What Happened to the Secular Bear Market in Equities?

History shows that US equity prices have consistently alternated between secular bull and bear trends. These price movements typically average 15-20 years in length and embrace several different business cycles. In April 2003 we published an article posing the question, “Whither the Secular Trend of Equities?” which laid out the case for the year 2000 being a secular or very long-term peak for the US stock market. Since the three previous secular bears averaged just over 18-years, our working hypothesis was for a weak market until sometime around 2018. Our view of continued secular vulnerability remains unchanged despite recent market strength.

Many point to record high equity prices in 2014 as evidence the secular bear ended in 2009 and the dominant trend is now a bullish one. That argument can be countered by the fact that record highs are nothing new in a secular bear market environment. For example, in 1909, seven years after the 1902 secular “peak”, prices were 16% higher (see point A in Chart 1). We see a similar situation between the 1960’s and 70’s, where the 1972 peak was 27% higher than that achieved 6-years prior (see point B in Chart 1) . The current differential between the November 2014 (so far) peak and that of August 2000 has been 36%. How, then, can we justify the label “secular bear” when nominal prices look otherwise?

Chart 1 - Nominal versus Inflation Adjusted US Stock Prices

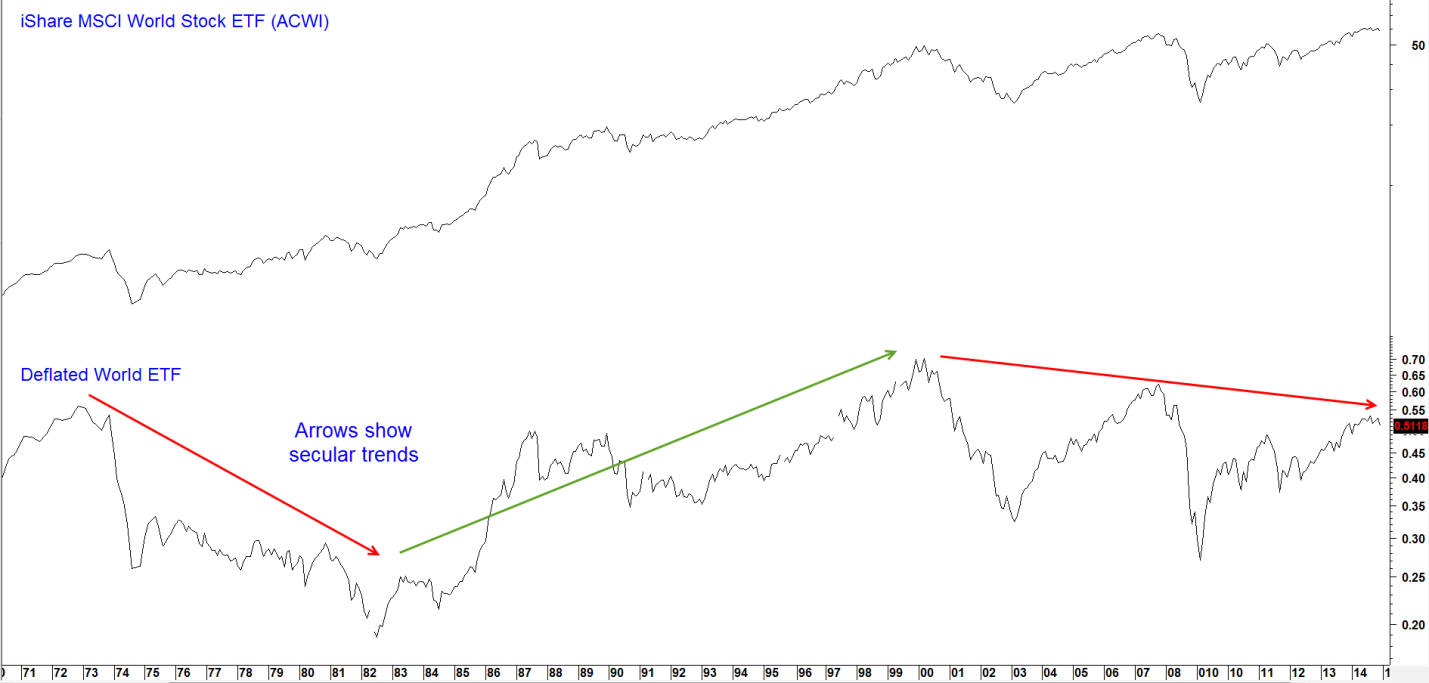

The answer lies in the fact that over very long periods, equity prices (adjusted for inflation) offer a far more realistic way of looking at things. After all, if my stock doubles in price over, say a 10-year a period, and this is replicated by the overall price level, am I any further ahead, in our book, Investing in the Second Lost Decade (McGraw-Hill, 2012) we pointed out that over short periods of time, inflation is not a big deal, but over longer intervals it becomes critical as inflation cunningly eats away at the real purchasing value of your portfolio. A comparison of the secular trading ranges in the nominally priced upper panel of Chart 1 with the bear trends of the inflation adjusted series in the lower panel demonstrates that difference pretty clearly. The chart also tells us that in late 2014 the adjusted price series had reached a critical juncture point, just fractionally below the 2000 high. The dashed brown lines and solid arrows show that previous secular peaks became important pivotal points in subsequent periods. Bottom line; now is as good a time as any for anticipating a primary trend peak. Chart 2 offers the same comparison, but this time between the nominal and inflation adjusted MSCI World Stock ETF. In this instance, the adjustment was made using the G7 CPI and the performance is even less robust than that of the US. Therefore, it is difficult not to conclude that the secular bear is both a US and global phenomenon.

Chart 2 - iShares MSCI World Stock ETF (ACWI)

The Causes of Secular Equity Bear Markets

1. Structural Problems

"We're seeing true currency wars and everybody is doing it, and I have no idea where this is going to end. The global elastic has been stretched even further than it was in 2008 on the eve of the Great Recession. The excesses have reached almost every corner of the globe, and combined public/private debt is 20% of GDP higher today. We are holding a tiger by the tail.” William White (Chairman of the OECD's Review Committee Daily Telegraph 1/21/2015

Secular bear markets do not develop in isolation but are the product of structural problems in the economy and financial system. In turn, these fundamental and monetary trends are reinforced by long-term swings in investor sentiment. Structural problems are most commonly caused by excessive capacity in key industries, either through overbuilding (housing 2006), new competition (steel between 1975 and 1990) or obsolescence because of technological advances (newspapers today, not a key industry, but a good example). In addition an aging population in developed countries offers another headwind as it means fewer spenders and producers. A final characteristic is a top-heavy debt structure, which adds the additional burden of higher servicing costs.

In the current cycle dating from 2000, earlier excesses associated with the dot.com bubble and housing have largely been worked off. However, demographic problems continue to act as a headwind, as does the 300% plus total debt/ GDP ratio. Even so, this pales in comparison to Japan’s 650% .

One way we can graphically symbolize one aspect of these long-term economic trends is to calculate the ratio between nonfarm payrolls (predominantly full-time employees) and those who work part-time for economic reasons.

Chart 3 - Secular Equity Trends and the Labor Market

This relationship is not only a great leading indicator for business cycle work, but its long-term trajectories also reflect secular trends in equities. When the ratio is rising, it indicates that full-time jobs are being created at a faster pace than part-time positions. This is a favorable factor because full-time jobs generally pay more and provide superior benefits. Also, an expansion in full-time as opposed to part-time workers demonstrates a stronger commitment by employers because full-time personnel are more difficult and expensive to fire. Returning to Chart 3, the shaded areas indicate secular bear trends in US equities. Such periods also correspond with a series of declining peaks and troughs in the labor market relationship in the lower window. This series typically peaks ahead of recessions, which have been flagged by the red highlights. At the start of 2015, there were no signs of business cycle weakness, but the indicator is still in a secular decline.

2. Giant Swings in Psychology

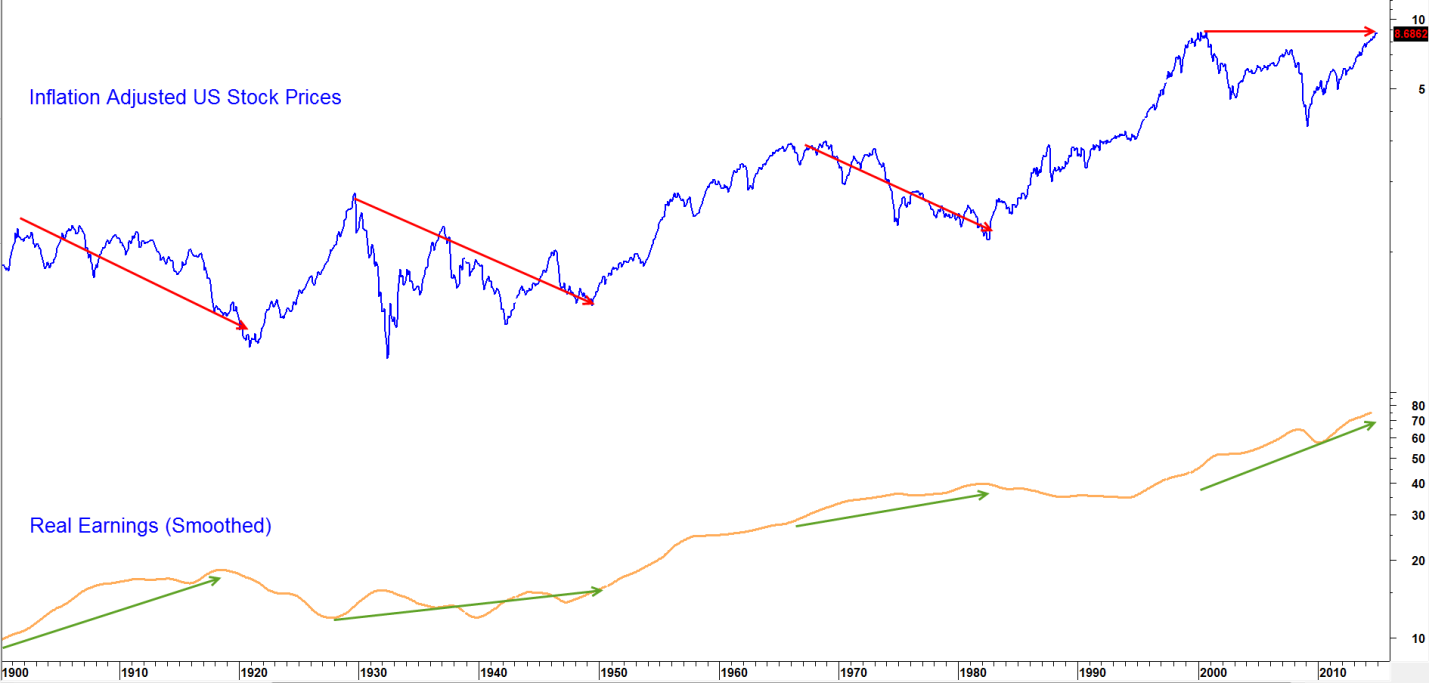

Most observers believe it is earnings that drive stock prices, but Charts 4 and 5 show that it is investor’s attitude to those earnings, rather than the earnings themselves, that is important. Consequently, an understanding of the secular trend is an appreciation of the fact that investors are continually undergoing long-term psychological mood changes, similar to the swing of a pendulum in a clock.

Chart 4 – Inflation Adjusted Stocks versus Real Earnings (Smoothed)

Chart 4 tracks a 10-year moving average of inflation adjusted profits compared to an inflation adjusted stock market series. Note how profits actually rise during the three secular bear markets.

Compare that relationship to the one in Chart 5, which reflects the attitude of investors to those earnings in the form of the Cyclically Adjusted Price Earnings (CAPE) ratio as published by Robert Shiller. A reading in excess of 22.5 indicates a high level consistent with a secular bull market peak. During the course of the subsequent secular bear this measure of valuation retreats to the 7 or 8 times level. At that point, the psychological foundation for a new secular bull is in place. It is important to note that when the P/E is excessive, investors are placing a very high valuation on those earnings. That means they are expecting them to continue to grow and are oblivious to the sustainability of that trend. In short, the only reason that investors are willing to buy at those levels is because they are extrapolating recent price trends into the future. In short, they are optimistic, excessively optimistic.

Chart 5 – Inflation Adjusted Stocks versus the Shiller P/E

By the same token, total disgust of equities sets in at secular lows because market participants have experienced 18 or so years of lower inflation-adjusted equity prices. Each rally brings hope, which is only dashed as prices sink to new lows. Under such an environment, it is only natural that investors demand to be paid handsomely for the huge risk they believe they are taking. Hence, the 18-20 year swing from exuberance and euphoria at the peak of the previous secular bull to despondency and despair at the start of the next one. The alternation of the red and green arrows in Chart 5 show this pendulum swing in crowd psychology has repeated with the consistency of clockwork over the last 114 years. Since secular bears are associated with structural problems, it is not surprising that they are characterized by numerous and frequent recessions. Is it any wonder that investors end such periods in a state of deep depression? Compare this environment to that of the 18-year secular bull market between1982-2000, which only experienced one period of contraction in 1990.

Returning to the current situation, the chart clearly shows that recent readings at the 27 level are closer to those at historical secular peaks than any previous secular low.

These giant swings in sentiment are not limited to P/E ratios, but can also be observed in similar swings in dividend yields from 2-3% at peaks to 6-7% at secular lows. For the record, the yield on the S&P in December 2014 was around 1.98%.

Chart 6 shows the Tobin Q ratio, which monitors swings in replacement value of US equities. This measure also moves in generational movements from around $1.05 at tops, to a discount whereby stocks sell at 30c on their replacement value at secular lows. According to the excellent Doug Short web site, the Tobin Q ratio was recently at $1.14, which is higher than any other secular peak except for the final years of the tech bubble. If past is prolog, we would expect to see these measures of valuation/sentiment return to levels closer to extreme pessimism before a solid foundation could be laid for a new secular bull. With the three valuation indicators at extreme levels, it makes sense to closely examine the state of the primary bull market. For if that is in the process of maturing, it is possible the secular bear might be about to resume.

Chart 6 – The Tobin Q Ratio (source: Dougshort.com/Advisorperspectives.com)

Source Advisorperspectives.com

The Cyclical Picture

“Two years of stocks going straight up have chased just about every skeptic from the U.S. market. Among professional forecasters on Wall Street, none tracked by Bloomberg sees a retreat in 2015…” Bloomberg 1/5/15

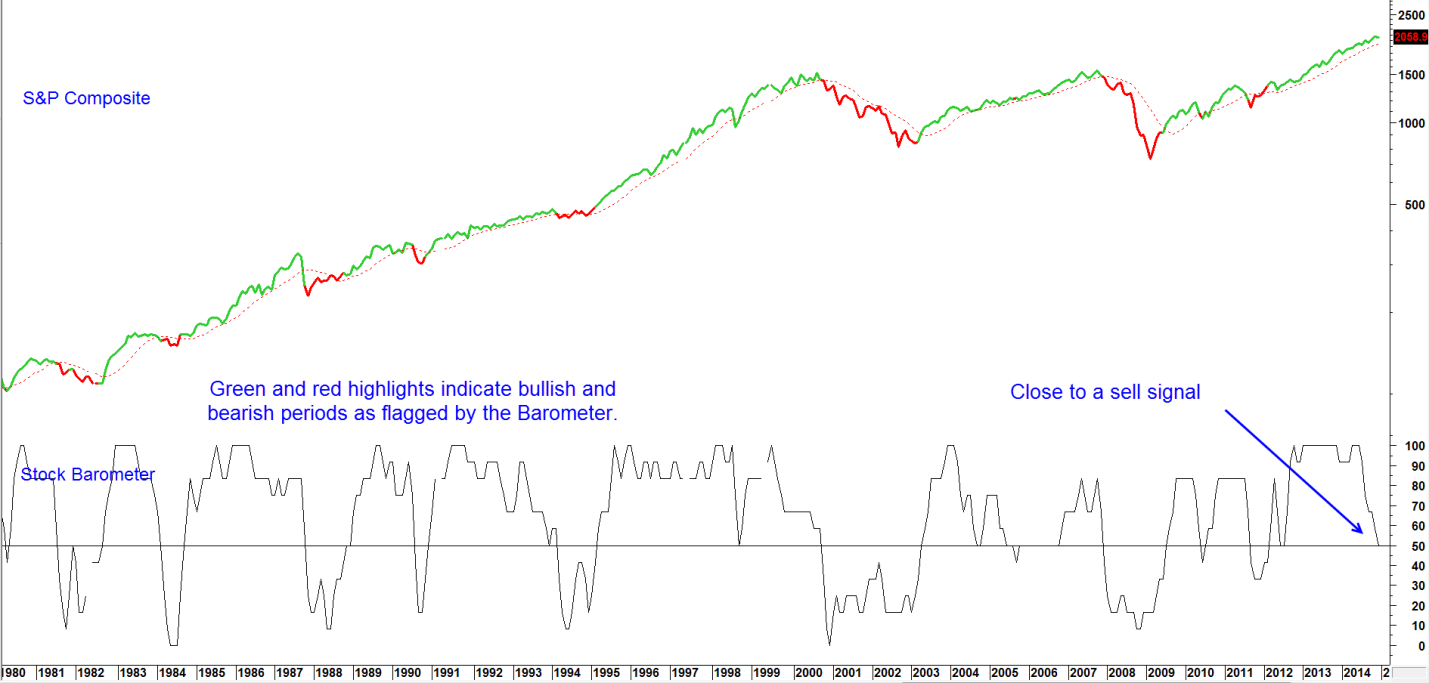

The current bull market is 5.8 years old, two years longer than the average of 3.8 years. There is nothing in the rule book that says it cannot continue, but in terms of time, the clock may well be approaching midnight; a view which is supported from the contrarian implications of the Bloomberg quote above. For example, our Stock Barometer, which consists of six technical and inter asset indicators, has recently been deteriorating and now stands at 50%. A reading below 50% is required for a bearish signal. That will not likely happen unless the S&P experiences an end of the month closing below its 12-month MA; that average was at 1945 in December. It is projected to advance close to the 1965 area in January. Until the Barometer actually goes negative, the benefit of the doubt should be given to the bull market. A summary of the Barometer’s performance from both 1955 and the start of the secular bear (2000) is presented in Table 1.

This model is updated monthly in the InterMarket Review at pring.com.

Chart 7 - S&P Composite versus the Pring Turner Stock Barometer

Table 1 - Stock Barometer Results 1955-2014

Even though the Barometer is currently bullish, the technical picture does not come without some risk. For example, the ratio between the Shiller P/E and government bond yields, shown in Chart 8, is one way of measuring equity returns against those of fixed income securities. The vertical lines indicate when this relationship first moves above the .75 (overvalued for stocks) level. As you can see, it pretty consistently signals a risky time to own equities. Nevertheless, as with all indicators, it does give false negatives from time-to-time as was the case in 1998, 2011 and 2012. However, the most recent reading at just above .95 is a record, even surpassing 1929 high. We are certainly not forecasting that a 1929-32 type bear will follow the current reading as this is a cyclical, as opposed to secular, indicator. However, given this extended reading, it is likely that equities would be extremely vulnerable in the event of a Stock Barometer sell signal.

Chart 8 - Inflation Adjusted US Stocks versus a Stock/Bond Valuation Indicator

Another way of comparing the stock/bond current return relationship is to calculate a smoothed momentum indicator for the ratio between Moody’s AAA Corporate bond yield and the dividend yield for stocks (Chart 9). Peaks in this momentum series have again consistently signaled primary trend tops in the equity market, as shown by the red arrows above the S&P. Nevertheless, there have been several failed signals, most notably those that developed in the 1990’s secular bull market, and are enclosed within the ellipse. The current situation is warning of problems, as the indicator has once again crossed below its MA.

Chart 9 - The S&P Composite versus Bond/Equity Yield Momentum

Finally, Chart 10 compares the ratio of NYSE margin debt to GDP to the inflation adjusted S&P. This series is currently close to a record. However, it is not the level that offers the best signals of trouble, but a change in trend, since downside reversals indicate when traders are growing more cautious.

Chart 10 - S&P versus Margin Debt to GDP

One way to identify such periods is to observe when the ratio crosses below its 15-month MA. This is indicated on the chart by a sub-zero crossover by the oscillator in the bottom panel. Previous instances have been flagged by the vertical lines. Those signals flagged with a small red arrow indicate when such signals have developed after a sharp decline, such as 1987 or 1998. At the moment, the model is still bullish since the ratio remains marginally above its MA. Clearly it would not take much in the form of a contracting number to trigger a signal. Note also that the ratio itself peaked in February and has not kept up with the S&P as is usually the case in a healthy situation.

Conclusion

The secular bear case has reached a critical juncture in that inflation-adjusted equity prices have moved back to their 2000 peak. Previous highs and lows often serve as important resistance points, which means that the secular bear case is about to be tested. Valuation/sentiment measures are currently at bullish extremes more typically associated with a secular high than low. Since they failed to move to the levels of extreme pessimism associated with previous secular lows, these indicators represent a missing piece of evidence in the secular bull case.

Moreover, several indicators that have consistently identified primary trend turning points in the past are flagging danger and that means that our next Stock Barometer sell signal is likely to be a prescient one. We are paying close attention but until then, enjoy the ride but definitely buckle up tighter than usual!

Martin Pring

*Pursuant to the provisions of Rule 206(4)-1 of the Investment Advisers Act of 1940, we advise all readers that they should not assume that all recommendations made in the future will equal that referred to in this material. Investing in securities involves risks, including the possibility of loss. Performance numbers include all retirement accounts. Performance includes total return (capital growth and dividends, after all costs)

Investment decisions formulated by Pring Turner Capital Group, Inc. are based on proprietary research and methods developed since 1977 by the owner/managers of the firm. None of the material contained herein is intended as a solicitation to purchase or sell a specific investment. Readers should not assume that all recommendations will be profitable or that future performance will equal that referred to in this material.