When we started Richard Bernstein Advisors roughly five years ago, we thought the US was entering one of the biggest bull markets of our careers. Today, we are likely in the midst of this long bull market. Despite the general consensus that a bear market is on the horizon and investors’ ongoing interest in protecting potential downside risk, we do not think the Fed, investors, or corporations are yet sowing the seeds for the next recession.

The current IPO market certainly seems highly speculative, but our recent Financial Timescommentary discussed how the speculation within the IPO market actually reflects investors’ fears regarding plain stocks that are sensitive to the economy.

High-beta stocks within the S&P 500® are actually selling at their cheapest relative valuations in nearly thirty years of data. The IPO market is frothy, but that frothiness doesn’t seem to have spread to more traditional stocks.

Investors remain uncertain

Investors never fully embraced the bull market and remain very uncertain despite that the bull market is more than five years old. Consider the following:

1) Credit Suisse data shows that US pension funds have their lowest equity allocations in more than 30 years.

2) BofAML’s “Sell Side Indicator” highlights that Wall Street strategists continue to underweight equities in their recommendations.

3) ISI’s hedge fund survey suggests that hedge funds are neutrally positioned.

4) ICI mutual fund flows have been negative for US equity funds for more than two months.

5)As mentioned, S&P 500® high beta stocks are selling at their cheapest relative valuations in nearly 30 years.

More importantly, corporations remain uncertain, too Over-enthusiasm is typically a characteristic of the late stages of a bull market. Analysts often focus on investor sentiment to determine if investors are over enthusiastic about stocks. As noted above, the data strongly suggest limited, if any, enthusiasm for the broader stock market.

It is often equally interesting to look at corporations because corporate hubris typically drives decision-making in the real economy during the late stages of an economic cycle. Corporations’ budding enthusiasm as the cycle matures leads them to increase their operating leverage and raise fixed-costs. Operating leverage generally increases firms’ sensitivity to the economy, and smaller changes in demand have a magnified effect on profits. During a slowdown, increased operating leverage amplifies a slowdown in profits which then results in layoffs, plant closings, and the drawdown of inventories.

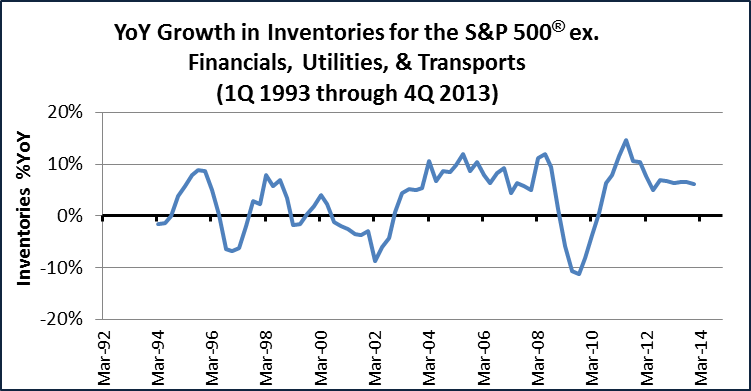

Corporations have been very conservative so far in this cycle regarding increasing fixed costs. Although merger and lending activity has recently picked up, uncertainty over the past several years has curtailed the normal cyclical corporate hubris. Such reserve could ultimately be a very healthy contributor to an elongated economic cycle. Chart 1 shows that corporations are not building excessive inventories. This suggests that the quality of earnings is probably quite good, and decreases the probability of an inventory-led recession (i.e., producing goods that can’t be sold and hindering future production).

Chart 1:

Source: Richard Bernstein Advisors LLC, Standard & Poors’ *S&P 500 excluding those stocks in the GICS financials, utilities and transports sectors/industries. For Index descriptors, see "Index Descriptions" at end of document.

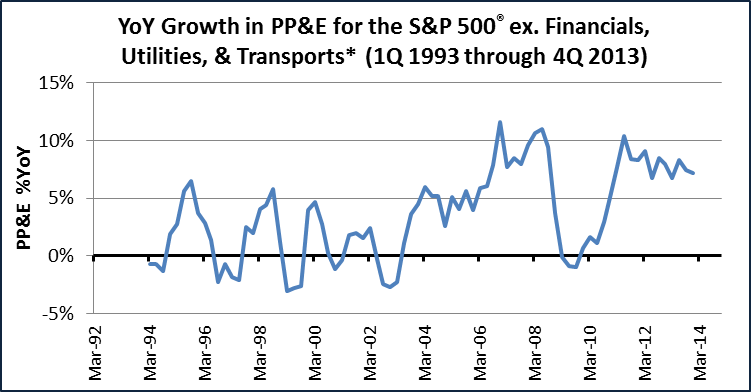

Chart 2 demonstrates that corporations are not yet building excess capacity. Property, plant, and equipment (PPE) growth, while above average, is hardly extreme and has slowed some.

Chart 2:

Source: Richard Bernstein Advisors LLC, Standard & Poors’

*S&P 500 excluding those stocks in the GICS financials, utilities and transports sectors/industries.

For Index descriptors, see "Index Descriptions" at end of document.

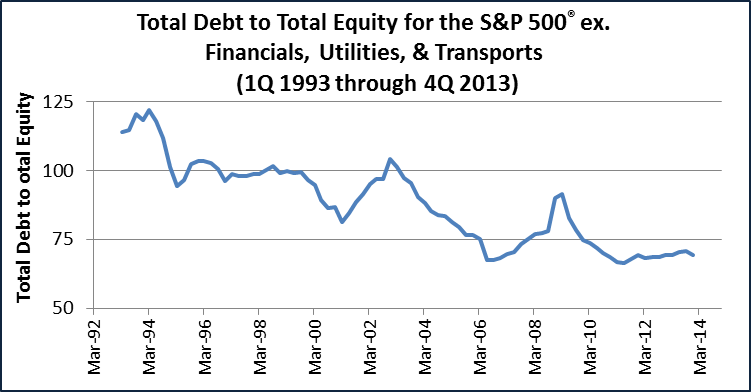

Chart 3 highlights that corporations are not using excessive leverage to finance PPE and inventory expansion. Debt/equity ratios seem quite conservative relative to history.

Chart 3:

Source: Richard Bernstein Advisors LLC, Standard & Poors’ *S&P 500 excluding those stocks in the GICS financials, utilities and transports sectors/industries. For Index descriptors, see "Index Descriptions" at end of document.

Uncertainty = OpportunitySM

RBA’s corporate motto is Uncertainty = OpportunitySM. Certainty implies risks not anticipated, and potential disappointment. Uncertainty, however, often suggests higher-than-normal risk premiums and investment opportunity.A broad swath of data, whether focused on investors or corporations, continues to suggest meaningful uncertainty. Accordingly, we continue to believe this may be an elongated cycle that still offers unrecognized investment opportunities.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

S&P 500®: Standard & Poor’s (S&P) 500® Index. The S&P 500® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment's value. Past performance is, of course, no guarantee of future results. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.

About Richard Bernstein Advisors:

Richard Bernstein Advisors LLC is an independent investment adviser. RBA partners with several firms including Eaton Vance Corporation and First Trust Portfolios LP, and currently has $3.3 billion collectively under management and advisement as of June 30, 2014. RBA acts as sub‐advisor for the Eaton Vance Richard Bernstein Equity Strategy Fund and the Eaton Vance Richard Bernstein All‐Asset Strategy Fund and also offers income and unique theme‐oriented unit trusts through First Trust. RBA is also the index provider for the First Trust RBA American Industrial RenaissanceTM ETF and the First Trust RBA Quality Income ETF. Additionally, RBA runs ETF asset allocation SMA portfolios at UBS and Merrill Lynch and on select RIA platforms. RBA's investment insights as well as further information about the firm and products can be found at

www.RBAdvisors.com.

© Richard Bernstein Advisors

Read more commentaries by Richard Bernstein Advisors