Heading down the homestretch in 2014, there are some market drivers that warrant close attention. Here are the five E’s for investors to watch:

1. Elections. While many market observers view the energy sector as the biggest beneficiary of mid-term election results, we believe business sentiment is the real winner. Over the past few years, we’ve heard repeatedly that corporate leaders were reluctant to spend, particularly on hiring new employees, because they feared greater regulation. But the mid-term election results should ease their concerns, as US companies are now likely to have a more business-friendly environment. That should be good for both spending and hiring.

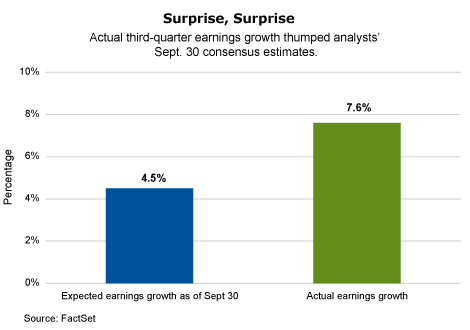

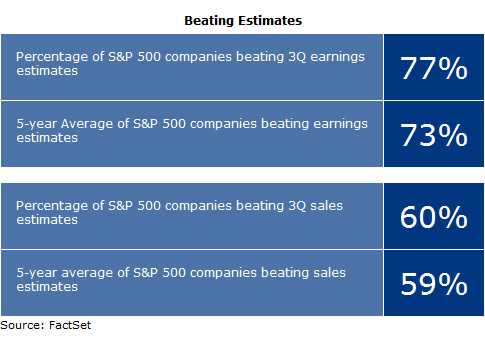

2. Earnings. Third-quarter earnings have been better than expected. Of the 446 companies in the S&P 500 that have reported earnings to date for the quarter, 77% have reported earnings above the mean estimate. And 60% have reported sales above the mean estimate. Back on Sept. 30, the estimated earnings growth rate for the third quarter was 4.5%. Today, the earnings growth rate for the third quarter is 7.6%. Nine of the 10 sectors reporting earnings have higher growth rates today than they did on Sept. 30 due to upside earnings surprises. We’re optimistic that fourth-quarter earnings will be at least slightly better than expected too.

“Nine of the 10 sectors reporting earnings have higher growth rates today than they did on Sept. 30 due to upside earnings surprises.”

3. Employment. The October jobs report underscores that the labor market is firmly in recovery. At 5.8%, the current unemployment rate is now equal to the long-term average since 1948. There are still flaws in the employment situation but even those trouble spots have been slowly improving. For example, U-6, the broadest measure of unemployment, has edged down to 11.5% from 11.8%. Overall, median income fell 5% between 2010 and 2013, while mean income increased 4%. According to the Federal Reserve, the decline in median income coupled with the rise in mean income is “consistent with a widening income distribution during this period” which was also seen in the preceding three-year period, 2007–2010. However, this trend is “in stark contrast to a pattern of substantial increases in both the median and the mean dating back to the early 1990s.”

Interestingly, Americans’ desire for higher wages and less disparity in personal income were also seen in the results from last week’s election. Even though we saw a Republican sweep in the election, key red states embraced higher minimum-wage laws by wide margins. Look for more focus, particularly from lawmakers, on improving wage growth and rectifying income inequality going forward. And look for the Fed to remain relatively accommodative.

4. Energy. There are disadvantages to lower energy prices, namely reduced capital expenditures by energy companies, which comprise approximately 15% of total capex spending. However, we believe the drawbacks are more than outweighed by the advantages. Specifically, consumers are likely to spend more because lower energy prices are like an unexpected pay hike.

“… consumers are likely to spend more because lower energy prices are like an unexpected pay hike.”

In addition, many industries—from manufacturing to airlines—are also benefiting from lower input costs. And while capex spending from the energy industry is likely to slow, don’t expect it to dry up entirely. Keep in mind that different oil companies have very different break-even points, ranging from slightly over $40 per barrel to approximately $180 per barrel, although the average hovers near $80. The decision to reduce capex will be made by each company based on its own break-even point as well as its projection on how long it will take for oil prices to rise.

“… we expect continued volatility, rotations in sector leadership and a ‘two steps forward, one step back’ pattern.”

5. Expectations. It seems that high expectations are priced into US stocks, so we don’t anticipate dramatic gains any time soon. However, we expect continued volatility, rotations in sector leadership and a “two steps forward, one step back” pattern. This will likely mean a gradual climb higher for US stocks but some nail-biting moments along the way.

Kristina Hooper, CFP, CAIA, CIMA, ChFC, is US head of investment and client strategies for Allianz Global Investors. She has a B.A. from Wellesley College, a J.D. from Pace Law and an M.B.A. in finance from NYU, where she was a teaching fellow in macroeconomics.

Past performance of the markets is no guarantee of future results. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities.

A Word About Risk: Equities have tended to be volatile, involve risk to principal and, unlike bonds, do not offer a fixed rate of return. Foreign markets may be more volatile, less liquid, less transparent and subject to less oversight, and values may fluctuate with currency exchange rates; these risks may be greater in emerging markets.

The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Allianz Global Investors Distributors LLC, 1633 Broadway, New York NY, 10019-7585, 1-800-926-4456.

AGI-2014-11-10-10997