that is universally accepted.[6] There is a world court but its ability to enforce rules rests mostly on the U.S. arresting those indicted. There is no global central bank or enforcer of trade rules. The only entity in the world that could reasonably enforce rules on a global scale is the United States. And, since there is no globally accepted body of international law, it is up to the U.S. to decide which laws to enforce. This naturally means that the law most likely to be enforced is U.S. law.

It is completely reasonable for other nations to resent America’s enforcement of its rules. There is a classic quote from an unnamed official with Standard Chartered Bank, which was accused by the U.S. of violating sanctions against Iran. The official sputtered, “…you Americans…who are you to tell us, the rest of the world, that we are not going to deal with the Iranians?”[7] However, given that no other nation wants to bear the burden of being the superpower, which includes not only the costs of providing the reserve currency but also providing global military security, then until something changes, the U.S. can enforce its rules on the world as it sees fit, if it has the power to coerce behavior.

Ramifications

The European media has been warning the U.S. that its “capricious” behavior, allowing prosecutors to bring foreign entities to justice under American law, will encourage foreign banks and companies to seek other reserve currencies. Presumably, that currency would be the euro. However, at the end of last year, S.W.I.F.T. reported that 81.1% of all letters of credit were denominated in U.S. dollars. Although this number is down from 85.0% in 2012, it clearly shows that, for international trade transactions, the dollar remains supreme.

Will the dollar be replaced? Although it is possible, we doubt any other nation will be willing to accept the role of providing the aforementioned global public goods that the reserve currency nation is required to make available. For example, for the euro to become the global reserve currency, Germany would have to run persistent trade deficits, which would be a major change in behavior and policy.

What about the yuan? Although China may be more open to running trade deficits at some point, it will be a while before China will open its financial markets to allow foreigners to hold their debt and affect their interest rates. At present, China’s capital account is only partly open to foreigners and giving up these capital controls isn’t likely in the near term.

For the foreseeable future, the world is “stuck” with the dollar and the U.S. legal system. This gives the U.S. great power to implement financial sanctions against nations it opposes. Until another nation or group of nations is willing to accept the burdens of being a superpower, the dollar should continue to not only remain the reserve currency but also give the U.S. a significant tool in global geopolitical management. This factor will tend to support the dollar’s exchange rate even as the Federal Reserve engages in policies that would usually be expected to bring about currency weakness. Of course, when policy tightens, it may also mean that the dollar will become surprisingly stronger.

Bill O’Grady

July 14, 2014

This report was prepared by Bill O’Grady of Confluence Investment Management LLC and reflects the current opinion of the author. It is based upon sources and data believed to be accurate and reliable. Opinions and forward looking statements expressed are subject to change without notice. This information does not constitute a solicitation or an offer to buy or sell any security.

[1] All prices are in home markets, 4:20 CDT, Wednesday, July 09, 2014.

[2] Farrell, Greg and Strowatt, Shane. “Commerzbank Said to Face Penalties in the U.S. Sanction Probe.” Bloomberg news wire, 8 July 2014.

[3] ibid

[4] “No Way to Treat a Criminal.” The Economist, 5 July 2014.

[5] ibid

[6] Some would argue that gold could play this role but, in reality, gold only acts as a store of value and, perhaps, a unit of account. However, even during the gold standard era, it was less commonly used as a medium of exchange. Instead, paper currency backed by gold was used, which was really a form of demand deposits. Bitcoin may eventually evolve into this universal currency. Its use as a medium of exchange is growing and it could potentially fulfill the other functions of money, unit of account and store of value. However, sovereign governments will be loath to relinquish the flexibility that money provides; although the IRS will accept bitcoins for taxes, it treats them as property, meaning that one is paying their taxes with an asset, like stocks or a chicken! Thus, using bitcoins to pay taxes can, paradoxically, create a tax liability, which would be determined by the difference between what the owner paid for the bitcoin in dollars, and the “exchange rate” at the time the taxes are paid.

[7] Dyer, Geoff. “U.S. Sanctions Risk Provoking Global Backlash Against the Dollar.” Financial Times, 3 July 2014.

© Confluence Investment Management LLC

Confluence Investment Management LLC is an independent, SEC Registered Investment Advisor located in St. Louis, Missouri. The firm provides professional portfolio management and advisory services to institutional and individual clients. Confluence’s investment philosophy is based upon independent, fundamental research that integrates the firm’s evaluation of market cycles, macroeconomics and geopolitical analysis with a value-driven, fundamental company-specific approach. The firm’s portfolio management philosophy begins by assessing risk, and follows through by positioning client portfolios to achieve stated income and growth objectives. The Confluence team is comprised of experienced investment professionals who are dedicated to an exceptional level of client service and communication.

© Confluence Investment Management