- Tactical decisions regarding the scaling of an LDI allocation cannot be based solely on Treasury market dynamics. Credit market considerations including valuations, fundamentals and technicals within that sector must be considered.

- Given recent underperformance of long credit relative to intermediate credit, LDI investors should consider increasing long credit exposure.

- A structured approach that combines rigorous top-down macroeconomic-analysis to take views on duration and credit sectors with equally thorough bottom-up credit research to identify companies where fundamentals are improving may deliver alpha that can help clients reduce their funding mismatch over time.

As long-dated interest rates remain low by historical standards, defined benefit plan sponsors may be tempted to delay increases in liability-driven investment (LDI) credit allocations or even scale back on current exposure. Before reaching that conclusion it is important to differentiate credit spread in a long maturity corporate bond from the Treasury yield.

Liabilities for U.S. corporate defined benefit plans are driven by high quality corporate bond rates: Consequently, an attractive hedge or LDI asset is a long duration credit bond. Therefore, tactical decisions regarding the scaling of an LDI allocation cannot be based solely on Treasury market dynamics. Credit market considerations including valuations, fundamentals and technicals within that sector must be considered.

Valuation

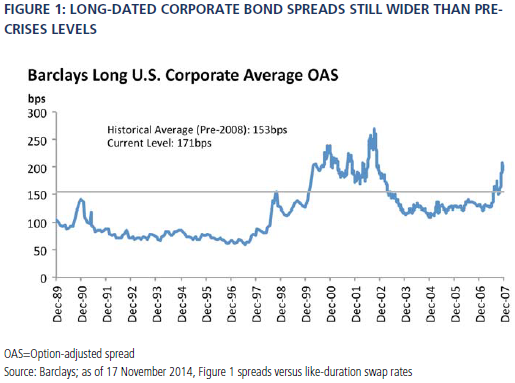

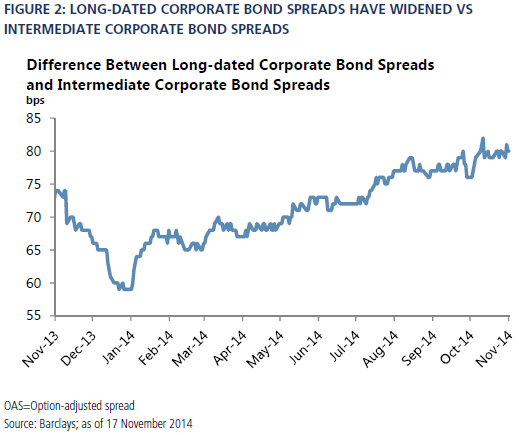

As spreads have tightened over the last several years, many investors are wondering whether we may be entering into rich spread territory. We still see value in spread sectors, especially at the long end of the curve. Long-dated spreads are still meaningfully wide relative to pre-2008 crisis average levels (see Figures 1 and 2). More importantly, the steepness of the spread curve is historically high, providing incremental compensation for investors willing to extend duration in the credit space.

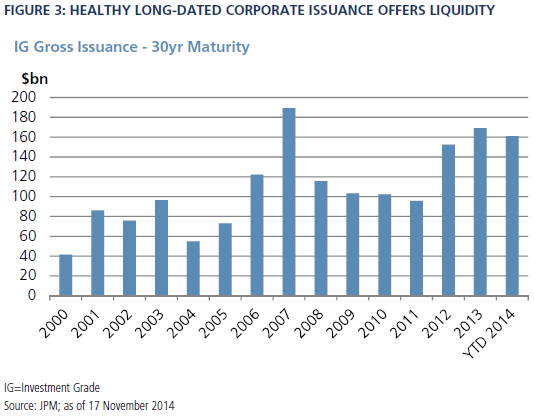

Despite long credit yields falling this year on the back of lower Treasury rates, long duration spread underperformance (relative to intermediate spreads and long Treasuries) offers an attractive entry point for plan sponsors who want to improve the match with their liabilities and avoid further declines in funding ratios that could occur as a result of long credit spreads tightening or a flattening of the spread curve. Healthy increases in issuance of long investment-grade corporate bonds over the last few years have created good liquidity conditions for sponsors seeking to increase those allocations (see Figure 3).

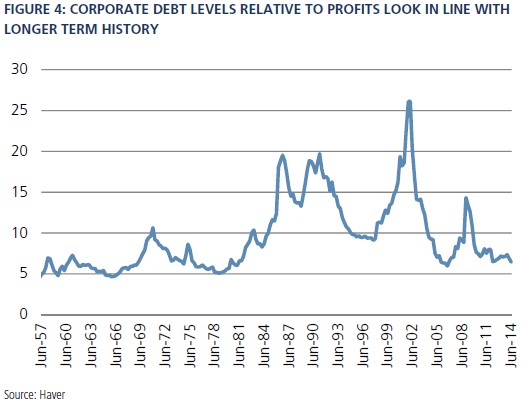

Because defined benefit plans typically have long (or very long) investment horizons, allocation decisions cannot be driven solely by valuations at a specific point in time or technical factors. Those decisions must incorporate fundamental factors. One of the most important fundamental factors when it comes to investing in credit – especially at the long end of the curve – revolves around a corporation’s debt burden. While some will point to moderate increases in aggregate leverage over the last couple of years as a reason for caution, it is important to acknowledge that corporate debt levels are actually in line with long term averages when measured relative to corporate profits (see Figure 4).

In addition, the outlook for the U.S. economy should support long credit spreads in the near to medium term. Indeed, economic growth remains robust, consumer confidence is strong and lower gas prices should be further supportive of consumption heading into the holiday season. This leads us to forecast 2.5% to 3% GDP growth for the U.S. over the next 12 months.

Technicals

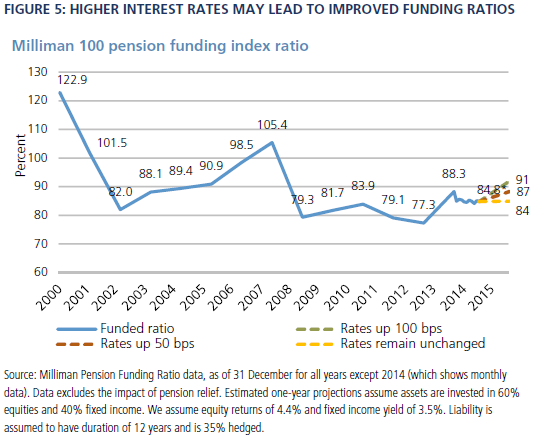

Technical factors should not be the main driver behind investment decisions for long-term investors like pension plan sponsors. However, given the persistent low interest rate environment and potential for lower returns across most asset classes and sectors going forward, technicals are now playing a more important role than they used to. We believe that technical factors are going to turn as we head into the new year. Our forecast is for the Federal Reserve to begin raising interest rates in the June to September timeframe (possibly earlier if data continues to confirm improvements in labor markets and the broad economy). Higher interest rates would lead to improving funding ratios for corporate defined benefit plans (see Figure 5). As a result demand for long credit bonds would pick up as pension plans move down their glide paths and de-risk thereby compressing longer dated corporate spreads even as Treasury yields rise.

Putting it all together

With fundamentals, technicals and valuations all pointing to adding long credit, plan sponsors need to consider portfolio construction. Purchasing long credit bonds presents several challenges. First, the holding period is much longer than that for intermediate or shorter maturity bonds. Second, transaction costs as a percentage of annual carry are meaningfully higher. Finally, liquidity decreases over time as on-the-run 30-year corporate bonds become off-the-run bonds as corporations issue new 30-year bonds.

Given these unique challenges, passive investing in long credit creates significantly higher risks. A structured approach that combines rigorous top-down macroeconomic-analysis to take views on duration and credit sectors with equally thorough bottom-up credit research to identify companies where fundamentals are improving may deliver alpha that can help clients reduce their funding mismatch over time.

PIMCO has a long history as a long duration portfolio manager and the global tools necessary for such sophisticated investing. Our rigorous macro process, starting with quarterly secular and cyclical forums and regional portfolio committees – all of which utilize the breadth and depth of our 250-strong global portfolio management team– makes PIMCO uniquely positioned to take advantage of the diverging global macro landscape. More importantly, our 60-plus credit analysts covering companies globally helps us identify investment opportunities for the long haul. Some of the themes that resonate across our long credit investments include companies and sectors with potential for strong secular/cyclical earnings growth, aggressive pricing power, high barriers to entry and, most importantly, expectations for de-leveraging on a forward-looking basis. Some of the sectors that look attractive based on these criteria include banks and financials, healthcare, building materials, mid-stream energy, pipelines, airlines and cable.

Given recent underperformance of long credit relative to intermediate credit, PIMCO is not only looking to increase long credit exposure in its LDI mandates that it manages for its clients but also to take advantage of the recent credit curve steepening by selectively extending maturities in the credits we like.

Long credit spread and long duration decisions can be bifurcated. You can consider spreads now, without committing to duration.

Investing in the bond market is subject to risks, including market, interest rate, issuer, credit, inflation risk, and liquidity risk. The value of most bonds and bond strategies are impacted by changes in interest rates. Bonds and bond strategies with longer durations tend to be more sensitive and volatile than those with shorter durations; bond prices generally fall as interest rates rise, and the current low interest rate environment increases this risk. Current reductions in bond counterparty capacity may contribute to decreased market liquidity and increased price volatility. Bond investments may be worth more or less than the original cost when redeemed. High yield, lower-rated securities involve greater risk than higher-rated securities; portfolios that invest in them may be subject to greater levels of credit and liquidity risk than portfolios that do not. Derivatives may involve certain costs and risks, such as liquidity, interest rate, market, credit, management and the risk that a position could not be closed when most advantageous. Investing in derivatives could lose more than the amount invested. Diversification does not ensure against loss.

Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be interpreted as investment advice, as an offer or solicitation, nor as the purchase or sale of any financial instrument. Forecasts and estimates have certain inherent limitations, and unlike an actual performance record, do not reflect actual trading, liquidity constraints, fees, and/or other costs. In addition, references to future results should not be construed as an estimate or promise of results that a client portfolio may achieve.

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are suitable for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

This material contains the opinions of the manager and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO and YOUR GLOBAL INVESTMENT AUTHORITY are trademarks or registered trademarks of Allianz Asset Management of America L.P. and Pacific Investment Management Company LLC, respectively, in the United States and throughout the world.

©2014, PIMCO.

© PIMCO