We will be hosting a live webinar and Q &A with Richard Bernstein and Jeffrey Gundlach on Oct. 14. To register, you must be an APViewpoint member. To attend these events, join or login to APViewpoint today and click on the APVIEWPOINT EVENTS link on the lower left-side navigation pane.

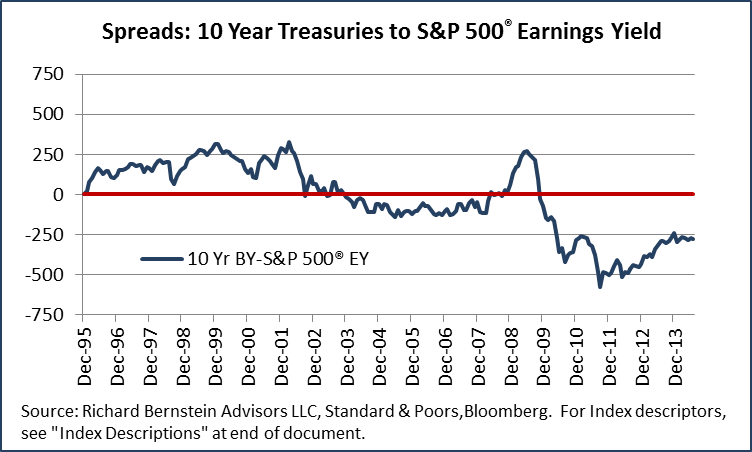

The track record of the so-called “Fed Model” is dubious at best. The relationship compares the S&P 500®’s earnings yield to the yield of the 10-year Treasury note, and there are many other indicators that have a better track record than does the Fed Model when attempting to predict twelve-month forward returns.

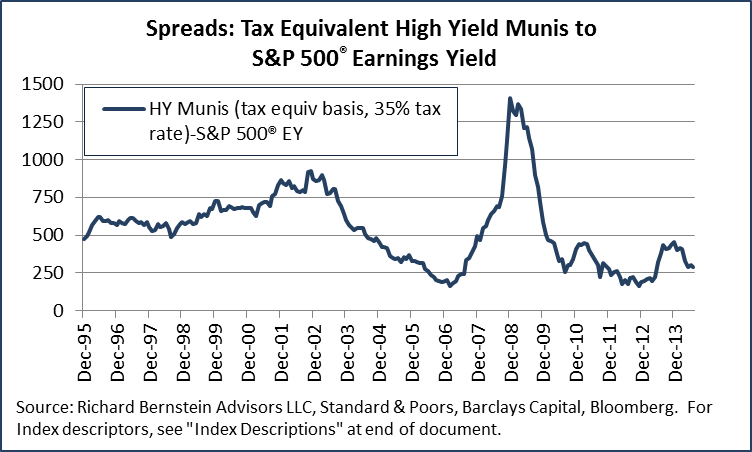

Despite that caveat, we nonetheless thought it interesting to examine the yield relationships between stocks and a broader array of fixed-income categories. Among those categories, high yield municipal bonds seem to be the only fixed-income that is attractive relative to stocks.

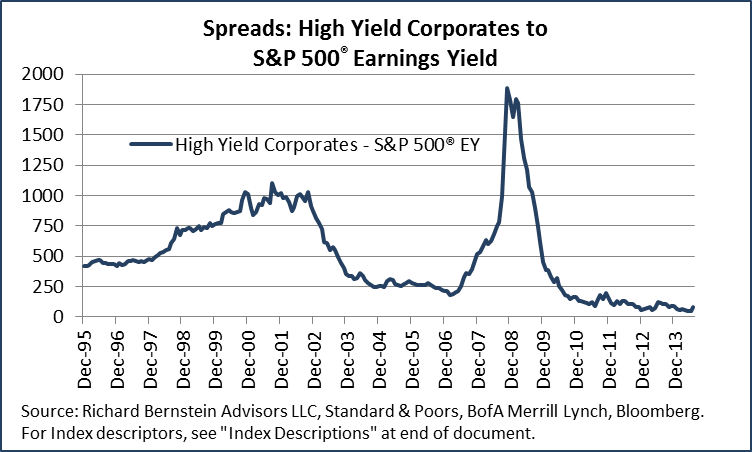

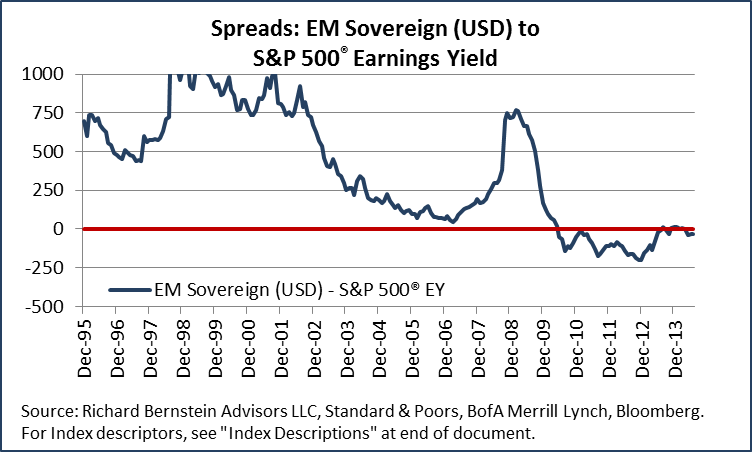

The charts in the appendix show the spreads between the yield on a fixed-income asset class and the earnings yield of the S&P 500®. If the spread is positive, that suggests that the fixed-income asset class is more attractive than are equities. If the spread is negative, it suggests equities are more attractive.

Several points are worth considering:

- As many have discussed for years, stocks appear attractive relative to treasuries. No new information there.

- High yield municipal bonds are very attractive, on a yield comparison basis, relative to equities. We continue to believe that high yield munis are very attractive because the asset class is very “equity-like” (meaning very sensitive to the economy) and it offers a tax-equivalent yield that is roughly three percent higher than the S&P 500®’s earnings yield.

- High yield corporates now have virtually no yield advantage to equities, which argues that one should prefer equities to high yield corporate debt. The debt doesn’t offer higher yields, and high yield corporates’ capital appreciation potential is typically muted relative to equities’.

- Despite investors’ enthusiasm for the asset class, sovereign debt seems remarkably unattractive. Investors seem to be over-estimating the risks associated with high yield munis, but under-estimating the risks of non-US debt. That may be especially true within the context of an appreciating US dollar.

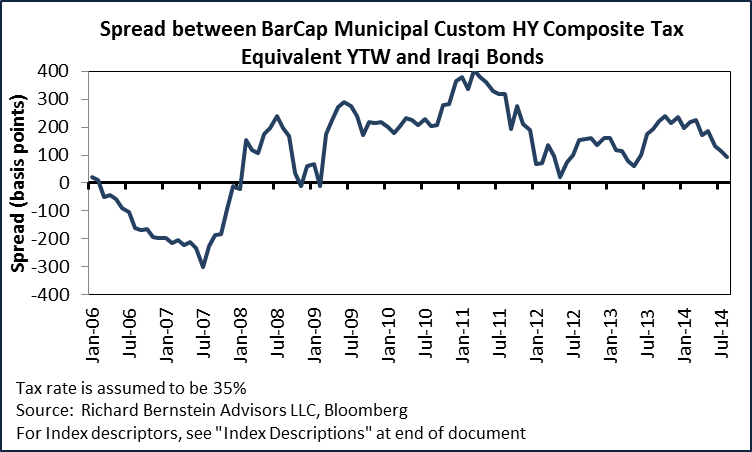

Which is riskier: Iraq bonds or high yield munis?

As mentioned, investors may be underestimating the risks of non-US debt and over-estimating the risks associated with high yield munis. Through time we have found some startling mispricings between these two asset classes. Our current example certainly fits that description.

Iraq is in the midst of a serious and growing civil war but, as Chart 1 highlights, US high yield munis as an asset class currently trade with a spread more than 150 basis points OVER Iraq! The bond market seems to feel that the diversified aggregate of US high yield munis is actually riskier than are Iraq bonds. (Note that the durations are roughly comparable).

Chart 1:

Stocks vs. bonds high yield munis

We have argued for several years that the US stock market could be in the biggest bull market of our careers, and we don’t think there are many fixed-income asset classes that are attractive relative to stocks. However, high yield munis are very equity-sensitive and offer attractive yields relative to the stock market. We remain amazed that fixed-income investors, like equity investors, refuse to believe that some of the most attractive investments may be right in their own back yards.

Chart 2:

Chart 3:

Chart 4:

Chart 5:

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

S&P 500®: Standard & Poor’s (S&P) 500® Index. The S&P 500® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

U.S. High Yield Corporates: BofA Merrill Lynch US Cash Pay High Yield Index. The BofA Merrill Lynch US Cash Pay High Yield Index tracks the performance of USD-denominated, below-investment-grade-rated corporate debt, currently in a coupon-paying period, that is publicly issued in the US domestic market. Qualifying securities must have a below-investment-grade rating (based on an average of Moody’s, S&P and Fitch) and an investment-grade-rated country of risk (based on an average of Moody’s, S&P and Fitch foreign currency long-term sovereign debt ratings), at least one year remaining term to final maturity, a fixed coupon schedule, and a minimum amount outstanding of $100 million.

EM Sovereign: The BofA Merrill Lynch US Dollar Emerging Markets Sovereign Plus Index. The BofA Merrill Lynch US Dollar Emerging Markets Sovereign Plus Index tracks the performance of US dollar denominated emerging market and cross-over sovereign debt publicly issued in the Eurobond or US domestic market. Qualifying countries must have a BBB1 or lower foreign currency long-term sovereign debt rating (based on an average of Moody’s, S&P and Fitch). Countries that are not rated, or that are rated “D” or “SD” by one or several rating agencies qualify for inclusion in the index but individual non-performing securities are removed. Qualifying securities must have at least one year remaining term to final maturity, a fixed or floating coupon and a minimum amount outstanding of $250 million. Local currency debt is excluded from the Index.

High Yield Municipals: The Barclays Municipal Custom High Yield Composite Index: The Barclays Municipal Custom High Yield Composite Index is calculated using a market value weighting methodology and it tracks the high-yield municipal bond market with a 75% weight in non-investment grade municipal bonds and a 25% weight in Baa/BBB-rated investment grade municipal bonds for liquidity and balance.

Iraqi Bonds: Republic of Iraq Sovereign, Unsecured, Maturity 01/15/2028, id number EF2306852

10 Year Treasury: US Generic 10-Year Government Yield (bloomberg) Yields are yield to maturity and pre-tax. The rates are comprised of Generic United States on-the-run government bill/note/bond indices.

© Copyright 2014 Richard Bernstein Advisors LLC. All rights reserved.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment's value. Past performance is, of course, no guarantee of future results. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.

About Richard Bernstein Advisors:

Richard Bernstein Advisors LLC is an independent investment adviser. RBA partners with several firms including Eaton Vance Corporation and First Trust Portfolios LP, and currently has $3.3 billion collectively under management and advisement as of July 31, 2014. RBA acts as sub‐advisor for the Eaton Vance Richard Bernstein Equity Strategy Fund and the Eaton Vance Richard Bernstein All‐Asset Strategy Fund and also offers income and unique theme‐oriented unit trusts through First Trust. RBA is also the index provider for the First Trust RBA American Industrial RenaissanceTM ETF and the First Trust RBA Quality Income ETF. Additionally, RBA runs ETF asset allocation SMA portfolios at UBS and Merrill Lynch and on select RIA platforms.