Money Market Reform: Reflections on This Critical Inflection Point for Cash Liquidity Investing

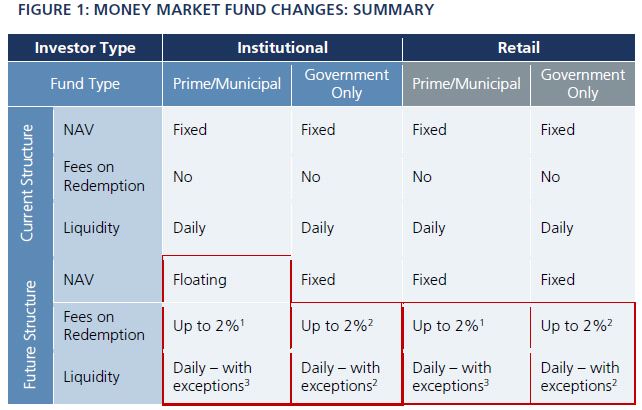

Under the SEC’s new regulations, institutional prime and institutional municipal money market funds will transition to a floating net asset value.

All money market funds (except government-focused funds) are required to impose liquidity fees and may use redemption gates if liquid assets fall below certain levels.

Investors, both institutions and individuals, should view this industry inflection point as an opportunity to revisit their approach to cash investing.

Actively managed short duration strategies are a compelling solution.

On July 23, the Securities and Exchange Commission (SEC) formally approved additional reforms for money market funds. These changes will directly impact institutional investors and definitively alter the dynamics of liquidity markets.

The reforms serve as a reminder of the challenges associated with investing and managing liquidity. These changes to near-zero-yielding “safe” money market funds should motivate investors to think broadly about efficient liquidity investing and to consider other opportunities to earn more attractive yields by putting their cash to work in solutions such as actively managed short-duration fixed income strategies.

Changes to money market funds and timeline for implementation

As many investors are aware, during the 2008 financial crisis, a large money market fund, the Reserve Primary Fund, faced losses on its debt securities after the bankruptcy of Lehman Brothers and fell below a net asset value (NAV) per share of $1, or “broke the buck.” That led to widespread money market fund redemptions and prompted the U.S. Treasury and the Federal Reserve to step in to make sure money market funds could pay in full all withdrawing investors. Since then, the SEC has focused on implementing changes in money market fund structure intended to prevent similar issues, leading to the newly announced changes on July 23, which we believe are the most significant to date.

The SEC decided to implement an approach that combines 1) a move from a fixed $1 NAV to a floating NAV for institutional prime and institutional municipal money market funds and 2) liquidity fees and redemption gates on all non-government money market funds.

• Floating NAV requirement: Institutional prime and institutional municipal money market funds will be required to float the value of their share price versus a current fixed NAV. Exempted from this rule will be

- Retail money market funds: The new rule defines “retail” as funds that have policies and procedures reasonably designed to limit investors to “natural persons.”

- Government money market funds: The new rule defines “government money market funds” as funds that invest 99.5% (formerly 80%) or more of total assets in cash, government securities and repurchase agreements collateralized with government securities or cash.

Why did the money market fund reform specifically highlight prime money market funds? It was in recognition of the fact that credit exposure can have a material impact on the $1 NAV. Therefore, the SEC is sending a clear message that credit risk in regulated institutional money market funds needs to be monitored more robustly.

• Liquidity fees and redemption gates: The rule contains provisions that affect both retail and institutional funds.

• Liquidity fees

- Non-government money market funds would be allowed to impose a liquidity fee of up to 2% if the fund’s level of “weekly liquid assets” were to fall below 30% of total assets.

- Non-government money market funds would be required to impose a 1% liquidity fee if the fund’s level of “weekly liquid assets” were to fall below 10% of total assets.

• Redemption gates

- A fund’s board of directors would be permitted to temporarily suspend redemptions if a fund’s level of “weekly liquid assets” were to fall below 30% of total assets. Gates would be permitted for up to 10 business days, but would be limited to 10 business days in any 90-day period.

The SEC approved additional reforms that include 1) enhanced disclosure of various events, such as gates or sponsor support 2) tightening of diversification requirements and 3) strengthening of stress testing. In addition to the SEC rulemaking, the Department of the Treasury and the Internal Revenue Service are expected to adopt new regulations that minimize the tax and accounting impact of a floating NAV on shareholders.

These changes represent an inflection point in liquidity management, particularly for institutional investors who must now determine whether a floating NAV fits their guidelines and goals. The challenge that remains for all investors, however, is designing an effective cash management strategy in an environment where yields are low and expected to remain that way.

For institutional investors without the need for a fixed NAV, now is the time to revisit cash management strategies and allocations. We believe there are strategies beyond money market funds that offer more attractive risk/reward profiles than money market funds (discussed in more detail below).

Institutional investors that require a fixed NAV may migrate to government-only money market funds. Based on increased demand, however, we believe these funds 1) will offer even more compressed returns as demand for a limited universe of securities spikes and 2) may be forced to close to new investors if faced with outsized demand and limited supply of investable assets. Therefore, even for investors who have historically been attracted to funds with fixed NAVs, we suggest using this reform as a catalyst to reexamine the use of money market funds.

The reform affects retail investors as well. Retail investors will retain the ability to invest in fixed NAV money market funds, but the liquidity of these strategies may be impacted by the possibility of liquidity fees and redemption gates. Investors should closely consider these tradeoffs. These funds continue to yield near-zero percent even after fee rebates, primarily due to their constrained investment guidelines.

How should investors evaluate various alternatives to money markets?

Understanding that some investors may still wish to allocate to money market funds, we suggest accompanying this allocation with a more dynamic approach to create a diversified cash management strategy.

Historically, investors have been slow to react to changing conditions due to competing priorities, or because government and money market fund yields were sufficient to meet liquidity needs. Low rates combined with the new regulations will create challenges for cash investors, so a focus on efficient cash management will be critical.

So what is the best approach?

As a first step, it is crucial to work with partners who have expertise in the ever-changing cash market. Cash management is not as simple as it once was. It now entails creating a comprehensive, proactive strategy to meet an investor’s unique needs.

Investment options to consider in this evaluation include:

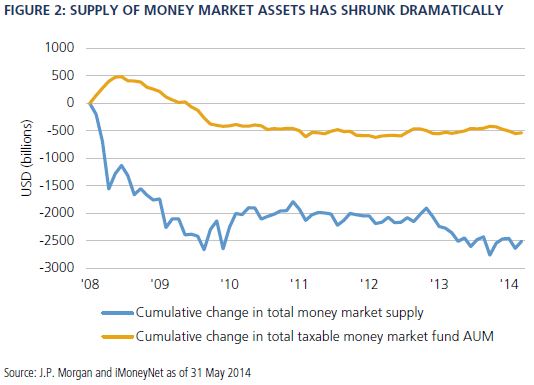

• Money market funds: While the fixed NAV is an attractive characteristic for some, it comes with a price: near-zero returns. This will only be exacerbated as institutional investors pile into government money market funds following the new reforms.The Crane Money Fund Average indicates that the category as a whole is already yielding only 1 basis point after fees. With approximately $2.5 trillion in assets under management, these funds must compete for the same assets, resulting in a “race to the bottom,” which props up prices and suppresses yields (see Figure 2).

Moreover, these funds are exposed to some degree of credit risk, and with yields so low, investors are not compensated for this risk. This also raises the question: Do all investment managers have the necessary staff to monitor these credit risks?

• Certificates of deposit and bank deposits: Some investors may turn to banks offering certificates of deposit (CD) or rates on deposits. While these do offer liquidity and stable value, there are drawbacks. First, if deposits are uninsured, investors are taking on concentrated credit risk with the bank for which they are not compensated. Second, CDs often include a penalty for early withdrawal, limiting their true liquidity.

• Short-duration strategies: We believe that active and well-diversified short-duration strategies best enable investors to escape the near-zero returns in money market funds. They are also much more flexible than passive short-duration strategies, including passive funds and index ETFs. This means active portfolio managers can identify areas of value across sectors, quality and geographies to manage risk, liquidity and NAV stability.

Passive strategies invest exclusively in the securities in their benchmarks, leaving them at risk of not being able to respond to changes in the market, thus limiting their potential benefits.

Passive short-duration strategies are designed to offer investors returns close to their benchmarks, but active short-duration strategies offer a unique proposition: They aim to achieve returns above their benchmarks by investing in high quality, short-term securities; investors thus gain upside potential in exchange for slightly higher risk than money market funds.

Indeed, in The New Neutral world, where we expect policy rates to remain low for an extended time, investors need active and flexible strategies that provide the opportunity for positive real returns while focusing on preserving capital. PIMCO developed the Short Asset Investment Strategy specifically to meet this need; it aims to identify opportunities just beyond the money market space while seeking to limit market value fluctuation. In doing so, it retains the ability to potentially capture upside opportunities while still working to protect on the downside. This is just one of several cash management strategies that PIMCO manages.

Conclusion

The SEC’s long-awaited reforms to money market funds have arrived, and they will change the cash management landscape. Investors should use this inflection point in liquidity management to re-examine their use of cash management strategies. There are attractive opportunities for investors – both retail and institutional – who allocate to strategies best suited to their needs and risk tolerance.

Past performance is not a guarantee or a reliable indicator of future results. All investmentscontain risk and may lose value. Money Market funds are not insured or guaranteed by FDIC or any other government agency and although the funds seek to preserve the value of your investment at $1.00 per share, it is possible to lose money by investing in money market funds. Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. Sovereign securities are generally backed by the issuing government. Obligations of U.S. government agencies and authorities are supported by varying degrees, but are generally not backed by the full faith of the U.S. government. Portfolios that invest in such securities are not guaranteed and will fluctuate in value. The credit quality of a particular security or group of securities does not ensure the stability or safety of the overall portfolio.

There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest long-term, especially during periods of downturn in the market. It is not possible to invest directly in an unmanaged index.

This material contains the opinions of the author but not necessarily those of PIMCO and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark or registered trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. THE NEW NEUTRAL and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Pacific Investment Management Company LLC in the United States and throughout the world.

©2014, PIMCO.

© PIMCO