Bonds or Jeter?

It’s Barry Bonds not treasury bonds that we are comparing to Derek Jeter. The significant differences between these two players’ batting strategies seems to have relevance to the current market environment and, perhaps more importantly, to long-term investment success. Both former players achieved hitting success during their careers, but did so by following vastly different strategies.

Why worry about risk/return?

Diversification is not a free lunch. Despite what marketing materials might claim regarding higher returns accompanying lower risk, that combination is quite rare. There is a cost to diversification, and an effectively-diversified portfolio (notice we do not use the term “well-diversified”) will likely underperform the returns of each year’s best performing asset class. That is the cost of diversification. One’s portfolio can be effectively diversified and be more likely to produce steadier, albeit more boring, returns or one’s portfolio can ride a roller coaster of extraordinary returns and market volatility.

Investors’ responses to the recent stock market volatility seem to reflect that their portfolios are not effectively diversified. The Eaton Vance Top-of-Mind Index shows that investors are suddenly more worried about volatility than capital appreciation or tax efficiency. Theoretically though, if one’s portfolio was indeed effectively diversified, one would NEVER worry about volatility.

It seems ironic that there are numerous articles regarding particular managers’ high returns each year. Rewards are given out to hot managers and capital flows to their funds. However, there are few articles ever written that highlight longer-term risk-adjusted returns despite that surveys, like Eaton Vance’s, suggest risk-adjusted steady returns are what investors actually desire. Boring doesn’t make exciting headlines or receive recognition.

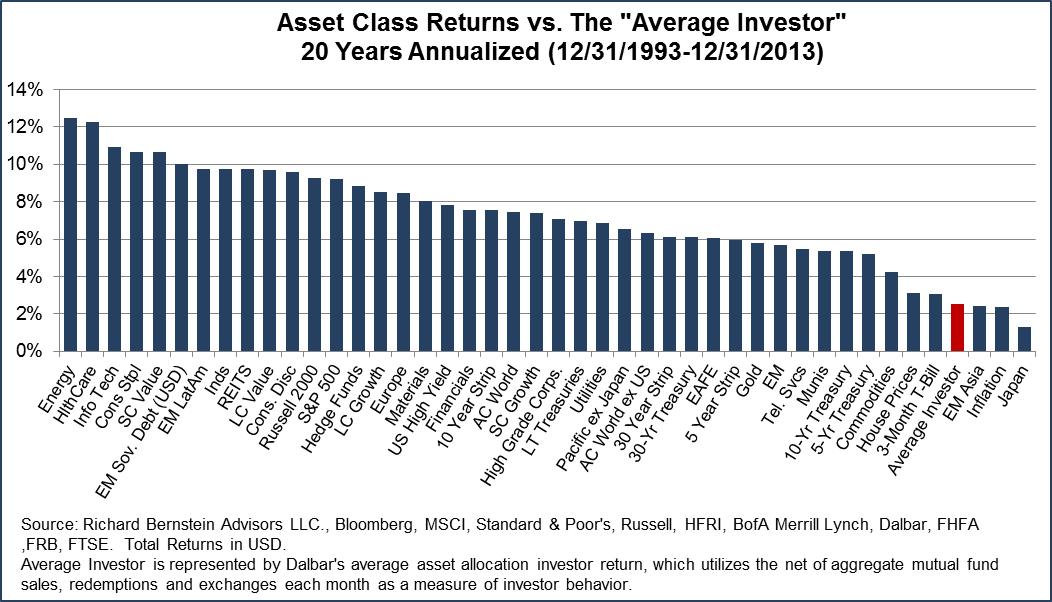

Following hot trends can be significantly detrimental to one’s investment performance. Chart 1 below shows the performance of the “typical” individual investor’s portfolio (as defined by Dalbar) versus a broad range of asset classes. Because investors tend to buy high (i.e., look for hot investments) and sell low (i.e., after being disappointed), investor performance has been abysmal.

Chart 1:

Risk/return in baseball

Risk/return tradeoffs are not limited to the financial markets. In baseball, hitters have a choice: they can swing for the fences and try to hit a home run or they can take a more accurate swing and try to get on base. Of course, the ultimate goal would be to hit a home run every at bat, but the statistics clearly show that is impossible. Singles outnumber home runs during every season demonstrating that there is indeed a risk/return tradeoff between trying to be a consistent, low-return singles hitter and trying to be a less consistent, high-return home run hitter.

A home run clearly has a bigger return than a single. Not only does the hitter’s team immediately score a run, but the home run might appear on the nightly TV sports roundup, which helps increase the home run hitter’s endorsement value. The probability of hitting a single is considerably higher than the probability of a hitting a home run, but the singles-hitter’s team must still work to score a run and, of course, how many ordinary singles are highlighted as the “play of the day”?

So baseball hitters must make a risk/return decision. Do they attempt to swing big for a home run with a higher payoff, but greater probability of failure or do they attempt to hit a single with a smaller payoff, but a higher probability of success?

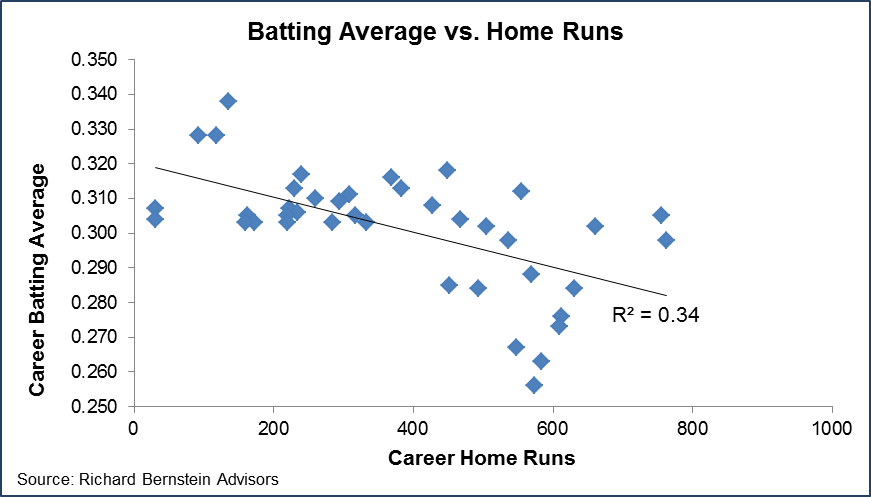

Charts 2 and 3 demonstrate this effect. Chart 2 shows the tradeoff between career home runs and batting average. The underlying sample is admittedly not scientific:

1) A player must no longer be an active player

2) Is among the lifetime leaders in batting average or home runs

3) Must have played during the post-expansion era

4) Had a career of fourteen years or more, and

5) I recognized their name!

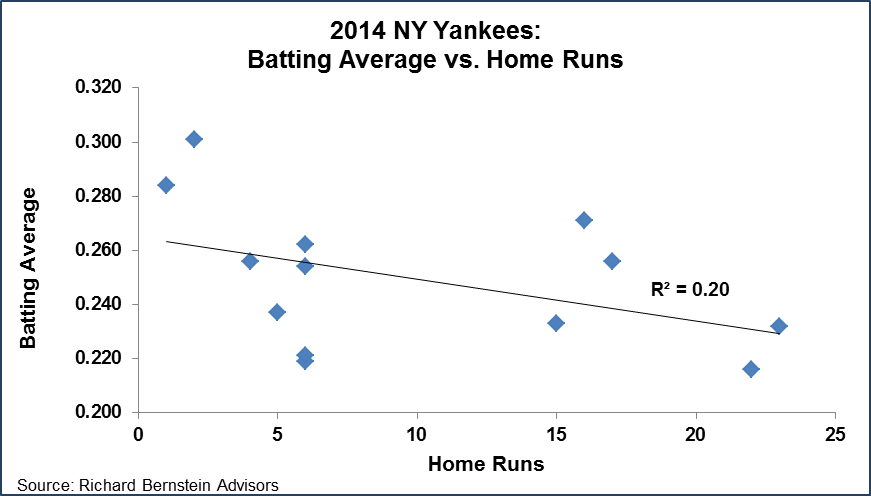

Chart 2 shows the same tradeoff among the New York Yankees players who played in at least 50 games during the 2014 season. In both cases, there is a negative relationship between batting average and home runs. In other words, if one swings for the fences, the odds are that one’s batting average will be lower.

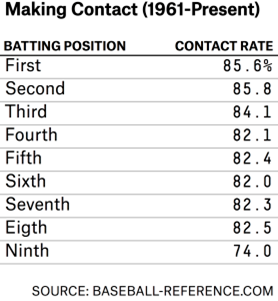

Data from Baseball-Reference.com shows the effect in a different way. Batters earlier in a batting order are expected to get on base, whereas a #4 hitter, the “clean up” hitter, is expected to swing away and drive the runners home. Table 1 shows that the #1 and #2 hitters have relatively high contact rates (i.e., their bat makes contact with the pitch), whereas the #4 hitter has one of the lowest contact rates. Note that the #9 data is skewed by pitchers hitting in the National League. This extremely large sample strongly supports our risk/return analysis, and suggests that hitters who attempt to simply get on base make contact more than hitters who swing for home runs.

Chart 2:

Chart 3:

Table 1:

Similarities to investing

There are many similarities between our small study on baseball risk/return tradeoffs and those in the financial markets. An investor has to decide whether they want to invest with a home run hitter or a consistent singles hitter. Home run hitters are the “managers of the year”, who often fail to repeat their single-year outstanding performances. Singles hitters talk about risk-adjusted returns, and rarely win awards. Of course, there is the occasional Miguel Cabrera, who manages to hit consistently with power, but they are exceptionally rare in both baseball and investing. Cabrera won the American League Triple Crown in 2012 (he led the league in home runs, runs batted in, and batting average), but he was the first player to achieve a Triple Crown in 45 years! Only fourteen players have won the Triple Crown since 1869. There aren’t many baseball players who can consistently hit home runs, and there aren’t many investment managers who can consistently hit investment home runs.

Inconsistency demands risk-adjusted returns

If one accepts that investment home runs are difficult to achieve with any consistency, then risk-adjusted returns become a critical component of longer-term investment success. Of course, there is a place in a portfolio for a home run hitter, but the entire investment plan should not be based on home run swings. As in baseball, the probability of an investment striking out increases as one attempts to hit a home run.

Here are some statistics that investors should examine when considering an investment:

1) Return

2) Standard deviation/volatility of return

3) The probability of losing money or falling below some needed investment return

4) Upside/downside capture, and

5) Skewness of the returns

PEDs?

Baseball has been riddled over the past decade or more with the accusations that players have been using performance enhancing drugs (PEDs). Some argue that PEDs allow players to achieve statistics that they otherwise could never produce.

Investing also has PEDs: leverage.

Leverage allows the manager to take a smaller swing and hit a home run. Leverage is used to enhance capital appreciation and to increase yields. Investors need to fully understand whether their managers are using PEDs within the portfolio and how those PEDs can accentuate the risk of a strategy.

Bonds or Jeter?

Investors must make a choice. Do they want Barry Bonds, Harmon Killebrew, and Jim Thome attempting to hit home runs but often striking out or do they want Rod Carew, Tony Gwynn, and Derek Jeter swinging more accurately for singles and doubles?

At RBA, our strategies are more akin to the hitting strategies of Carew, Gwynn, and Jeter. We want to make contact and try to get on base. We’ll hit our occasional home run, but we are unlikely to be featured as the “play of the day” on ESPN.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

MSCI All Country World Index (ACWI®): The MSCI ACWI® Index is a widely recognized, free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of developed markets.

S&P 500®: Standard & Poor’s (S&P) 500® Index. The S&P 500® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

U.S. Small Caps: Russell 2000 Index. The Russell 2000 Index is an unmanaged, capitalization-weighted index designed to measure the performance of the small-cap segment of the US equity universe. The Russell 2000 Index is a subset of the Russell 3000® Index.

Europe: MSCI Europe Index. The MSCI Europe Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of the developed markets in Europe. The MSCI Europe Index consists of the following 16 developed market country indices: Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland, Italy, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, and the United Kingdom

EM Equity: MSCI Emerging Markets (EM) Index. The MSCI EM Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of emerging markets.

MSCI BRICs. THE MSCI EM BRIC Index: The MSCI EM BRIC Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of Brazil, Russia, China and India.

Latam: MSCI EM (Emerging Markets) Latin America Index . The MSCI EM Latin America Index s a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of emerging markets in Latin America. The MSCI EM Latin America Index consists of the following 5 emerging market country indices: Brazil, Chile, Colombia, Mexico, and Peru.

Europe: MSCI Europe Index. The MSCI Europe index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of the developed markets in Europe. The MSCI Europe Index consists of the following 16 developed market country indices: Austria, Belgium, Denmark, Finland, France, Germany, Greece, Ireland, Italy, the Netherlands, Norway, Portugal, Spain, Sweden, Switzerland, and the United Kingdom.

Brazil: MSCI Brazil Index. The MSCI Brazil Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of Brazil.

Russia: MSCI Russia Index. The MSCI Russia Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of Russia.

India: MSCI India Index. The MSCI India Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of India.

China: MSCI China Index. The MSCI China Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity-market performance of China.

Gold: Gold Spot USD/oz Bloomberg GOLDS Commodity. The Gold Spot price is quoted as US Dollars per Troy Ounce.

Commodities: S&P GSCI® Index. The S&P GSCI® seeks to provide investors with a reliable and publicly available benchmark for investment performance in the commodity markets, and is designed to be a “tradable” index. The index is calculated primarily on a world production-weighted basis and is comprised of the principal physical commodities that are the subject of active, liquid futures markets.

Hedge Fund Index: HFRI Fund Weighted Composite Index. The HFRI Fund Weighted Composite Index is a global, equal-weighted index of over 2,000 single-manager funds that report to the HFR (Hedge Fund Research) database. Constituent funds report monthly net-of-all-fees performance in USD and have a minimum of $50 million under management or a twelve (12)-month track record of active performance. The Index includes both domestic (US) and offshore funds, and does not include any funds of funds.

REITS: THE FTSE NAREIT Composite Index. The FTSE NAREIT Composite Index is a free-float-adjusted, market-capitalization-weighted index that includes all tax qualified REITs listed in the NYSE, AMEX, and NASDAQ National Market.

3-Mo T-Bills: BofA Merrill Lynch 3-Month US Treasury Bill Index. The BofA Merrill Lynch 3-Month US Treasury Bill Index is comprised of a single issue purchased at the beginning of the month and held for a full month. The Index is rebalanced monthly and the issue selected is the outstanding Treasury Bill that matures closest to, but not beyond, three months from the rebalancing date.

Long-term Treasury Index: BofA Merrill Lynch 15+ Year US Treasury Index. The BofA Merrill Lynch 15+ Year US Treasury Index is an unmanaged index comprised of US Treasury securities, other than inflation-protected securities and STRIPS, with at least $1 billion in outstanding face value and a remaining term to final maturity of at least 15 years.

Intermediate Treasuries (5-7 Yrs): The BofA Merrill Lynch 5-7 Year US Treasury Index

The BofA Merrill Lynch 5-7 Year US Treasury Index is a subset of The BofA Merrill Lynch US Treasury Index (an unmanaged Index which tracks the performance of US dollar denominated sovereign debt publicly issued by the US government in its domestic market). Qualifying securities must have at least one year remaining term to final maturity, a fixed coupon schedule and a minimum amount outstanding of $1 billion. including all securities with a remaining term to final maturity greater than or equal to 5 years and less than 7 years.

Municipals: BofA Merrill Lynch US Municipal Securities Index. The BofA Merrill Lynch US Municipal Securities Index tracks the performance of USD-denominated, investment-grade rated, tax-exempt debt publicly issued by US states and territories (and their political subdivisions) in the US domestic market. Qualifying securities must have at least one year remaining term to final maturity, a fixed coupon schedule, and an investment-grade rating (based on an average of Moody’s, S&P and Fitch). Minimum size requirements vary based on the initial term to final maturity at the time of issuance.

High Grade Corporates: BofA Merrill Lynch 15+ Year AAA-AA US Corporate Index. The BofA Merrill Lynch 15+ Year AAA-AA US Corporate Index is a subset of the BofA Merrill Lynch US Corporate Index (an unmanaged index comprised of USD-denominated, investment-grade, fixed-rate corporate debt securities publicly issued in the US domestic market with at least one year remaining term to final maturity and at least $250 million outstanding) including all securities with a remaining term to final maturity of at least15 years and rated AAA through AA3, inclusive.

U.S. High Yield: BofA Merrill Lynch US Cash Pay High Yield Index. The BofA Merrill Lynch US Cash Pay High Yield Index tracks the performance of USD-denominated, below-investment-grade-rated corporate debt, currently in a coupon-paying period, that is publicly issued in the US domestic market. Qualifying securities must have a below-investment-grade rating (based on an average of Moody’s, S&P and Fitch) and an investment-grade-rated country of risk (based on an average of Moody’s, S&P and Fitch foreign currency long-term sovereign debt ratings), at least one year remaining term to final maturity, a fixed coupon schedule, and a minimum amount outstanding of $100 million.

EM Sovereign: The BofA Merrill Lynch US Dollar Emerging Markets Sovereign Plus Index. The BofA Merrill Lynch US Dollar Emerging Markets Sovereign Plus Index tracks the performance of US dollar denominated emerging market and cross-over sovereign debt publicly issued in the Eurobond or US domestic market. Qualifying countries must have a BBB1 or lower foreign currency long-term sovereign debt rating (based on an average of Moody’s, S&P and Fitch). Countries that are not rated, or that are rated “D” or “SD” by one or several rating agencies qualify for inclusion in the index but individual non-performing securities are removed. Qualifying securities must have at least one year remaining term to final maturity, a fixed or floating coupon and a minimum amount outstanding of $250 million. Local currency debt is excluded from the Index.

© Copyright 2015 Richard Bernstein Advisors LLC. All rights reserved.

PAST PERFORMANCE IS NO GUARANTEE OF FUTURE RESULTS

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor's investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment's value. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment's value. Past performance is, of course, no guarantee of future results. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.

About Richard Bernstein Advisors:

Richard Bernstein Advisors LLC is an independent investment adviser. RBA partners with several firms including Eaton Vance Corporation and First Trust Portfolios LP, and currently has $3.4 billion collectively under management and advisement as of December 31, 2014. RBA acts as sub‐advisor for the Eaton Vance Richard Bernstein Equity Strategy Fund, the Eaton Vance Richard Bernstein All‐Asset Strategy Fund and the Eaton Vance Richard Bernstein Market Opportunities Strategy Fund and also offers income and unique theme‐oriented unit trusts through First Trust. RBA is also the index provider for the First Trust RBA American Industrial RenaissanceTM ETF and the First Trust RBA Quality Income ETF. Additionally, RBA runs ETF asset allocation SMA portfolios at UBS, Merrill Lynch, Morgan Stanley Smith Barney and on select RIA platforms. RBA's investment insights as well as further information about the firm and products can be found at www.RBAdvisors.com.