Last week was a big one for Federal Reserve communications, and we should be listening to what’s being said. The FOMC minutes were released on Wednesday and Fed Chair Janet Yellen delivered the Fed’s outlook for the economy on Friday. On Monday, Fed Vice Chair Stanley Fischer gave a speech in Israel, reiterating that economic data will drive its decision on when to raise rates.

Central bankers have been vocal in their emphasis of weighing the path of interest rates over the timing of liftoff, but that doesn’t mean investors in certain asset classes should not heed the implications of the first interest-rate hike in nearly a decade.

The FOMC minutes confirmed that a liftoff in June is unlikely, as expected, given its view that the economic data that will be available ahead of the June meeting is unlikely to be strong enough to raise short-term interest rates. There was a discussion about consumer spending weakness and its causes and persistence. While some members felt there were factors beyond the weather involved, the consensus was that there was nothing too concerning.

Inflation Debate Rages On

Some FOMC members suggested there was a seasonal pattern of weakness in the first quarter followed by a revival. They expected real economic activity to resume expansion at a moderate pace. In addition, there was continued debate about why inflation is so low, an issue that’s clearly vexing many FOMC members.

However, the most important takeaway came from the FOMC’s discussion of recent market developments and financial stability. FOMC participants discussed the low level of term premiums and the possible risks created by that situation. Some FOMC participants noted the possibility that, at the time when they decide to begin liftoff of the federal funds rate, term premiums could rise sharply—similar to the 2013 taper tantrum—which might drive longer-term interest rates higher.

Additionally, they discussed how bond prices are likely to exhibit more volatility in the future than they had in the past for a variety of reasons, including the increased role of high-frequency traders, falling inventory of bonds held by broker-dealers and elevated bond fund assets.

Bonds, Not Stocks, Overvalued

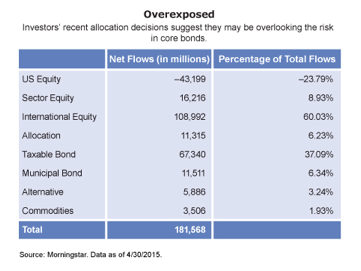

To be sure, investors need to take these potential risks seriously. That’s particularly important because bonds have been directly manipulated by the Fed and many investors are overweight core bonds. So far in 2015, we’ve seen 45% of overall mutual fund flows move into equity funds while almost as many dollars—more than 37% of flows—have been invested in taxable bond funds. And while we think investors are well aware of stock-market risks such as stretched valuations and disappointing earnings, we’re not entirely sure they’re seeing the full risk picture. In fact, the greater risk may lurk in core bonds, which is arguably even more richly valued than the stock market.

For greater clarity, think of the Sharpe ratio, a metric used to estimate risk-adjusted returns. It’s a helpful way to compare individual securities or mutual funds. It can even be used to compare different asset classes. However, because it’s backward-looking—using historical return and historical standard deviation—it can be misleading, particularly if volatility is expected to increase in the future. And that’s exactly what the Fed is anticipating. Investors may be willing to take on the risk of core bonds, assuming that if returns are low, then risk will likely be low too. But what if the risk is actually much higher?

Underestimating the Risks of Core Bonds

If investors expected higher volatility, then they may not be as inclined to hold core bonds. In addition, they have to worry about some of the collateral damage of financial repression—like capital depreciation. If longer-term rates move higher, then prices will move lower, resulting in a decrease in the value of their bonds.

So while we continue to hear members of the FOMC discuss the importance of focusing on the path of rates rather than the liftoff date, we have to worry about the implications of liftoff for certain asset classes. And that may occur sooner than many market participants think. While we expect this event to create volatility in stocks, we’re far more concerned about its impact on the bond market.

What’s an investor to do? The first step is to recognize the risks. Then investors can choose whether or not to reduce exposure to areas such as core bonds and reallocate to a well-diversified, actively managed multi-asset investment. Interestingly, only 6% of fund flows this year have moved into asset allocation funds. Yet those funds may be an appropriate choice for investors, enabling them to pivot to embrace opportunities and to avoid risks as they unfold. Like the Fed, investors need to be nimble.*

Kristina Hooper, CFP, CAIA, CIMA, ChFC, is the US investment strategist and head of US Capital Markets Research & Strategy for Allianz Global Investors. She has a B.A. from Wellesley College, a J.D. from Pace Law and an M.B.A. in finance from NYU, where she was a teaching fellow in macroeconomics.

Subscribe Today

The Upshot is available as a subscription for financial professionals only. New issues will be delivered via email every Monday. Visit us.allianzgi.com/theupshot to learn more.

The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Past performance of the markets is no guarantee of future results. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities.

A Word About Risk: Equities have tended to be volatile, involve risk to principal and, unlike bonds, do not offer a fixed rate of return. Foreign markets may be more volatile, less liquid, less transparent and subject to less oversight, and values may fluctuate with currency exchange rates; these risks may be greater in emerging markets.

There is no guarantee that an active manager’s investment decisions and techniques will be successful. It is possible to lose some or all of your investment using active management.

Allianz Global Investors Distributors LLC, 1633 Broadway, New York NY, 10019-7585, us.allianzgi.com, 1-800-926-4456.

AGI-2015-05-26-12348