Every new year brings a wave of prognostications. We’re as guilty as anyone regarding stuffing email inboxes with year-ahead reports, but it is always useful to remember that the most important events in any year generally aren’t recognized until they happen. Risk managers will always have an impossible job because risk is, by definition, what isn’t expected. Risks that can be planned for simply aren’t risks.

The energy sector (grease) and the Eurozone (Greece) seem to dominate this year’s supply of year-ahead reports, but there may be related issues that most observers seem to be overlooking. We think they are worth considering.

Greece at risk?

The European Central Bank (ECB) continues to alter Eurozone monetary policy with the speed of an octogenarian using a walker. Despite that deflationary pressures have been building in the Eurozone for several years, the ECB only now appears to be shifting from a mind-boggling tightening policy to a more accommodative one. Deflating balance sheets have put pressure on the EZ banking system, and widespread deflationary forces are once again putting pressure on Europe’s peripheral countries to meet their debt obligations.

There are renewed questions whether Greece might leave the Euro. Certainly, there could be transitional problems as the Greek banking system would have to readjust to a new (undoubtedly weak) Drachma and inflation could deter consumption, but longer-term leaving the Euro might be quite good for Greek economy. A weak Drachma might make Greek goods more competitive, and who wouldn’t enjoy a cheap vacation to the Greek islands?

On the other hand, Greece leaving the Euro might be very bad for the German economy. German productivity has been waning, and a combination of weakening productivity and a stronger Euro could make German exports uncompetitive. Fortunately for Germany, the problems in the EZ peripheral countries kept the Euro weaker than it might have otherwise been. Thus, Germany’s lack of productivity was offset to some extent by the weaker Euro. One might argue that the best thing to happen to Germany has been Greece! Because of Germany’s preference for tight monetary policies, German economic growth might significantly slow if Greece were to leave the Euro. The Euro would likely strengthen as countries other than Germany left the Euro because the Euro would increasingly act like a new Deutsche Mark supported by German tight monetary policies. A strong currency and weakening productivity would likely hurt German growth.

So, an oddity during 2015 could be that Germany actually convinces Greece to remain in the Euro, and Europe benefits from a weaker Euro.

Grease at risk?

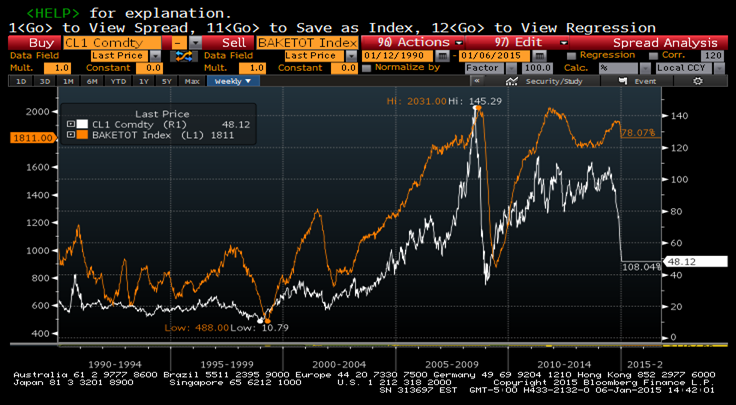

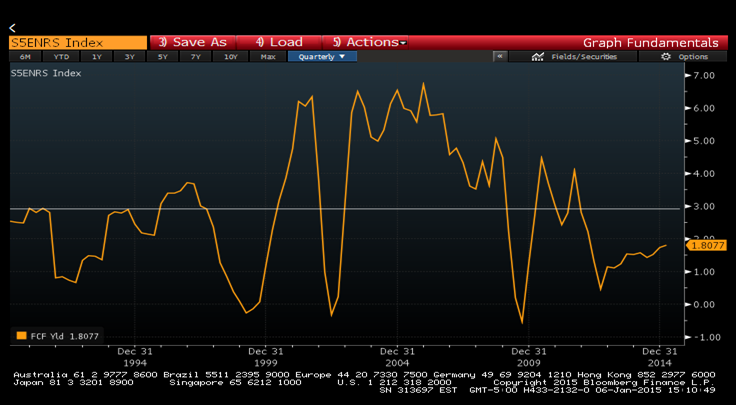

When discussing capital-intensive industries, it’s always important to remember that commodity prices move faster than does the expansion or contraction of capacity. Chart 1 highlights that is now a major issue facing the energy sector. The chart compares the total rig count in the United States to the price of WTI crude oil, and turns in the price of WTI tend to lead turns in the rig count. Most important, the rig count has yet to decrease despite the 50+% fall in the price of WTI. Energy sector earnings and cash flows could be well below analysts’ estimates for quite some time to come. Free cash flow yields for the sector (Chart 2) are below average, so the combination of potentially waning cash flows and overvaluation suggests the energy sector might continue to underperform.

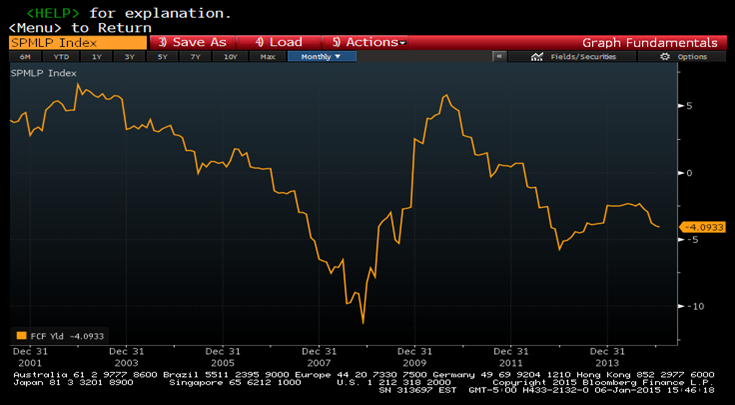

In particular, investors seem to be underestimating the risks of MLPs*. These stocks are very expensive and have negative free cash flow yields (Chart 3). They offered free cash flow yields in excess of +5% years ago when we thought they were attractive. Today, they have free cash flow yields of almost -5%! A 50% drop in oil prices seems certain to have a negative impact on MLPs because of the sector’s overvaluation and increased dependency on external capital for funding.

The fixed-income markets have quickly sensed that energy sector cash flows may come under significant pressure and energy sector spreads have widened considerably. However, it appears to us that equity investors may be too sanguine regarding the sustainability of dividend payments despite that dividends are subordinated relative to debt.

So, another oddity during 2015 could be that the energy sector turns out to be much riskier than investors expect despite the well-known drop in oil prices.

*An MLP is a limited partnership that is publicly traded on a given exchange. MLPs are often recognized for their tax benefits since they are pass-through entities that generally avoid corporate income tax at both state and federal levels since they are classified as partnerships. To qualify for these tax benefits, MLPs must earn at least 90% of their income from “qualified sources” as per the guidelines published by the Internal Revenue Service, such as natural resources. According to the National Association of Publicly Traded Partnerships, qualifying natural resources include: Oil, gas and petroleum products, Coal and other minerals, Timber, Any other resource that is depletable under section 613 of the federal tax code, Industrial source carbon dioxide, Ethanol, biodiesel and other fuels (transportation and storage only).

Grease vs. Greece

2015 could be a year during which Greece is less risky than investors currently believe, but Grease could be even riskier. We remain positioned accordingly.

Chart 1: Rig count versus WTI price

Source: Bloomberg

Chart 2: S&P 500® Energy Sector Free Cash Flow Yield

Source: Bloomberg

Chart 3: S&P MLP Index Free Cash Flow Yield

Source: Bloomberg

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

S&P 500®: Standard & Poor’s (S&P) 500® Index. The S&P 500® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

Sector/Industries: Sector/industry references in this report are in accordance with the Global Industry Classification Standard (GICS®) developed by MSCI Barra and Standard & Poor’s. The GICS structure consists of 10 sectors, 24 industry groups, 68 industries and 154 sub-industries.

MLPs: The S&P MLP Index. The S&P MLP Index provides investors with exposure to the leading partnerships that trade on the NYSE and NASDAQ and includes both Master Limited Partnerships (MLPs) and publicly traded LLC's, which have similar legal structure to MLPs and share the same tax benefits.

*An MLP is a limited partnership that is publicly traded on a given exchange. MLPs are often recognized for their tax benefits since they are pass-through entities that generally avoid corporate income tax at both state and federal levels since they are classified as partnerships. To qualify for these tax benefits, MLPs must earn at least 90% of their income from “qualified sources” as per the guidelines published by the Internal Revenue Service, such as natural resources. According to the National Association of Publicly Traded Partnerships, qualifying natural resources include: Oil, gas and petroleum products, Coal and other minerals, Timber, Any other resource that is depletable under section 613 of the federal tax code, Industrial source carbon dioxide, Ethanol, biodiesel and other fuels (transportation and storage only).

© Copyright 2015 Richard Bernstein Advisors LLC. All rights reserved.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment's value. Past performance is, of course, no guarantee of future results. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.

About Richard Bernstein Advisors:

Richard Bernstein Advisors LLC is an independent investment adviser. RBA partners with several firms including Eaton Vance Corporation and First Trust Portfolios LP, and currently has $3.4 billion collectively under management and advisement as of November 30, 2014. RBA acts as sub‐advisor for the Eaton Vance Richard Bernstein Equity Strategy Fund, the Eaton Vance Richard Bernstein All‐Asset Strategy Fund and the Eaton Vance Richard Bernstein Market Opportunities Strategy Fund and also offers income and unique theme‐oriented unit trusts through First Trust. RBA is also the index provider for the First Trust RBA American Industrial RenaissanceTM ETF and the First Trust RBA Quality Income ETF. Additionally, RBA runs ETF asset allocation SMA portfolios at UBS and Merrill Lynch and on select RIA platforms. RBA's investment insights as well as further information about the firm and products can be found at www.RBAdvisors.com.