The increasing divergence of US economic growth from the rest of the developed world is making the Federal Reserve's job more difficult. And, in the process, it's creating more uncertainty around when the Fed will begin raising rates and pushing market volatility higher.

Last week, the stock market experienced even wilder swings than the previous week, with the Dow trading down hundreds of points from Monday's highs to Wednesday's lows—then rising by hundreds of points from Wednesday's lows to Friday's highs. And the yield on the 10-year Treasury fell below 2% last week on fears of a slowdown in global growth emanating from Europe.

Despite mounting evidence of acceleration in US economic activity, there are growing concerns that deterioration in the global growth outlook could stifle the US recovery. A 10-year Treasury yield that fell below 2% last week underscores this fear. Plus, economic expectations in the United States have become very optimistic, leaving little room to surprise on the upside.

A Head's Up on Tails

Today, our base case scenario remains intact: We believe the Fed is likely to start raising rates in June 2015. But we also recognize that there is an increasing probability of a wider range of outlier outcomes. Essentially, tails are getting fatter. That's because US economic conditions continue to improve, particularly the job market and consumer sentiment. Last week's data was encouraging: Initial jobless claims came in lower than expected and consumer sentiment jumped to its highest level since 2007 on falling oil prices.

However, we also recognize that downside risks to this scenario have increased given that a global growth deceleration is underway and the dollar is strengthening. It's important to note that consensus US GDP estimates for 2015 still haven't been revised.

Given this backdrop of an improving US economy but greater risks, we're no longer talking exclusively about when tightening will begin. The new wrinkle to the discussion? Whether or not the Fed might embark on QE4 if the US economy decelerates.

Mixed Messages?

As a result, the road ahead is less clear. The gap between Fed projections and markets has significantly widened. And Fed communication has become increasingly confusing. St. Louis Fed President James Bullard actually created more confusion last week by suggesting that the end of quantitative easing should be delayed or the Fed should possibly increase QE, if necessary. At the same time, he said he was uncomfortable keeping the short-term rate at zero if the economy continues to improve.

Meanwhile, Boston Fed President Eric Rosengren said he still expects the Fed to raise rates in 2015, but added that the Fed should consider a fourth round of government bond purchases—if the US economy weakens enough. In fact, there's been a massive reassessment of interest-rate-hike probabilities by money markets and bond markets. However, there haven't been any signs of a change in the path of Fed policy.

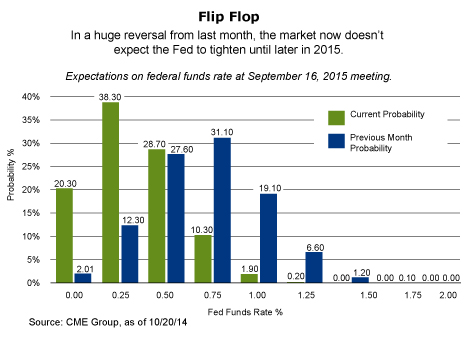

Nevertheless, uncertainty is high. How high? Federal funds futures have dramatically changed in the past week, with most participants predicting that tightening will not begin until September of 2015 or later. We know the market doesn't like uncertainty, particularly on monetary policy, and the fatter tails present a big question mark for investors.

How to Play It

What does this mean for investors? They shouldn't avoid stocks. But they need to recognize that next year won't be easy. Valuations are more attractive than they were just a few weeks ago. What's more, small-cap stocks are actually performing well and have moved away from correction territory. For months, many market watchers have fretted about stocks because of small-cap weakness. A small-cap reversal could bode well for the overall stock market. But most importantly, investors with long time horizons and substantial goals need the upside potential stocks offer.

Still, as we anticipated in our Economics & Strategy forecast, higher volatility will likely be the norm going forward given greater monetary policy uncertainty.

Kristina Hooper, CFP, CAIA, CIMA, ChFC, is US head of investment and client strategies for Allianz Global Investors. She has a B.A. from Wellesley College, a J.D. from Pace Law and an M.B.A. in finance from NYU, where she was a teaching fellow in macroeconomics.

Gross domestic product (GDP) is the value of all final goods and services produced in a specific country. It is the broadest measure of economic activity and the principal indicator of economic performance.

The Dow Jones Industrial Average (DJIA) is a price-weighted average of 30 actively traded blue chip stocks, primarily industrials, but including financials and other service-oriented companies. The components, which change from time to time, represent between 15% and 20% of the market value of NYSE stocks.

The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Past performance of the markets is no guarantee of future results. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities.

A Word About Risk: Equities have tended to be volatile, involve risk to principal and, unlike bonds, do not offer a fixed rate of return. Foreign markets may be more volatile, less liquid, less transparent and subject to less oversight, and values may fluctuate with currency exchange rates; these risks may be greater in emerging markets.

Allianz Global Investors Distributors LLC, 1633 Broadway, New York NY, 10019-7585, us.allianzgi.com, 1-800-926-4456.

AGI-2014-10-20-10801