2015 Year Ahead: Continuing to Deflate the Global Credit Bubble

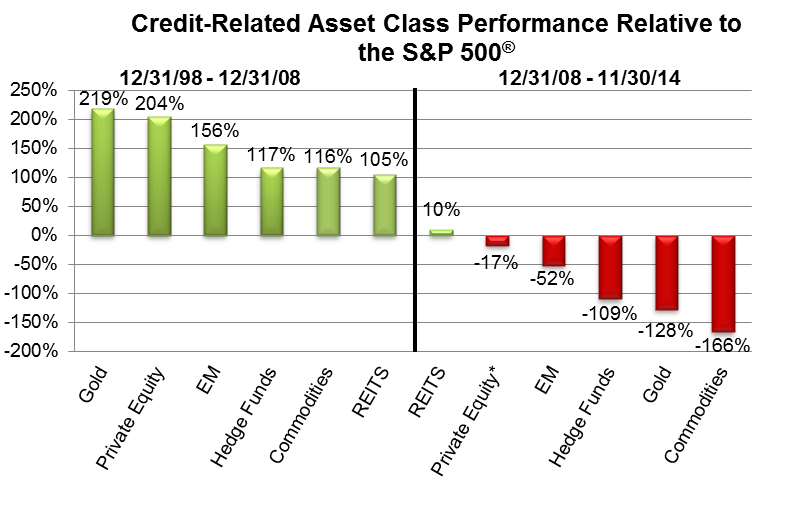

Stock market leadership virtually always changes when volatility significantly spikes, and the 2008 bear market was no exception. Credit-related asset classes led the markets for the decade prior to 2008 as the global credit bubble inflated.

Since 2008’s bear market, however, leadership has significantly changed and credit-related asset classes have generally underperformed plain, old-fashioned stocks.

Chart 1 below shows the relative performance of credit-related asset classes versus the S&P 500® from 1998 to 2008 and from 2008 to present. The deflation of the global credit bubble has clearly hurt the performance of credit-related asset classes.

The deflation of the global credit bubble remains the prime driver of our positioning for 2015. We continue to underweight or fully avoid credit-related asset classes.

Chart 1:

*Private Equity Performance available through 6/30/14

Source: Richard Bernstein Advisors LLC, MSCI, Standard & Poors, BofA Merrill Lynch, Bloomberg, Cambridge Associates. For Index descriptors, see "Index Descriptions" at end of document

1. ECB causes Europe to flounder

The European Central Bank (ECB) seems to be trying very hard to be among the worst central banks in history. The ECB actually tightened monetary policy over the past couple of years despite mounting evidence of budding deflation. One does not need a Ph.D. in Economics to know that tightening monetary policy in the face of deflation and contracting private sector credit growth is not a sound monetary policy. The ECB’s continuous missteps have resulted in significantly subpar growth.

The ECB is now claiming they will significantly expand their balance sheet, and such actions might be bullish for European equities. However, recent data suggests they have so far only stopped tightening, and have yet to start easing. If they alter that policy, then European stocks might again be attractive, however, the ECB’s sclerotic policy reaction to building deflation warrants an underweight of European equities. Our portfolios remain underweight Europe, with exposure limited to large cap and defensive stocks.

2. Japan grows market share

Early in my career at EF Hutton in 1986, our auto analyst stated in our morning meeting that Toyota felt they could gain market share from GM at 120 ¥/$. ¥/$ was 160 at the time, and the entire meeting broke up in laughter. No one could believe that the dollar would depreciate 25% versus the Yen and, if it ever did, Toyota would never gain market share. The Yen eventually traded to 80¥/$, and Toyota nearly put GM out of business.

The point to the story is that Japan at the time had a significant competitive advantage versus the United States. The fact that the Yen might appreciate was a minor hindrance to Japanese companies gaining market share versus US companies. Today, however, Japan’s competitive advantage has been whittled away by the combination of Japanese demographics, Japan’s lack of domestic investment in productive resources, and the improvement in productivity in other parts of the world (including the US).

In the absence of a competitive advantage, companies or countries are forced to compete on price in order to gain market share, and we believe depreciating the Yen is the only route for the Japanese economy to re-emerge within the time frame of most investors. We began this theme when ¥/$ was roughly 85, and we think the Yen may weaken significantly even from today’s depressed levels (roughly 120).

We remain overweight Japan with an emphasis on large cap exporters of finished goods.

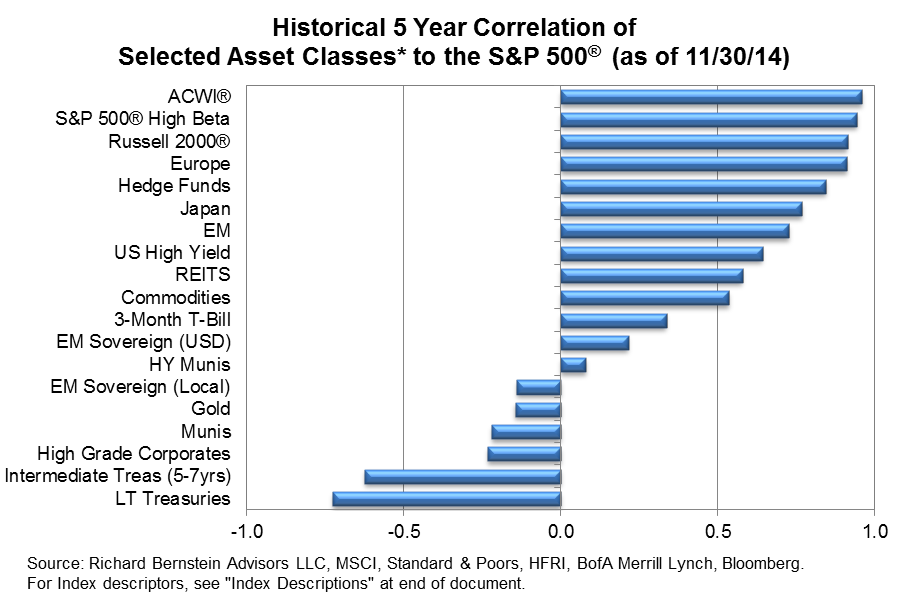

3. Treasuries for diversification…yes, still.

We have become somewhat notorious for our liking of treasuries as a portfolio diversifier. Although not as extreme as it was several years ago, Chart 2 shows the correlation of various asset classes to the S&P 500® and there are relatively few asset classes that have negative correlation to stocks. By including treasuries, we can take stronger risk positions within our multi-asset portfolios, but not increase overall portfolio volatility.

Chart 2:

Source: Richard Bernstein Advisors LLC, MSCI, Standard & Poors, HFRI, BofA Merrill Lynch, Bloomberg.

For Index descriptors, see "Index Descriptions" at end of document.

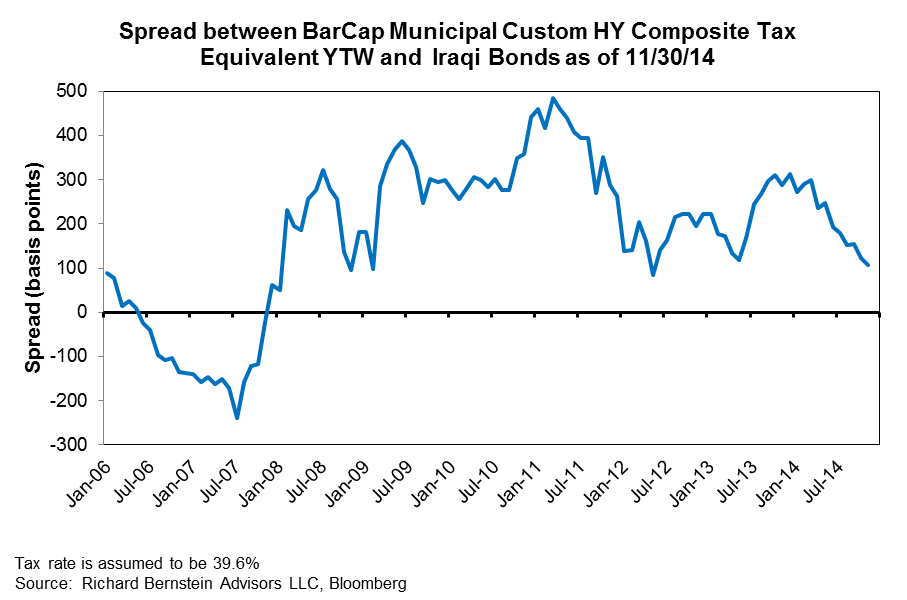

4. High Yield Munis remain attractive

High yield municipal bonds are a sizeable portion of most of our multi-asset portfolios because we view them as the most attractive sector of the global fixed-income markets. It seems ironic to us that investors are taking all sorts of risks in sectors like emerging market debt, but refuse to look at US high yield munis.

Chart 3 shows the spread between high yield munis and Iraq government bonds. The spread implies that US high yield municipal bonds are riskier than Iraqi bonds. Isn’t there a brutal civil war taking place in Iraq? One might question fiscal responsibility in Illinois or Michigan, but they’re certainly not Iraq!

Chart 3:

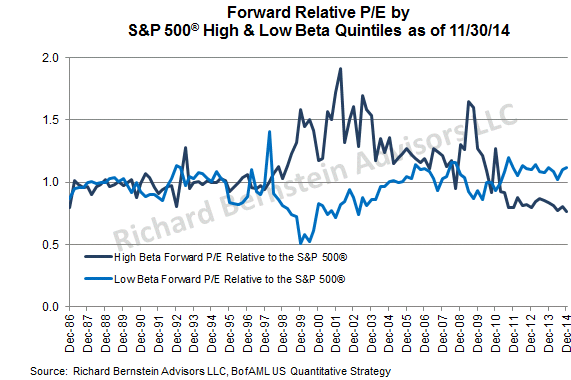

5. Cheap High Beta

Whereas high-beta social media stocks and other “disruptor” stocks (as CNBC calls them) are extraordinarily expensive, other more traditional high-beta stocks appear historically undervalued. Chart 4 shows the relative PE of low beta and high beta stocks within the S&P 500®. This chart clearly suggests that investors remain very scared of traditional high beta stocks, but we have significant exposure to this traditional high-beta group which is historically undervalued.

Chart 4:

Our overall positioning of avoiding credit-related asset classes remains largely out-of-favor, and remains the cornerstone of our portfolios. We will watch these themes closely and reposition accordingly should a more favorable cyclical backdrop potentially outweigh this secular trend.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

World: MSCI All Country World Index (ACWI®). The MSCI ACWI® is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of global developed and emerging markets.

S&P 500®: Standard & Poor’s (S&P) 500® Index. The S&P 500® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

S&P 500® High Beta: Standard & Poor’s (S&P) 500® High Beta Index : The S&P 500® High Beta Index is designed to measure the performance of the 100 constituents in the S&P 500® that are most sensitive to changes in market returns. For this index, the market is represented by the performance of the S&P 500®.

Europe: MSCI Europe Index. The MSCI Europe Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of the developed markets in Europe. The MSCI Europe Index consists of the following 16 developed market country indices: Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland, Italy, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, and the United Kingdom

Japan: MSCI Japan Index: The MSCI Japan Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of Japan.

EM Equity: MSCI Emerging Markets (EM) Index. The MSCI EM Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of emerging markets.

U.S. Small Caps: Russell 2000 Index. The Russell 2000 Index is an unmanaged, capitalization-weighted index designed to measure the performance of the small-cap segment of the US equity universe. The Russell 2000 Index is a subset of the Russell 3000® Index.

Gold: Gold Spot USD/oz Bloomberg GOLDS Commodity. The Gold Spot price is quoted as US Dollars per Troy Ounce.

US Dollar: : InterContinentalExchange (ICE) US Dollar Index (DXY). The ICE US Dollar Index, indicating the general international value of the USD, averages the exchange rates between the USD and six major world currencies, using rates supplied by some 500 banks.

Commodities: S&P GSCI® Index. The S&P GSCI® seeks to provide investors with a reliable and publicly available benchmark for investment performance in the commodity markets, and is designed to be a “tradable” index. The index is calculated primarily on a world production-weighted basis and is comprised of the principal physical commodities that are the subject of active, liquid futures markets.

REITS: THE FTSE NAREIT Composite Index. The FTSE NAREIT Composite Index is a free-float-adjusted, market-capitalization-weighted index that includes all tax qualified REITs listed in the NYSE, AMEX, and NASDAQ National Market.

Hedge Fund Index: HFRI Fund Weighted Composite Index. The HFRI Fund Weighted Composite Index is a global, equal-weighted index of over 2,000 single-manager funds that report to the HFR (Hedge Fund Research) database. Constituent funds report monthly net-of-all-fees performance in USD and have a minimum of $50 million under management or a twelve (12)-month track record of active performance. The Index includes both domestic (US) and offshore funds, and does not include any funds of funds.

3-Mo T-Bills: BofA Merrill Lynch 3-Month US Treasury Bill Index. The BofA Merrill Lynch 3-Month US Treasury Bill Index is comprised of a single issue purchased at the beginning of the month and held for a full month. The Index is rebalanced monthly and the issue selected is the outstanding Treasury Bill that matures closest to, but not beyond, three months from the rebalancing date.

Intermediate Treasuries (5-7 Yrs): The BofA Merrill Lynch 5-7 Year US Treasury Index

The BofA Merrill Lynch 5-7 Year US Treasury Index is a subset of The BofA Merrill Lynch US Treasury Index (an unmanaged Index which tracks the performance of US dollar denominated sovereign debt publicly issued by the US government in its domestic market). Qualifying securities must have at least one year remaining term to final maturity, a fixed coupon schedule and a minimum amount outstanding of $1 billion. including all securities with a remaining term to final maturity greater than or equal to 5 years and less than 7 years.

Long-term Treasury Index: BofA Merrill Lynch 15+ Year US Treasury Index. The BofA Merrill Lynch 15+ Year US Treasury Index is an unmanaged index comprised of US Treasury securities, other than inflation-protected securities and STRIPS, with at least $1 billion in outstanding face value and a remaining term to final maturity of at least 15 years.

Municipals: BofA Merrill Lynch US Municipal Securities Index. The BofA Merrill Lynch US Municipal Securities Index tracks the performance of USD-denominated, investment-grade rated, tax-exempt debt publicly issued by US states and territories (and their political subdivisions) in the US domestic market. Qualifying securities must have at least one year remaining term to final maturity, a fixed coupon schedule, and an investment-grade rating (based on an average of Moody’s, S&P and Fitch). Minimum size requirements vary based on the initial term to final maturity at the time of issuance.

High Yield Municipals: Barclays Municipal Custom High Yield Municipals Composite. The Barclays Municipal Custom High Yield Municipals Composite is calculated using a market value weighting methodology and it tracks the high-yield municipal bond market with a 75% weight in non-investment grade municipal bonds and a 25% weight in Baa/BBB-rated investment grade municipal bonds for liquidity and balance.

High Grade Corporates: BofA Merrill Lynch 15+ Year AAA-AA US Corporate Index. The BofA Merrill Lynch 15+ Year AAA-AA US Corporate Index is a subset of the BofA Merrill Lynch US Corporate Index (an unmanaged index comprised of USD-denominated, investment-grade, fixed-rate corporate debt securities publicly issued in the US domestic market with at least one year remaining term to final maturity and at least $250 million outstanding) including all securities with a remaining term to final maturity of at least15 years and rated AAA through AA3, inclusive.

Private Equity: The Cambridge Associates LLC U.S. Private Equity Index®. The Cambridge Associates LLC U.S. Private Equity Index® is an end-to-end calculation based on data compiled from 986 U.S. private equity funds (buyout, growth equity, private equity energy and mezzanine funds), including fully liquidated partnerships, formed between 1986 and 2012. Pooled end-to-end return, net of fees, expenses, and carried interest.Historic quarterly returns are updated in each year-end report to adjust for changes in the index sample.

EM Sovereign (USD): The BofA Merrill Lynch US Dollar Emerging Markets Sovereign Plus Index. The BofA Merrill Lynch US Dollar Emerging Markets Sovereign Plus Index tracks the performance of US dollar denominated emerging market and cross-over sovereign debt publicly issued in the Eurobond or US domestic market. Qualifying countries must have a BBB1 or lower foreign currency long-term sovereign debt rating (based on an average of Moody’s, S&P and Fitch). Countries that are not rated, or that are rated “D” or “SD” by one or several rating agencies qualify for inclusion in the index but individual non-performing securities are removed. Qualifying securities must have at least one year remaining term to final maturity, a fixed or floating coupon and a minimum amount outstanding of $250 million. Local currency debt is excluded from the Index.

EM Sovereign (Local): The BofA Merrill Lynch Local Debt Markets Plus Index: The BofA Merrill Lynch Local Debt Markets Plus Index is designed to track the performance of sovereign debt publicly issued and denominated in the issuer's own domestic market and currency other than the more established top-tier sovereign markets. In order to be included in the Index, a country (i) must have at least $10 billion (USD equivalent) outstanding face value of Index qualifying debt (i.e., after imposing constituent level filters on amount outstanding, remaining term to maturity, etc.); and (ii) must have at least one readily available, transparent price source for its securities. In addition, the following countries are specifically excluded from the index: G10 countries, Euro members; all countries with a foreign currency long-term sovereign debt rating of AA3 or higher (based on an average of Moody’s,S&P and Fitch).

Iraqi Bonds: Republic of Iraq Sovereign, Unsecured, Maturity 01/15/2028, id number EF2306852

© Copyright 2014 Richard Bernstein Advisors LLC. All rights reserved.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment's value. Past performance is, of course, no guarantee of future results. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.

About Richard Bernstein Advisors:

Richard Bernstein Advisors LLC is an independent investment adviser. RBA partners with several firms including Eaton Vance Corporation and First Trust Portfolios LP, and currently has $3.4 billion collectively under management and advisement as of November 30, 2014. RBA acts as sub‐advisor for the Eaton Vance Richard Bernstein Equity Strategy Fund, the Eaton Vance Richard Bernstein All‐Asset Strategy Fund and the Eaton Vance Richard Bernstein Market Opportunities Strategy Fund and also offers income and unique theme‐oriented unit trusts through First Trust. RBA is also the index provider for the First Trust RBA American Industrial RenaissanceTM ETF and the First Trust RBA Quality Income ETF. Additionally, RBA runs ETF asset allocation SMA portfolios at UBS and Merrill Lynch and on select RIA platforms. RBA's investment insights as well as further information about the firm and products can be found at www.RBAdvisors.com.