A weak finish to the month of April 2015 was “made in Europe” as expectations of better global growth weighed on bonds. On Monday, May 4, 2015, the 10-year German government bond yield closed at 0.45%, more than quadrupling over the past two weeks. European strength combined with a dovish Federal Reserve (Fed) meeting outcome continued to arrest U.S. dollar strength, a primary driver of the steady decline in inflation and investors’ inflation expectations from mid-2014 through the first quarter of 2015. In turn, forward-looking financial markets anticipate that a halt in U.S. dollar strength may not only help reverse inflation expectations, but also remove a burden to profit growth of multinational U.S. companies.

European market moves overshadowed another round of weaker than expected U.S. economic data, which would normally have supported bond prices. Although a soft reading on first quarter 2015 economic growth was expected, the miserly 0.2% growth rate continued to dampen expectations of a substantial rebound for the current second quarter. A lower reading on the Institute of Supply Management (ISM) manufacturing survey also indicated a sluggish second quarter growth pace.

If the data were not enough, the Fed’s latest meeting (April 28–29, 2015) concluded with a market-friendly announcement that acknowledged first quarter economic weakness. The Fed viewed first quarter weakness as transitory, but recent economic reports have failed to fully corroborate that notion.

Taken together, the soft economic data and dovish Fed meeting outcome would have normally helped push bond prices higher, but forward-looking markets read between the lines. Fading U.S. dollar strength, better growth in Europe, and the rebound in oil prices point to a reversal of the lower inflation expectations that powered bond strength for most of 2014 and early 2015.

GROWTH SIGNALS

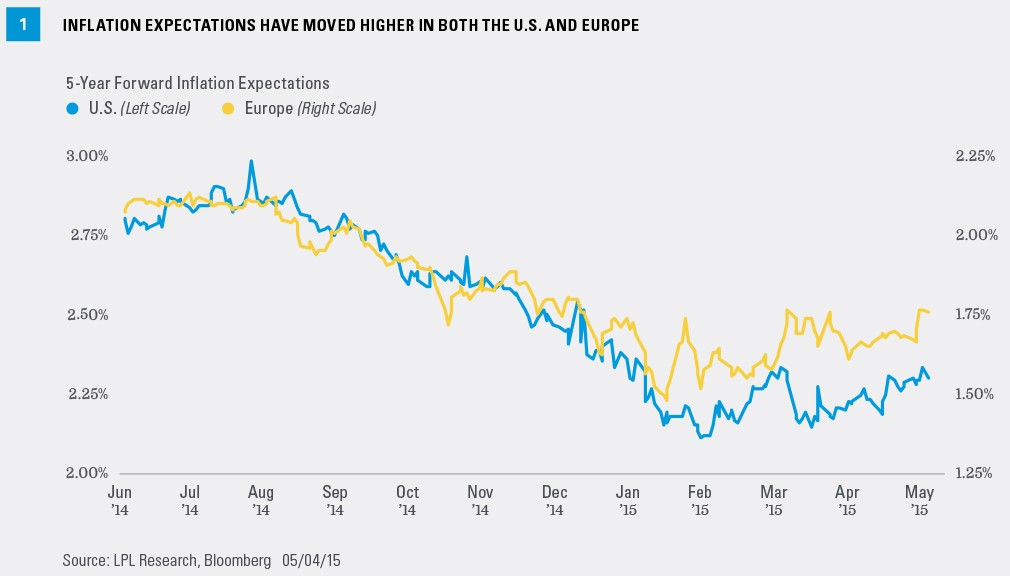

Inflation expectations—both in Europe and the U.S.—have been volatile, but moving higher [Figure 1]. These market-based measures of inflation expectation are closely monitored by central banks, and the Fed in particular may follow through with a long-expected interest rate increase should inflation expectations continue to rise from here. Consumer inflation expectations as measured by last Friday’s release of the University of Michigan consumer sentiment survey also pointed higher. Together they may incrementally build the Fed’s case to raise interest rates.

Growth signals were not limited to rising inflation expectations as global yield curves continued to steepen. Long-term yields rose more than short-term yields, leading to the steepening move. Yield differentials between 2- and 10-year maturity Treasuries and German government bonds also increased.

A position imbalance likely contributed to bond weakness as the amount of long-term U.S. government bonds held by bond dealers had increased to a multiyear high [Figure 2]. The European bond sell-off created an opportunity for investors to unload positions and reduce interest rate risk. Position extremes, either significant long positions or net short positions, can be contrarian in nature and signal a reversal. Dealers unloading positions may have exacerbated weakness as they back away from market-making activities leading to illiquid trading conditions. Price moves can be intensified under such circumstances.

LATE APRIL SHOWER

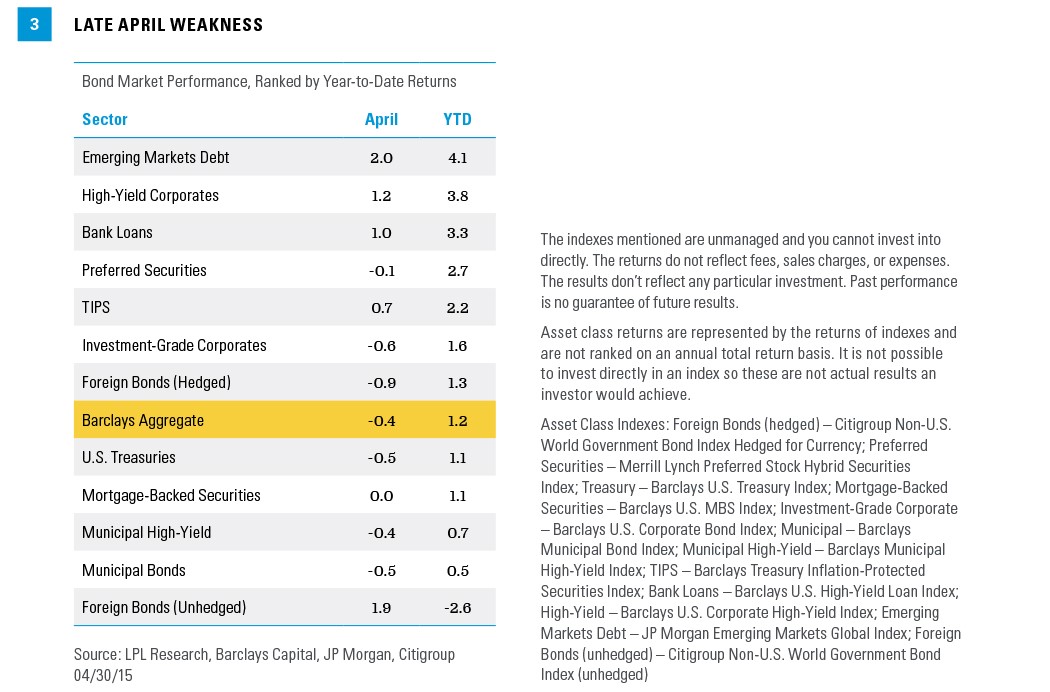

Late April weakness led to a poor month of bond performance overall as several bond sectors registered losses [Figure 3]. A reversal, given the strong start to bond performance in 2015, is not entirely surprising and speaks to the more challenging return environment we envision ahead. The last time a growth scare pushed yields higher to a similar degree occurred in September of last year but improvement in Europe gives this latest episode a different feel.

KEY INDICATORS

The 30-year Treasury bond has set the direction for the overall bond market over the past two years and may indicate whether current weakness has run its course. In 2013, the yield on the 30-year Treasury bottomed a few days before yields on other Treasury maturities did the same. If the 30-year Treasury yield sustains a breach above a 2.83% yield, the recent peak and a boundary of the recent yield range, then additional weakness may ensue and higher yields may follow across the maturity spectrum. Similarly, the 10-year German Bund sits near a 0.40% yield, and a break above would mean the current slide continues. Both benchmarks may be the first to usher in more widespread moves across bond markets.

On the economic front, the April employment report, which will be released Friday, May 8, 2015, will be the next key fundamental data point. A disappointing jobs report may question forward-looking growth expectations and bond prices may rebound, while a stronger report may only add fire to the weak sentiment in the bond market. April bond performance is a reminder of the ups and downs investors may expect in what we continue to be a very low return environment in 2015.

IMPORTANT DISCLOSURES

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values and yields will decline as interest rates rise, and bonds are subject to availability and change in price.

Government bonds and Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

Investing in foreign fixed income securities involves special additional risks. These risks include, but are not limited to, currency risk, political risk, and risk associated with foreign market settlement. Investing in emerging markets may accentuate these risks.

High-yield/junk bonds are not investment-grade securities, involve substantial risks, and generally should be part of the diversified portfolio of sophisticated investors.

Mortgage-backed securities are subject to credit, default, prepayment risk that acts much like call risk when you get your principal back sooner than the stated maturity, extension risk, the opposite of prepayment risk, market and interest rate risk.

Municipal bonds are subject to availability, price, and to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rate rise. Interest income may be subject to the alternative minimum tax. Federally tax-free but other state and local taxes may apply.

INDEX DESCRIPTIONS

The Barclays U.S. Aggregate Bond Index is a broad-based flagship benchmark that measures the investment-grade, U.S. dollar-denominated, fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS, and CMBS (agency and non-agency).

Barclays U.S. High-Yield Loan Index tracks the market for dollar-denominated floating-rate leveraged loans. Instead of individual securities, the U.S. High-Yield Loan Index is composed of loan tranches that may contain multiple contracts at the borrower level.

The Barclays U.S. Corporate High-Yield Index measures the market of USD-denominated, noninvestment-grade, fixed-rate, taxable corporate bonds. Securities are classified as high yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below, excluding emerging market debt.

The Barclays U.S. Corporate Index is a broad-based benchmark that measures the investment-grade, U.S. dollar-denominated, fixed-rate, taxable corporate bond market.

The Barclays U.S. Mortgage Backed Securities (MBS) Index tracks agency mortgage backed pass-through securities (both fixed rate and hybrid ARM) guaranteed by Ginnie Mae (GNMA), Fannie Mae (FNMA), and Freddie Mac (FHLMC)

The Barclays U.S. Municipal Index covers the USD-denominated long-term tax-exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds, and pre-refunded bonds.

The Barclays Municipal High Yield Bond Index is comprised of bonds with maturities greater than one-year, having a par value of at least $3 million issued as part of a transaction size greater than $20 million, and rated no higher than ‘BB+’ or equivalent by any of the three principal rating agencies.

The Barclays U.S. Treasury TIPS Index is a rules-based, market value-weighted index that tracks inflation-protected securities issued by the U.S. Treasury.

The Barclays U.S. Treasury Index is an unmanaged index of public debt obligations of the U.S. Treasury with a remaining maturity of one year or more. The index does not include T-bills (due to the maturity constraint), zero coupon bonds (strips), or Treasury Inflation-Protected Securities (TIPS).

The BofA Merrill Lynch Preferred Stock Hybrid Securities Index is an unmanaged index consisting of a set of investment-grade, exchange-traded preferred stocks with outstanding market values of at least $50 million that are covered by Merrill Lynch Fixed Income Research.

The Citi World Government Bond Index (WGBI) measures the performance of fixed-rate, local currency, investment-grade sovereign bonds. The WGBI is a widely used benchmark that currently comprises sovereign debt from over 20 countries, denominated in a variety of currencies, and has more than 25 years of history available. The WGBI provides a broad benchmark for the global sovereign fixed income market. Sub-indexes are available in any combination of currency, maturity, or rating.

The JP Morgan Emerging Markets Bond Index is a benchmark index for measuring the total return performance of international government bonds issued by emerging markets countries that are considered sovereign (issued in something other than local currency) and that meet specific liquidity and structural requirements.

DEFINITIONS

The presidents of regional Federal Reserve Banks are commonly classified as hawks or doves. Hawks generally favor tighter monetary policy, with less monetary support from the Federal Reserve. Doves are the opposite, generally favoring easing of monetary policy.

The U.S. Institute for Supply Managers (ISM) manufacturing index is an economic indicator derived from monthly surveys of private sector companies, and is intended to show the economic health of the U.S. manufacturing sector. A PMI of more than 50 indicates expansion in the manufacturing sector, a reading below 50 indicates contraction, and a reading of 50 indicates no change.

The Michigan Consumer Sentiment Index (MCSI) is a survey of consumer confidence conducted by the University of Michigan. The MCSI uses telephone surveys to gather information on consumer expectations regarding the overall economy.