Gauging foreign demand for U.S. bonds, Treasuries in particular, is a constant source of attention for bond investors, with foreign ownership of outstanding U.S. Treasuries remaining fairly constant at approximately 50% over the past few years. The yield disparity between foreign and domestic government bonds remains near historically wide levels and continues to influence the bond market [Figure 1]. However, foreign buying interest alone does not account for price movements among high-quality bonds.

STILL BUYING

Last week’s release of Treasury International Capital (TIC) system data for February showed a decline in foreign purchases of U.S. Treasuries. Japan swapped places again with China as the largest foreign holder of U.S. Treasuries, but few additional insights emerged. The TIC data are significantly delayed and subject to sizable revisions, limiting their usefulness as a gauge of foreign bond buying.

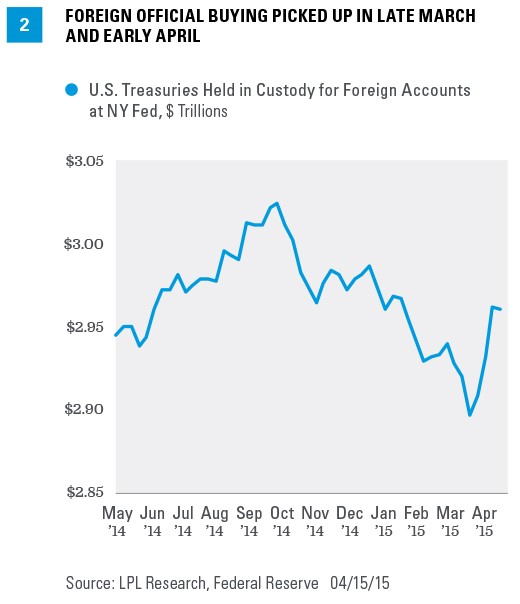

However, other data show foreign buying remains steady. A look at more timely data from the Federal Reserve Bank of New York shows that foreign buying decelerated from late February through most of March 2015, only to pick up again in late March through the start of April [Figure 2]. Bond prices increased in March and decreased at the start of April, almost exactly the opposite direction that foreign buying would indicate, which suggests more dominant forces are at work.

Classic drivers of bond prices and yields—economic growth and Federal Reserve (Fed) expectations—arose once again to dominate price action in the bond market, despite the presence of increased foreign buying. Specifically:

· Weaker economic growth. Disappointing economic results from February 2015 through early March revealed that economic growth was likely to slow from the sluggish 2.2% pace of the fourth quarter of 2014. Current forecasts for first quarter 2015 economic growth stand at 1.4%, according to Bloomberg. Weaker growth lowers the risk of Fed rate hikes and suppresses the odds that inflation breaks free of its stubbornly low range.

· Reduced Fed rate hike expectations. At the conclusion of its March 2015 meeting, the Fed announced significant reductions to projected overnight borrowing rates, suggesting a later start and slower pace of interest rate hikes. Bond prices rose and yields fell through the end of March in response.

Last week’s weaker than expected monthly retail sales report reiterated the impact of economic data. Retail sales fell short of expectations and consumer spending remains lackluster to start 2015, despite savings from lower energy prices. The consumer spending data led to a reversal of a weak start to the second quarter of 2015 for the bond market.

Details of recent Treasury auction results show a gradual increase in foreign demand for new Treasuries, offset by weaker domestic demand. The percentage of auctions awarded to “indirect bidders”—a group of investors who submit bids for auctions via the New York Fed, a majority of which are foreign central banks and monetary authorities—has gradually increased over the last several months [Figure 3]. Even the 30-year Treasury bond auction, a security that historically has not witnessed much foreign demand, has seen a modest increase in the amount awarded to indirect bidders since the middle of 2014.

At the same time, demand from domestic investors has waned as low yields have reduced demand. The percentage of recent auctions awarded to “direct bidders” — – a group of investors that bids directly through the Treasury rather than through a bond dealer—has gradually decreased in recent months [Figure 3] to less than 10% across the auction maturities shown, down from 10–20% for most of 2014. Although foreign demand remains firm, it has been offset by weaker domestic demand.

CHANGING MIX

Overall, the pace of foreign buying has slowed in recent years but remains a steady and firm presence in the bond market. Foreign institutions, such as central banks, have slowed their purchases, and weaker economic growth abroad has reduced excess reserves that are typically invested into Treasuries. But as institutions have reduced their involvement, others have taken up the slack to keep foreign interest in the U.S. bond market elevated. Additionally, TIC data reveal demand for other sectors, such as corporate bonds, has strengthened, while Treasury purchases have slowed.

Still, charting total foreign holdings of Treasuries shows that while the pace of buying has slowed, it nonetheless remains on pace with overall growth of the outstanding Treasury market [Figure 4].

Foreign domiciled investors remain a source of support for the U.S. bonds as recent data attest to. Nonetheless, classic drivers of bond prices and yields—economic growth and Fed rate expectations—will continue to potentially have a greater impact on the direction of bond yields.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values and yields will decline as interest rates rise, and bonds are subject to availability and change in price.

Government bonds and Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

Investing in foreign fixed income securities involves special additional risks. These risks include, but are not limited to, currency risk, political risk, and risk associated with foreign market settlement. Investing in emerging markets may accentuate these risks.

Corporate bonds are considered higher risk than government bonds but normally offer a higher yield and are subject to market, interest rate, and credit risk as well as additional risks based on the quality of issuer coupon rate, price, yield, maturity, and redemption features.

High-yield/junk bonds are not investment-grade securities, involve substantial risks, and generally should be part of the diversified portfolio of sophisticated investors.

DEFINITION

Treasury International Capital (TIC) is select groups of capital that are monitored with regards to their international movement. Treasury International Capital is used as an economic indicator that tracks the flow of Treasury and agency securities, as well as corporate bonds and equities, into and out of the United States. TIC data are important to investors, especially with the increasing amount of foreign participation in the U.S. financial markets.