For some time now we have been making the case for a long-term bull market in U.S. equities. This has rested on the prediction of a gradual economic recovery devoid of inflationary pressures, played out against a very accommodative monetary backdrop. So far, this is exactly what has occurred. But as we all know, trees don’t grow to heaven and nothing lasts forever. Therefore the relevant questions we ask ourselves every day are: (1) what could go wrong and (2) when should we start to worry? We shall devote this quarter’s Outlook to the things we worry about.

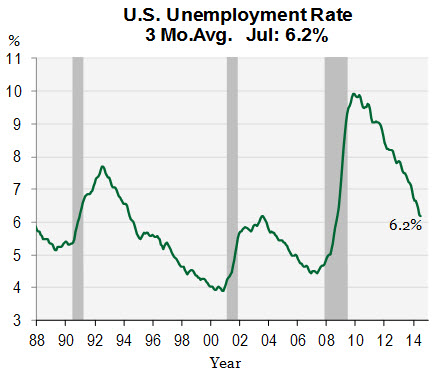

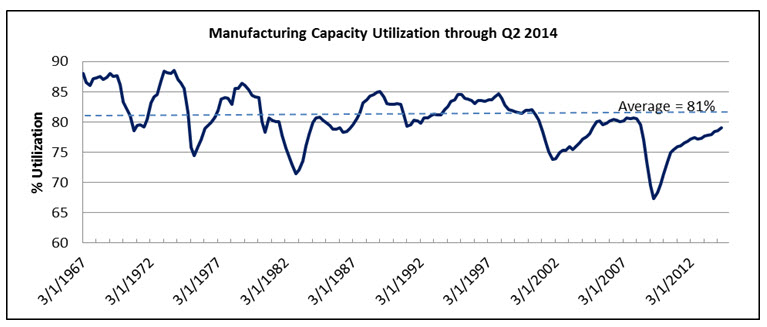

Primary among our concerns would be a sudden and unexpected pick-up in inflation. So far during this recovery there has been enough slack in the U.S. economy, especially in the labor markets and in terms of capacity utilization, that the recovery has not sparked wage and price inflation. The deep recession in 2008/2009 drove unemployment up and capacity utilization down. Now, however, after over five years of slow but grinding recovery unemployment has dropped to levels that historically have triggered wage inflation, and capacity utilization has jumped back close to its historical average (Figures 1 & 2). There are now scattered reports of labor shortages and wage pressure in certain professions, such as welding, but these instances appear to be industry- and geography-specific and not yet generalized. A recent report noted that new jobs created since the 2008 debacle pay 23% less than the jobs lost in the downturn.1 Regardless of its accuracy, this statistic is consistent with anecdotal reports of lower- and middle-class economic stagnation and financial stress continuing despite the economic expansion. If, when and how fast labor markets may tighten is a key risk. Our bet is that it’s a ways off and not a sure thing in the next 12-18 months.

Figure 1:

Source: Cornerstone Macro. Data from 1/1/1988 – 12/31/2015. Data after 8/1/2014 are estimated. Shaded areas represent times of recession.

Figure 2:

Source: Bloomberg (Data from 3/1/1967 - 6/30/2014).

The other potential source of inflationary pressure (other than monetary conditions) would be commodities. Fortunately the slowdown in China’s growth, coupled with recessionary conditions in Europe, has resulted in price weakness in many key commodities as well as strength in the U.S. dollar. Some economists suggest that the transition in China from investment led growth (infrastructure, real estate and factories) of the past 20 years to services led/consumer growth spells the end of the commodity super cycle of the past 15 years. Overlaying a stronger U.S. dollar on looser commodity markets suggests that commodity prices could stay weak for U.S. consumers and manufacturers for an extended period of time. So, we do not see inflation pressures building here. Additionally, the strengthening U.S. dollar is helping to hold-down the cost of imports for all goods, not just commodities.

The second risk revolves around weak economic conditions abroad. Europe is beset by slow growth at best and actual recession at worst, Brazil is in outright recession and China’s growth is slowing. With our trading partners suffering from economic anemia, there is concern that the U.S. could follow suit. Maybe, but recent data suggest the U.S. economy is actually accelerating and does not depend too much on trade. In fact over 70% of U.S. gross domestic product (GDP) is driven by U.S. consumers, with exports making up just 14% of GDP.

The third most obvious risk is that our “easy money” policies eventually have to give way to more neutral or even tight policies, and this will likely remove the high-octane fuel behind the stock market’s upward trajectory. We have long contended that the Federal Reserve (the “Fed”) will probably “taper” in concert with the economic recovery, i.e. the degree of tapering should be proportionate to the strength of the recovery. We have not yet entered the first phase of rising rates where the Fed raises rates to get back to normal levels, and we feel we are far from the second phase where they raise rates to slow down the economy. Inflation does not appear to be a problem that the Fed needs to fight just now. As long as inflation remains benign, the return to monetary neutrality should not derail the stock market. If inflation becomes a problem, then, and only then, should one worry about Fed tightening. In other words, “tapering ain’t tightening.”

Fourth, we worry about geopolitical risks spiraling out of control and wreaking havoc on the world’s economy. But geopolitical risks are a bit like germs; they are always out there, and sometimes they knock you down, but they are rarely fatal.

The fifth risk we worry about is rather amorphous and difficult to quantify. We have long contended that if you want to know where the next big crisis will erupt, look to see who has been borrowing the most money. For example, look at housing debt during the 2005-2007 period. What followed was, of course, the housing debacle of 2008. Since 2008 the biggest net borrowers have been central governments. In the U.S., government deficits have been shrinking rapidly. However, central governments elsewhere in the world are still running large deficits. How long this can go on is anybody’s guess.

Finally, a number of investors worry that stock market valuations have become stretched and are vulnerable to a setback. We have argued for some time that valuations – i.e. conventional price-to-earnings (P/E) ratios – are reasonable and have been hovering just above the long-term average. Given the current low level of interest rates, one would actually expect the market’s (as measured by the S&P 500 Index) P/E to be higher; roughly double where it is today. So, the market is either discounting higher interest rates and is therefore not likely to be vulnerable to Fed tapering, or it is discounting a future drop in corporate profits, or some combination of the two. If none of these turn out to be the case, then the market may be significantly undervalued.

One school of investors looks not at the conventional P/E ratio, but at the Cyclically Adjusted Price-to-Earnings ratio (CAPE). CAPE is a P/E ratio calculated on the market’s trailing 10 years’ earnings. It may be somewhat useful in forecasting long-term market returns. People believe the higher the CAPE, the lower the market’s expected return over the next 10 years, and vice-versa. But CAPE is a very poor timing indicator. In other words, a high CAPE does not indicate an imminent market crash, just as a low CAPE does not mean a bull market is about to jump out of the starting blocks. CAPE is high right now relative to the average CAPE of the past 100 years. Some say this is because the last 10 years included the debacle of 2008 and its aftermath. Others point out that current earnings may be biased downward by the way tech companies account for option grants and that tech represents an ever-increasing share of the overall market. Still others point out that S&P earnings have been hit by huge write downs at a few companies. Using a different measure of profits, which adjusts for such write downs, would likely show a much lower CAPE.

Our view is that low interest rates should bias CAPE upwards, just as it should raise the conventional P/E ratio. Using a CAPE average over 100 years is not terribly meaningful to us as there have been long periods when interest rates were high and equity valuations low (not just CAPE measures of value, but all measures). We prefer to look at the past 25 years as a period when interest rates and inflation have fallen from much higher post-World War II levels. The CAPE valuation is currently in line by that measure (Figure 3).

Figure 3:

Source: Bloomberg and Cornerstone Macro LP (Data from 1/29/1988 - 9/30/2014).

Without belaboring the point, we believe that market valuations are currently reasonable, and that if corporate profits grow over the next few years, the stock market is likely to rise in tandem. To the extent that we are able to identify companies with depressed valuations and accelerating earnings and cash flows, we strive to be able to produce reasonable investment returns.

We thank you for your continued confidence in our management.

Sincerely,

John Osterweis

Matt Berler

[1] Megan Davies, “U.S. jobs rose since ’08 crisis, but pay is 23 pct less: report” Thomson Reuters online – August 11, 2014

____________________

Past performance is no guarantee of future results.

This commentary contains the current opinions of the author as of the date above, which are subject to change at any time. This commentary has been distributed for informational purposes only and is not a recommendation or offer of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but is not guaranteed.

Price-to-Earnings (P/E) ratio is the ratio of the stock price to the trailing 12 months diluted EPS.

CAPE Ratio (also known as the Shiller Ratio): Cyclically Adjusted Price-to-Earnings Ratio. The numerator of the CAPE is the real (inflation-adjusted) price level of the S&P 500 Index and the denominator is the moving average of the preceding 10 years of the S&P 500 Index’s real reported earnings, where the U.S. Consumer Price Index is used to adjust for inflation.

The S&P 500 Index is an unmanaged index that is widely regarded as the standard for measuring large-cap U.S. stock market performance.

This index reflects the reinvestment of dividends and/or interest income and is not available for investment.

Cash Flow measures the cash generating capability of a company by adding non-cash charges (e.g. depreciation) and interest expense to pretax income.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock.

One cannot invest directly in an index. [11233]

© Osterweis Capital Management

© Osterweis Capital Management