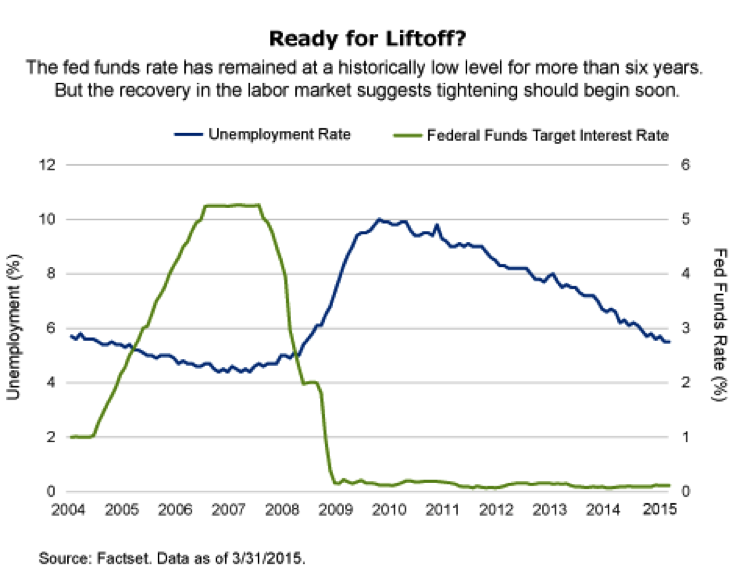

It's a big week for the Federal Reserve—and investor confidence. Concerns over rate hikes and economic growth have gripped the markets tighter than usual recently. The Federal Open Market Committee holds its regular monthly meeting—beginning on Tuesday—to discuss the state of the economy and debate when to begin raising the federal funds rate. The Fed has waited a long time to raise rates. In fact, the Fed has kept rates extremely low since December 2008. You may recall the Fed raised its benchmark interest rate from late 2004 until the middle of 2006 in an attempt to prevent the economy from overheating and to keep inflation in check. However, in September 2007, the Fed took a policy U-turn in response to the housing crisis. The Fed began to lower rates very rapidly, and in a little more than a year, lowered the federal funds rate from 5% to the 0%-0.25% band it remains in today. Six years is a long time. In 2007, my youngest child was just a year old—bald and hardly talking—when the Fed brought rates down to their current level. Now he's in the second grade, sporting a full head of hair and tackling common core math. Similarly, the US economy has made a lot of progress. In December 2008, the unemployment rate was 7.3%; it climbed to its peak of 10% in October 2009 and then began falling. Today, the unemployment rate stands at 5.5%.

Suffice it to say that the Taylor Rule, which fairly accurately predicted the fed funds rate from 1988 through 2008, might as well be in my attic with my Duran Duran albums, Benetton rugbies and other vestiges of the '80s and '90s.

Weather or Not?

What will happen at the April FOMC meeting? First let's cover what won't happen. We're very confident that the Fed will not announce a hike in rates at this meeting. But we think a lot will happen at this meeting. Recall Fed Chair Janet Yellen's pledge that decision-making will be data dependent rather than date dependent. As a result, we expect FOMC members to spend a lot of time assessing how poor the first quarter was, and whether the factors contributing to the downturn were temporary in nature. In other words, how much of the slowdown was due to bad weather as opposed to the strong dollar and low oil prices? We need to pay close attention to the FOMC's view on this because of what it suggests about economic growth potential going forward.

In addition, FOMC members will be analyzing initial second-quarter economic data to gain insight into where growth is headed. If the earliest the Fed will move is at its June meeting, then it needs enough information to inform its decision. While it seems increasingly unlikely that liftoff will begin in June given the poor first-quarter data and initial second-quarter data that is weak, we can't entirely rule it out—at least not until we see more published data. But we'll need to see an improvement soon in order for the Fed to act in June.

No Free Lunch

Still, there is a small chance that the economy stalls. Our base case is that the economy will improve in the second quarter and beyond, driven largely by a moderate increase in consumer spending. If there's no rate hike in June, then we think it's likely that the Fed will begin liftoff in July or September. Yellen will likely try to communicate those intentions in advance, just as Ben Bernanke did with the start of tapering in 2013 in an attempt to mitigate extreme market reactions. But it may not work. As a research paper released by the University of Chicago last year suggests, "Stimulus now is not a free lunch, and it comes with a potential for macroeconomic disruptions when the policy is lifted."

Disruptions are likely to occur given the mismatch between market expectations and what we think the Fed will do. Investors need to keep in mind that the Fed will act in advance of reaching its goals, as Yellen made clear in a March speech: "…policymakers cannot wait until they have achieved their objectives to begin adjusting policy." That means there could be a situation where the Fed's actions seem out of sync with current economic data. Simply put, the Fed is taking a long-term view of monetary policy. At the April meeting, we expect FOMC participants to spend some time on the mechanics of raising rates. We need to hear that the Fed, after testing its tools, is comfortable that it can achieve the desired fed funds target range when the FOMC is ready to raise rates. This is critical in advance of any decision on liftoff. Overall, look for short-term volatility to increase and expect to be surprised. But don't let that scare you. We think ultimately the market will be soothed by the Fed's commitment to data dependency in determining the path of rates, which is likely to remain lower for longer. We can't stress enough that the path is far more important than the liftoff date. Pay attention to the FOMC minutes, but don't let them dictate investment decisions. Just as I have had to reluctantly let my baby grow up, the Fed will eventually have to let short-term rates rise.

The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Past performance of the markets is no guarantee of future results. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities. A Word About Risk: Equities have tended to be volatile, involve risk to principal and, unlike bonds, do not offer a fixed rate of return. Foreign markets may be more volatile, less liquid, less transparent and subject to less oversight, and values may fluctuate with currency exchange rates; these risks may be greater in emerging markets.

© Allianz Global Investors Distributors LLC

AGI-2015-04-27-12061