In the second half of 2014, the inflation protection provided by Treasury Inflation-Protected Securities (TIPS) has proven to be somewhat of a curse, as falling oil prices have dragged down inflation expectations, and with it, the value of TIPS. This inflation protection can be a blessing, as interest payments and market value will keep pace with inflation, the long-term enemy of bond investors, but this can be a drag when inflation rates decelerate, as has been the case in 2014.

TIPS & Oil

TIPS have underperformed similar-dated Treasuries thus far in 2014, due to lower oil prices. The interest rate sensitivity of TIPS has been a positive for performance, as it has for all high-quality bonds, as interest rates declined over the course of the year, but the inflation component of TIPS has detracted from performance. Energy, and specifically gasoline prices, can be a significant driver of overall inflation as measured by the Consumer Price Index (CPI). Therefore, large swings in oil prices can influence the CPI [Figure 1], which, in turn, determines the inflation compensation paid to TIPS holders. Oil prices can therefore have a significant impact on TIPS prices. Underperformance of TIPS relative to Treasuries can be traced to mid-2014 as oil prices peaked [Figure 2].

TIPS & Inflation Expectations

TIPS underperformance has led to the lowest market-implied inflation expectations of the past four years [Figure 3]. The 10-year break-even inflation rate implied by TIPS has fallen to 1.7%, down from a high of 2.3% in 2014 and below the long-term average of 2.1%. The break-even inflation rate is the rate of inflation at which an investor will break even relative to a conventional Treasury with a comparable maturity. A lower break-even inflation rate implies TIPS are cheaper relative to conventional Treasuries and vice versa.

Budding Opportunity

The fall in oil may be creating opportunities for TIPS investors. The U.S. economy expanded at healthy 4.6% and 3.9% rates over the second and third quarters of 2014 and is on pace to expand at a 2.5 - 3.0% pace during the current quarter. Data continue to reflect an improving U.S. economy, and the labor market, although slow to recover, is gradually reducing excess slack. Inflation expectations may be unrealistically low, and the low implied inflation expectations provide a low hurdle rate for investors.

On the other hand, slower overseas economic growth and weaker oil demand may keep inflation low or may lead to even lower realized inflation rates. Winter is a seasonally weak period for oil demand, which is a contributing factor to current oil price declines.

TIPS performance may then follow one of two paths:

- If inflation or inflation expectations increase, TIPS may outperform Treasuries, as current inflation expectations are low and the inflation accrual could bolster returns.

- In a deflationary environment, TIPS prices would benefit, as bond prices rise in response to deflation risks, but likely not as much as conventional Treasuries.

Fed Catalyst

This week’s Federal Reserve (Fed) meeting may provide a catalyst for TIPS. A key focal point will be whether the Fed maintains use of the “considerable time” language in its discussion of how long rates will remain at historically low levels. Dropping “considerable time” could be viewed as a sign of confidence in the economy and that deflation risks may be overblown. High-quality bonds could weaken in response, but such a sell-off would likely be accompanied by rising inflation expectations among TIPS that would at least partially offset price weakness from rising rates. Rising inflation expectations, all else equal, would benefit TIPS relative to Treasuries.

Conversely, if the Fed cites slower overseas economies and lower oil prices as affording them to be patient with regard to rate hikes, TIPS may continue to lag as investor demand for inflation protection remains weak.

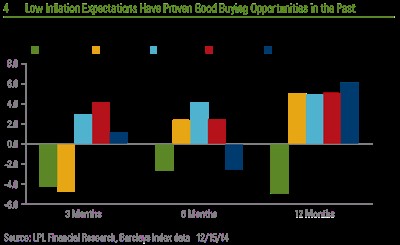

Potential Positive Returns

The last five times break-even inflation rates have declined to 1.7% or lower, the average 12-month return for the Barclays U.S. TIPS Index was 3.3%. Not only did TIPS produce positive returns but they outperformed conventional Treasuries in the process, with the exception of the 2003 episode, according to Barclays Index data [Figure 4]. (In periods where inflation expectations fell below 1.7%, we use the low point in inflation expectations.)

Although this is encouraging for an investor considering TIPS, it is important to know that virtually all of the performance of TIPS during those time periods was driven by interest rate sensitivity and not inflation expectations moving higher. In other words, TIPS benefited from the tailwind of falling interest rates that benefited all high-quality bonds -- a factor that is unlikely to be repeated. Lower interest rates appear unlikely, leaving lower total return prospects than previous experience.

Conclusion

TIPS have become much more attractive as low inflation expectations have provided a low hurdle rate for longer-term investors. However, low absolute yields and lingering uncertainty over oil may limit the prospects of quick improvement. We do, however, find TIPS an attractive high-quality option and certainly more appealing than Treasuries as a result of recent underperformance.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values and yields will decline as interest rates rise, and bonds are subject to availability and change in price.

High-yield/junk bonds are not investment-grade securities, involve substantial risks, and generally should be part of the diversified portfolio of sophisticated investors.

Treasury Inflation-Protected Securities (TIPS) help eliminate inflation risk to your portfolio, as the principal is adjusted semiannually for inflation based on the Consumer Price Index (CPI), while providing a real rate of return guaranteed by the U.S. government. However, a few things you need to be aware of are that the CPI might not accurately match the general inflation rate; therefore, the principal balance on TIPS may not keep pace with the actual rate of inflation. The real interest yields on TIPS may rise, especially if there is a sharp spike in interest rates. If so, the rate of return on TIPS could lag behind other types of inflation-protected securities, like floating rate notes and T-bills. TIPs do not pay the inflation-adjusted balance until maturity, and the accrued principal on TIPS could decline, if there is deflation.