Southeast Asia represents one of the fastest-growing regions in the world today, and is one that we are excited about as investors. The Templeton Emerging Markets Group held our semiannual analyst conference in Jakarta in September, and one of the key reasons for choosing that location was to observe and discuss the changes and challenges on the ground with the new regime of President Joko Widodo. I’ve invited my colleague Tek Khoan Ong to pen some thoughts on the outlook and investment opportunities in Indonesia today.

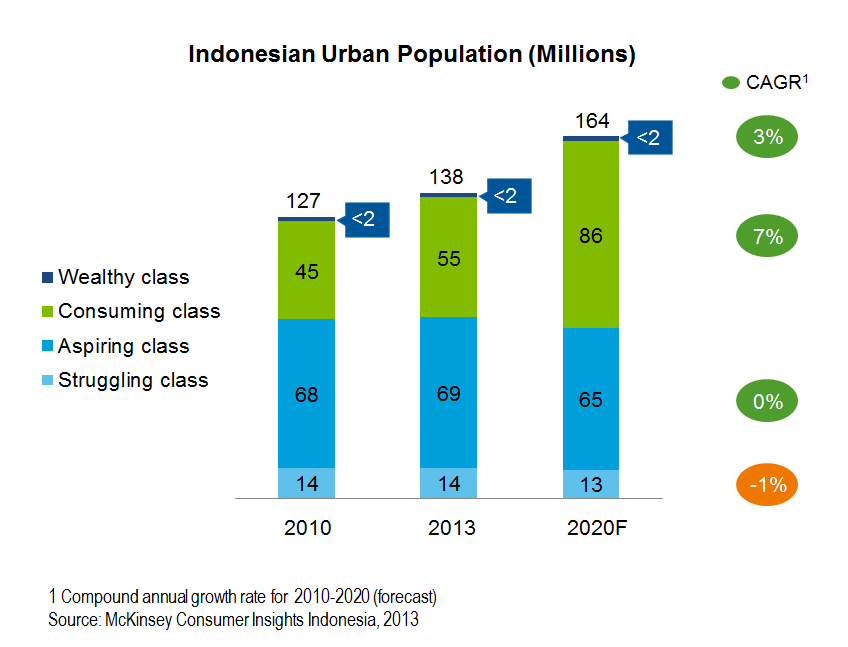

As investors in Indonesia, we think there is much to be excited about. Indonesia has a large and young population that is fast-urbanizing and, hence, fueling growth in income and consumption. It has the world’s 4th largest population of more than 240 million (5th largest considering the European Union as a whole, as of 2013), more than 40% of which are younger than 25 years old.1 Indonesia’s resource-rich economy is the 16th largest in the world, and it could become the 7th largest by 2030, if the economy’s GDP growth trend of 5-6% per annum continues.2 Indonesia’s urban population of 110 million alone is expected to increase to over 200 million by 20303 and consumer spending is increasing rapidly among the estimated 45 million middle-income Indonesians.4 It means by 2030, Indonesia’s economic strength could even overtake the economies of all EU countries, including Germany and the United Kingdom.

As the largest nation in Southeast Asia by population, we believe Indonesia’s growing prosperity will benefit the region as a whole.

High Hopes for The People’s President

Voted in as the “people’s president” based on his humble background and his strong track record as mayor of Solo and governor of Jakarta, there are high expectations that President Joko Widodo (or “Jokowi” as he is popularly known) will be able to replicate his successes in those cities nationwide. We believe he has his heart and intentions in the right place and has a good core team to help him, but there will likely be speed bumps along the way. Regarded as a political outsider, Jokowi faces a number of challenges, which include dealing with his own party, the Indonesian Democratic Party-Struggle (PDI-P), and a fragmented Parliament. A case in point is the selection of his Cabinet; a practical combination and one of the stronger governance teams in years—but with some members not his first choice. Then there are issues of corruption and a slowing economy with a twin (fiscal and current account) deficit. But Jokowi’s biggest challenge is probably meeting the expectations of the Indonesian people.

Fuel subsidies, one legacy of former President Suharto, have been a subject of hot debate within the new regime. Fuel subsidies total about US$20-25 billion a year, or roughly 20% of Indonesia’s budget, compared with just about 10% for infrastructure and 5% for health care.5 The fuel subsidy, when introduced, was meant to benefit the poor, but it has also benefited the rich so it is a blunt tool. In our view, reducing fuel subsidies should help Indonesia reduce its fiscal deficit and better allocate funds for much-needed reforms in infrastructure, health care and education. There had been previous fuel price hikes in fiscal years, 2005/2006 and 2008/2009, as well as most recently in 2013. Such price hikes have been accompanied by monthly cash subsidies to the poorest households for 2-9 months. In our view, any political fallout from such a reduction or removal should be temporary, especially given the president’s popularity and his ability to engage the masses.

Corruption and Bureaucratic Inefficiency: More Work to Be Done

Indonesia has made inroads in addressing corruption with the establishment of the anti-corruption commission, officially named Komisi Pemberantasan Korupsi (KPK). Established by law in 2002, the KPK is modeled after Hong Kong’s Independent Commission Against Corruption (ICAC). KPK has prosecuted hundreds of cases with an excellent success rate, including successful cases against the chief justice of an Indonesian constitutional court, and the police inspector-general. Prominent businessmen, ministers and even former President Susilo Bambang Yudhoyono’s son have not been immune to investigation. We think much still needs to be done, as law enforcement is weak and coupled with regional autonomy, widespread corruption continues. We believe President Jokowi will need to continue to support and strengthen the efforts of the KPK. Recognizing that reducing corruption will require a change in mindset, President Jokowi is introducing a mental revolution in the education system, whereby the emphasis from a young age and in primary school will be on character building.

Addressing bureaucratic inefficiencies will need to take several forms, in our view. These include hiring capable people and putting in place a merit-based performance appraisal system, including better accountability and key performance indicators, as well as impromptu visits from senior officials, more online systems to improve transparency and fairness, and budget allocation based on targeted priorities.

The Investment Outlook

The Indonesian stock market has been performing quite well this year on the heels of strong performance in 2013, some of which has been tied to reform optimism with the new regime. President Jokowi is a change from all past presidents since Indonesia gained independence in 1945. Hence, we think some degree of optimism is justified, although as mentioned earlier, it will not be without hurdles. Given the performance of the market, it is indeed more expensive today than a year or two ago. However, we do not believe Indonesia’s market is overvalued yet, provided the macroeconomic environment remains stable.

We are finding potential investment opportunities in many sectors that benefit from existing demographics and expected reforms. These includes banks, which lend to both fast-growing corporates and provide mortgages, credit cards and other retail banking products to consumers, and companies in the consumer, resources and infrastructure-related sectors.

We also think there is room for equity investing to grow its domestic base. Indonesia historically has had high interest rates and inflation rates. As such, many Indonesians prefer to leave their savings in cash and deposits given the high returns, or invest them in properties as an inflation hedge. The fact that many Indonesian investors lost money in the stock market during the Asian crisis in 1997-1998 did not help the perception of the equity asset class. While equities may come with volatility, we think this is an attractive asset class over a mid- to long-period of time. For instance, over the past 10 years, the Jakarta Composite index (JCI) has delivered an annual return in US dollar terms of just under 20% per annum.6 We believe that with more investment education, a younger investing community, and a lower and more stable interest rate and inflation environment, there will eventually be more interest in equities, and in Indonesia, among the global investment community at large.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

The comments, opinions and analyses expressed by the individuals herein are personal views and are intended to be for informational purposes and general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. The information provided in this material is rendered as at publication date and may change without notice and it is not intended as a complete analysis of every material fact regarding any country, region market or investment.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton Investments (“FTI”) has not independently verified, validated or audited such data. FTI accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user. Products, services and information may not be available in all jurisdictions and are offered by FTI affiliates and/or their distributors as local laws and regulation permits. Please consult your own professional adviser for further information on availability of products and services in your jurisdiction.

What Are the Risks?

All investments involve risks, including possible loss of principal. Foreign securities involve special risks, including currency fluctuations and economic and political uncertainties. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets.

© Franklin Templeton Investments