A solid grasp of exchange rates and how they impact various asset classes can help international investors make better-informed decisions.

The asset class most likely to be impacted negatively by a strengthening dollar is non-dollar fixed-rate bonds.

Weakness in foreign currencies and corresponding strength in the US dollar has caused the dollar to rally toward multiyear highs relative to a basket of other currencies. Still, the dollar remains at low levels compared with previous decades. In this context we thought it would be useful to review exchange rate conventions and the impact of exchange rate changes on various asset classes. Next, we take a look at the factors that have helped the dollar to strengthen and how they might evolve in the coming years.

The Unconventional Conventions of Exchange Rate Quotes

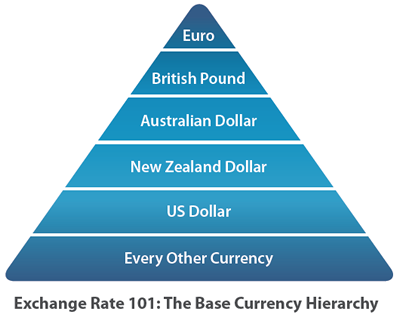

The conventions of quoting exchange rates can be confusing and counterintuitive. First, there is the legacy of base currency hierarchy. That hierarchy goes as follows: euro > British pound > Australian dollar > New Zealand dollar > US dollar > every other currency. Thus, the convention for quoting the euro and US dollar exchange rate is always "EUR/USD." A British pound to Australian dollar cross rate would be "GBP/AUD." And a US dollar to Japanese yen cross rate is "USD/JPY." Sometimes the notation is slightly different: EUR-USD or USD-JPY for example. Also, for the "every other currency" part of the above hierarchy, there is no standard convention for which part of the cross rate comes first or second.

Next, there is the strange convention for what exchange rates like EUR/USD or GBP/AUD mean exactly. When we think of rates in the scientific sense, such as meters per second (m/s) for speed or pounds per square inch (psi) for pressure, we state them in terms of quantity of the numerator per one unit of the denominator: number of meters traveled per each second, number of pounds per each square inch, etc. Not so with exchange rates. For reasons we cannot divine, the progenitors of exchange rate convention decided to do the opposite. An exchange rate like EUR/USD means one euro per number of US dollars. EUR/USD quoted at 1.30 thus means ‘for each euro, 1.30 US dollars’ and the base currency (the one we fix) is always in the numerator, not the denominator.

How Foreign Exchange Movements Can Impact Your Investment

Investors’ home country currencies constitute their present and future purchasing power. For US investors, a strengthening dollar is the converse of weakening foreign currencies, and it means that investors’ assets outside the US could be negatively impacted by the dollar’s strength. All else equal, those assets would buy fewer US dollar goods.

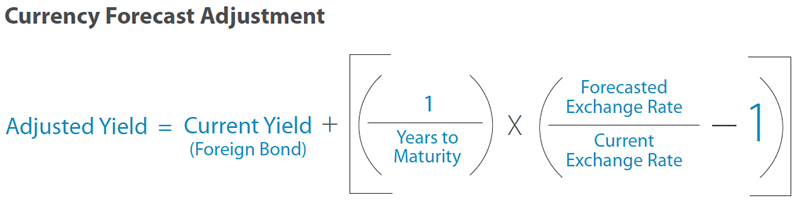

But all else is not equal when investing outside the US. Non-US equities, in particular, may be impacted in myriad ways by fluctuating exchange rates and their impact on company costs, revenues, assets, and liabilities. However, the asset class most likely to be impacted negatively by a strengthening dollar is non-dollar fixed-rate bonds. The purchase of a non-dollar fixed-rate bond locks in a yield to maturity. Assuming the bond is held to maturity, its return would be roughly its yield plus or minus the change in the exchange rate between the time the bond was purchased and its maturity. In the context of a weakening foreign currency, the currency impact subtracts from the yield in US dollar terms. The calculation for deciding whether and how much to invest in non-dollar bonds going forward is to take the starting yield, make an adjustment for the currency forecast over the investment horizon, and then determine whether the expected yield in dollar terms is sufficient to compensate for whatever additional risks are involved compared to US government bonds and their yields.

With stocks, exposure to a strengthening dollar can be positive or negative depending on the circumstances. For example, an export-oriented company based in Europe may make significant sales to US dollar-based customers while euro-denominated manufacturing labor constitutes a large portion of its costs. Such a company could benefit from a stronger dollar as its costs would decrease faster than its revenues (when translated to US dollars), and the company’s profit margins and earnings could increase enough to offset the decline in the exchange rate. This is a positive result from weakness in a company’s operating and reporting currency.

On the other hand, a retailer that sells products manufactured from raw materials using foreign labor could be negatively impacted by weakness in its domestic currency. In this scenario, the company’s costs rise relative to what it can charge in its domestic market, and competitors that offer domestically sourced products gain a pricing advantage.

Exchange Rate Forecasting: Mind Your Ps

Over long periods of time we believe exchange rates are ultimately tethered to purchasing power parity (PPP). Purchasing power parity is a theory that explains how exchange rates adjust over time to equalize the value of identical goods priced in different currencies. Over shorter periods, a variety of factors can influence currency exchange rates, sometimes pulling the exchange rate between two countries far away from what might be considered a fair value based on their citizens’ purchasing power. Such factors include differences in the countries’ interest rates, trade flows, current account balances, savings rates, government budget deficits, raw materials prices, import/export intensity, and political actions, among others.

Attempting to navigate the intersection of these various factors may be a fool’s errand: there are a relatively small number of actively traded currencies in comparison with thousands of individual stocks, and the foreign exchange markets are incredibly deep and liquid. The competition to gain in the short run from a bit of news regarding any factor expected to influence an exchange rate is extremely intense and rapid. But, with a long enough time horizon, a bit of forethought, and significant enough deviation of exchange rate from the path of relative purchasing power, investors have a chance to benefit from the forces of purchasing power parity, or at least avoid getting hurt by them.

Will the dollar’s strength last?

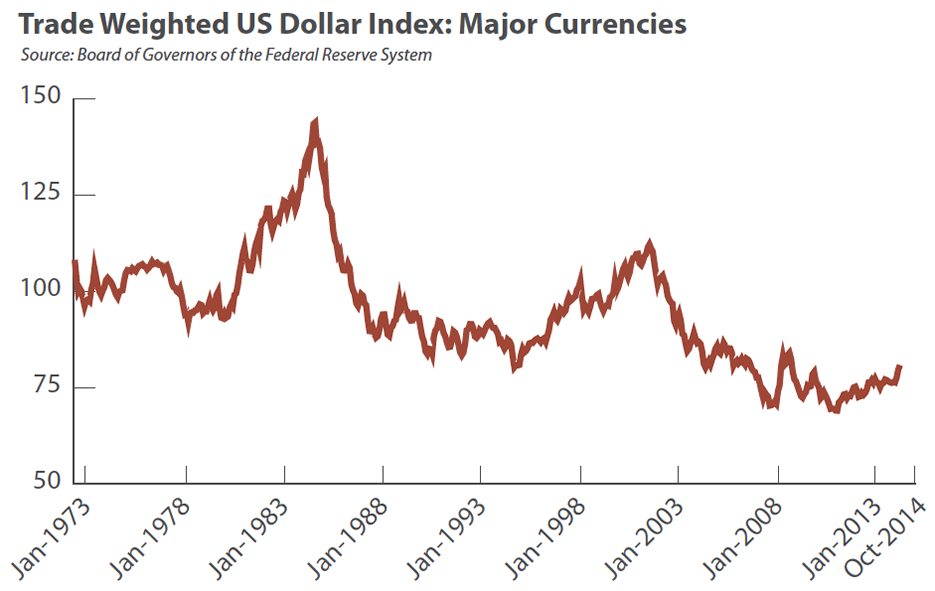

The US dollar’s relative strength today is a fairly recent phenomenon. The dollar has been a generally weak currency against many developed and emerging markets currencies for much of the past decade. Once the "strong dollar policy" of Robert Rubin, Secretary of the Treasury under Clinton, was in the rearview mirror, it was apparent that the policy had worked too well — to the point that the dollar had strengthened substantially beyond the level implied by its purchasing power against many other currencies. The political will to continue supporting the dollar’s strength (by running large government surpluses, for example) began to evaporate. As a result, the dollar weakened by more than 37% against a trade-weighted basket of other major currencies between 2001 and 2011.

The dollar weakness between 2001 and 2011 is likely to have "overcorrected" the excess strength it had built in the prior years, especially relative to commodity-oriented currencies. The currencies of Canada, Australia, and commodity-oriented emerging markets such as Brazil (iron ore, agriculture) and Chile (copper) benefited from US dollar weakness, commodity strength, and strong demand from China, whose appetite for raw materials greatly increased throughout the 2000s. Strong economic growth in these economies had allowed their central banks to keep interest rates higher than in the US, so investors attempted to profit from the extra "carry" they could earn by investing in foreign currency bonds, knowing that the currencies were likely to be supported by continued trade flows.

Today, the phenomenal growth in the volume of China’s raw materials imports has slowed as its leaders attempt to shift focus from commodity-intensive investment projects to an increase in domestic consumption. Elsewhere, such as Europe and Japan, growth has stalled, and central banks have brought interest rates to zero with promises of further stimulus. Commodities and energy prices have fallen with the slowdown in China’s demand, impacting the trade flows of commodities exporters.

All of this leaves the US as a bright spot: the one major economy closest to operating at a "normal" level after several years of lackluster growth. The Federal Reserve is likely to begin raising interest rates next year, but inflation expectations remain subdued. The US dollar is close to fairly valued against major currencies such as the euro, pound, and yen, and is still undervalued against the Canadian and Australian dollars and several emerging markets currencies — all on the basis of purchasing power parity. This should mean that an improving interest rate spread with other currencies is less likely to be undermined by purchasing power’s stubborn tow in the wrong direction.

As a result of these influences, we remain optimistic about the dollar’s continued strength and favor domestic over foreign denominated bonds of otherwise equivalent risk. We also favor foreign companies with strong and improving export positions. We are wary of companies positioned to suffer as a consequence of weakening exchange rates in their home countries.

Copyright 2014 Saturna Capital Corporation and/or its affiliates. All rights reserved. Vol. 8 · No. 9

Saturna Capital does not share subscriber information with third parties.

Important Disclaimers and Disclosures

This report is intended only for the information of the reader and is not to be used for or considered as an offer or the solicitation of an offer to sell or buy any securities or other financial instruments of any kind, including without limitation, any mutual fund or other product offered, sponsored, created, or managed by Saturna Capital Corporation or its subsidiaries or affiliates ("Saturna"). This report is not intended for distribution to, or use by, any person or entity who is a citizen or resident of, or located in, any locality, state, country, or other jurisdiction in which such distribution, publication, availability, or use would be contrary to law or regulation or which would subject Saturna to any registration or licensing requirement within such jurisdiction.

This document should not be considered as providing investment advice or services, or any other service offered by Saturna. Saturna may not have taken any steps to ensure that the securities referred to in this report are suitable for any particular investor. Saturna will not treat recipients as its customers by virtue of their reading or receiving the report.

Nothing in this report constitutes investment, legal, accounting, or tax advice or a representation that any investment or strategy is suitable or appropriate to a particular investor's circumstances or otherwise constitutes a personal recommendation to any investor. Saturna does not offer advice on the tax consequences of any investment.

All material presented in this report, unless specifically indicated otherwise, is under copyright to Saturna. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied, or distributed to any other party without the prior express written permission of Saturna. Unless otherwise indicated, all trademarks, service marks, and logos used in this report are trademarks or service marks of Saturna.

The information in this report was obtained from sources Saturna believes to be reliable, and Saturna believes the information and opinions in the material are accurate and complete as of the date of this material. However, information and opinions contained herein will change over time and without notice. Saturna has no obligation to update or amend any information or opinions at any time. Saturna makes no representations as to the accuracy or completeness of this material, nor does it have any responsibility to ensure that any other materials, including any containing materially different information, are brought to the attention of any recipient of this report.

Under no circumstances shall Saturna, its employees, or any affiliate be responsible for any investment decision by any recipient. This material is distributed on condition that it will not form the sole basis or a sufficient basis for any investment decision by any recipient. Any recipient who is not a market professional or institutional investor should seek the advice of an independent financial adviser prior to making any investment based on this report or for any necessary explanation of its contents.

Saturna does not provide tax, legal, or accounting advice. Investors should consult their own tax, legal, and accounting advisers before engaging in any transaction. In compliance with IRS requirements, recipients are notified that any discussion of US federal tax issues contained or referred to herein is not intended or written to be used for the purpose of (A) avoiding penalties that may be imposed under the Internal Revenue Code; nor (B) promoting, marketing, or recommending to another party any transaction or matter discussed herein.

The Dow Jones Industrial Average is a price-weighted index of 30 of the largest, most widely held US stocks. The S&P 500 is an index comprised of 500 widely held common stocks considered to be representative of the US stock market in general. The Russell 1000 Growth index is a widely recognized index of large-cap growth stocks. The Russell 2000 Index is comprised of US small cap stocks and measures the performance of the 2,000 smallest US companies in the Russell 3000 Index. The NASDAQ Composite index measures the performance of more than 5,000 US and non-US companies traded "over the counter" through the National Association of Securities Dealers Automated Quotation system. The MSCI EAFE Index, produced by Morgan Stanley Capital International, measures the equity market performance of developed markets in Europe, Australasia, and the Far East. The MSCI Emerging Markets Index, produced by Morgan Stanley Capital International, measures equity market performance in over 20 emerging market countries. Barclay's Capital US Aggregate Bond Index measures the performance of the US bond market. The BofA Merrill Lynch (BAML) US High Yield Index tracks the performance of US-dollar-denominated below-investment-grade corporate debt publicly issued in the US domestic market. The BofA Merrill Lynch (BAML) US High Yield Index tracks the performance of US-dollar-denominated below-investment-grade corporate debt publicly issued in the US domestic market.

All indices shown are widely recognized unmanaged indices of common stock and bond prices that reflect no deductions for fees, expenses, or taxes. Investors cannot invest directly in the indices.

Past performance does not imply or guarantee future performance, and no representation or warranty, express or implied, is made regarding future performance. The price for, value of, and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of foreign securities and financial instruments is subject to exchange rate fluctuations that may have a positive or negative effect on the price or income of such securities or financial instruments. Investors in securities such as American Depositary Receipts — the values of which are influenced by currency volatility — effectively assume this risk.