Searching for Clarity Among the Dots

Fixed Income Outlook - April 2015

In 1886 Georges Seurat finished his most famous painting, A Sunday Afternoon on the Island of La Grande Jatte. Seurat used a new technique, Pointillism, in which small dots of color are applied to the canvas to express an image. More recently, Janet Yellen and the Federal Open Market Committee (the FOMC) updated their own version of Pointillism to express an image called the dot plot – a graphical representation of each FOMC member’s forecast of future federal funds (fed funds) rates. While Seurat’s “dot plot” ushered in a new era of impressionism, the FOMC’s dot plot has ushered in a new wave of confusion, questions and concern. Investors are confused about the health of the economy following recent economic releases, and they have questions about future interest rate actions given changes in the FOMC’s dot plot trajectory. The confusion is partially explained by the Fed’s challenge of evaluating the “data” in determining when is the best time to raise rates while balancing the complexities of their actions on the global economy. While investors continued to hope for image clarity, recent Fed minutes and Janet Yellen’s post meeting press conference have instead left people wondering “will she or won’t she?” We think the key question is when she finally does, can they manage the process without creating extreme volatility in the market?

Let’s revisit what got us here. To calm and stimulate markets following the economic collapse of 2008, the Fed cut the fed funds rate over 500 basis points (5%) and instituted three rounds of Quantitative Easing (QE). With risk-free rates at essentially 0%, investors moved out on the risk curve in their search for higher yields and returns. Prices of equities, emerging market debt and corporate bonds subsequently experienced healthy rallies. Fed thinking is that lower borrowing costs spur corporate investment and higher security prices, which in turn cause a wealth effect, leading investors to view the economy more positively. In theory, this should cause increased spending due to their newly increased wealth. The flipside is that excessive liquidity and risk taking potentially form financial bubbles. In addition, it effectively taxes savers and those on fixed incomes by decreasing current and future income on savings. While QE was supposed to be temporary, it has dragged on for over six years and bloated the Fed’s balance sheet to over $4.2 trillion. It did calm markets and generate some wealth effect, but investors have been slow to spend their newfound gains to stimulate the economy. This may be partially explained by the sluggish wage growth we have seen in this recovery and the desire for consumers to rebuild their balance sheets by increasing savings.

The Fed originally set targets (goalposts) for ending its QE stimulus and ultimately raising interest rates. These goalposts included a 6.5% unemployment rate (as measured by U-3) and a 2.0% inflation rate. While unemployment declined to 6.7% by Feb 2014, it clearly happened faster than the Fed expected so it moved the goalpost to 6.0%. As the unemployment rate continued to fall, the Fed continued to move the goalpost lower: to 5.5% in December 2014, to 5.2% in March 2015 and then suggested that it might like to see unemployment rate fall to below 5.0%. No wonder the market is confused. Core inflation (Consumer Price Index (CPI) less food and energy), on the other hand, has been a little slower to reach the Fed’s 2.0% target. Although it has been consistently above 1.5% on a rolling 12 month basis since the middle of 2011, it has not sustainably breached the 2.0% target. Could it be that the natural rate of inflation has shifted lower in the post-2008 economy, or is there another explanation? Certainly this recovery has been sub-par, and since the crisis consumers have been repairing their balance sheets and possibly delaying their purchases for longer than expected. Is it possible that the Fed data on inflation is faulty and behind the curve? We’ve been skeptical about the veracity of the CPI data for a while as it did not show much movement when real estate prices were jumping nationwide and the cost of energy was rising, leading up to the 2008 financial crisis. Nor has it moved much with the large increases in health care costs. It is so replete with various hedonic adjustments that it now likely bears little resemblance to the real world it is trying to measure.

Real world inflation may actually be on the rise. We are certainly seeing inflation at the high end evidenced by the recent record prices paid at classic car and art auctions. High end real estate is also fetching astronomic prices in New York, San Francisco and London. Additionally, the Billion Prices Project from MIT, which tracks prices from hundreds of websites to create a broad inflation index, has shown inflation rising since last year even though the U.S. Department of Labor data show the opposite. We are also beginning to see wage inflation as large retailers and at least one major fast food company have announced wage increases. Should companies begin to raise prices to counter increased wages paid, as opposed to squeezing their own profit margins, we could finally see upward pressure on inflation that might even show up in the core CPI measure used by the Fed.

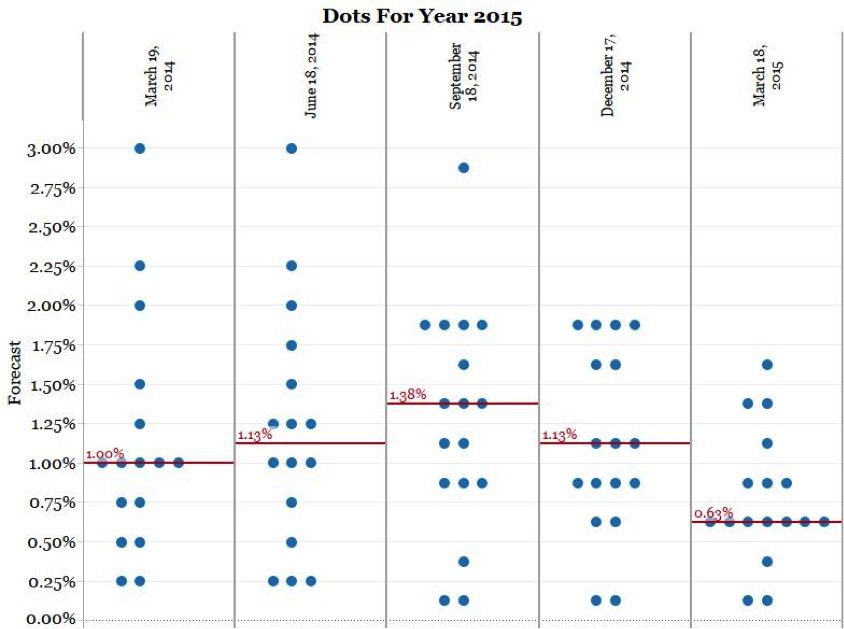

Despite having dropped the word “patient” from its forward looking guidance, the FOMC seems in no rush to raise rates. We expect they will be particularly “patient” as any Fed actions are likely to have global repercussions. As Janet Yellen explained in her most recent press conference, the FOMC is afraid of prematurely raising rates and choking off the recovery. As you can see, the dot plots below show that FOMC members have adjusted their 2015 median fed funds rate forecasts five times in the last 12 months. The last two adjustments were lowered following the weaker recent economic data (which may have been influenced by severe winter weather). The Fed is still data dependent, but it is not entirely clear to us what data the Fed is following. What is clear is that no one can accuse the Fed of being rash.

Source: Bianco Research, L.L.C.

We do believe that the situation in Japan and Europe is affecting the Fed’s decisions. While the U.S. economy has been slowly improving over the last several years, Japan and most of the European Union (the EU) have been struggling. Japan implemented its first round of QE in 2001 in response to its 1990s “lost decade” of growth and followed up with a larger, second round of QE in 2013. The latest round of so called Abenomics targeted $1.4 trillion of purchases by the end of 2014. The result of this has been a stock market rally (the Nikkei Index has risen over 115% since late 2012), a weak currency and very little Gross Domestic Product (GDP) growth. For the past 15 years, Japanese corporations have been the beneficiaries of government largesse while consumers and savers lost out. Given the long drought in interest income, Japanese consumers hoarded their savings and didn’t spend like the government needed them to. It’s not clear what the long-term outcome will be from Abenomics, but the results so far have been disappointing unless you count the large bubble also forming in Japanese bonds. The jury is still out as to whether there is also a bubble in equities or if it’s another in a series of false bear market rallies. There is cause for concern as these levels could deflate significantly once support from Abenomics is removed.

The EU seems to be following in Japan’s footsteps. They have in common a weak banking system, like Japan in the 1990s, and very low consumer growth combined with poor demographics (read: a low birth rate). Like Japan, European authorities did not inject massive amounts of capital into their banks following the 2008 recession, but instead took a laissez faire approach. They are now playing catch up, but the banks are still too precariously capitalized (despite passing the European Central Bank’s (the ECB’s) “easy-A” fitness tests) to do meaningful lending, much like the Japanese banks were in the 1990s. Although Europe at least has some immigration, it has many of the same structural issues that Japan faced 20 years ago. Growth in Europe has mostly been weak, and interest rate cuts by the ECB over the last several years have had little effect on calming nerves and stimulating economic growth. Not having learned from Japan and the U.S. regarding bubbles and the disincentives that QE causes for consumers and savers, the ECB announced its own asset purchase program this past March. To date, the program has driven interest rates down further (to where many countries now have negative rates), weakened the currency and rallied stock markets. Sound familiar? Negative interest rates are not normal, and economists have not prepared for a below zero-bound world. Negative yields ensure a loss if bonds are held to maturity, and as in Japan, the lower rates go, the more people feel the need to save creating a negative feedback loop.

Europe is a large export market and a desirable tourist destination, so it is possible that the low currency exchange rate will drive some growth. Of course, the irony of the ECB successfully generating growth and inflation is that investors in negative yielding bonds could see significant losses on their investments. Signs of positive growth from Spain and Germany might soon put policy makers to the test. It should be illuminating to see how the ECB will explain these “green shoots”, a rise in inflation and the appropriateness of negative yields in the same sentence. In addition, results out of Great Britain show good GDP growth over the last few years. It is interesting to note that Britain instituted its own form of QE in 2009 and stopped its purchases in 2012. This begs the question: if rates begin rising in Europe, what will happen to interest rates in the U.S.? Our guess is that they will begin the long awaited march upward.

In Seurat’s painting, his dots produce a clear image. We can’t say the same for the FOMC’s dots. The ever-changing plots, torturous language and a nebulous dependency on data have led to increased investor uncertainty. Also, it seems each time a Fed official gives a speech, his or her views conflict with those of other Fed officials who are also on the speaking circuit. At a minimum, this may indicate that there is a healthy debate within the Fed about when to raise rates. From where we sit, real world inflation is brewing, asset bubbles are growing and global QE has pushed investors into uncomfortably risky positions. Global central banks are in uncharted waters and the unwinding of QE followed by the normalization of interest rates could cause significant market volatility. In contrast, the British QE program was much smaller, so it cannot be used as a test case for the effects of unwinding. While we do know that central bankers are keenly aware of the risks caused by the bursting of asset bubbles, if history is a guide, they will likely remain blind to them until after the dams burst. While we do not know when or how the Fed is going to normalize interest rate policy, we do expect that it may involve significant dislocations, at least initially. At current levels in many asset classes, investors don’t seem to be getting compensated for moving out on the risk curve. Until that changes, we remain steadfast in our view that seeking to control risk while working to obtain moderate yields in shorter duration high yield and convertible securities is the most attractive alternative at this point. We continue to keep cash as dry powder for when we do get bouts of volatility and can layer in longer dated assets at attractive yields.

Past performance is no guarantee of future results. This commentary contains the current opinions of the authors as of the date above which are subject to change at any time. This commentary has been distributed for informational purposes only and is not a recommendation or offer of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but is not guaranteed.

No part of this article may be reproduced in any form, or referred to in any other publication, without the express written permission of Osterweis Capital Management.

Basis point is a unit that is equal to 1/100th of 1%.

U-3 is the total unemployed, as a percent of the civilian labor force (official unemployment rate).

Consumer Price Index (CPI) is a measure that examines the weighted average of prices of a basket of consumer goods and services, such as transportation, food and medical care.

Nikkei Index (Japan's Nikkei 225 Stock Average) is the leading and most-respected index of Japanese stocks. It is a price-weighted index comprised of Japan's top 225 blue-chip companies on the Tokyo Stock Exchange. The Nikkei is equivalent to the Dow Jones Industrial Average Index in the U.S.

One cannot invest directly in an index. [14141]

(c) Osterweis Captial Management

© Osterweis Capital Management