IN THIS ISSUE

- Federal Reserve Grapples with Mixed Data

- Multiple Central Banks Still in Easing Mode

- Europe Has Bond Market Hiccup

Federal Reserve Grapples with Mixed Data

Having come through 2015’s first quarter with virtually no growth, the US economy is generally expected to pick up during the rest of this year. Indeed, as we move into a new quarter and shake off the effects of a significant West Coast dock strike and severe winter weather, forward indicators have pointed toward better growth. The Institute for Supply Management’s (ISM’s) purchasing managers’ index for nonmanufacturing rose to 57.8 in April, well above the 50 mark that separates expansion from contraction, suggesting that activity in the US services sector—which accounts for the lion’s share of the American economy—has continued to march higher.

At the same time, the ISM reading for the manufacturing sector has weakened somewhat, perhaps reflecting the adverse effects of a strong US dollar, which has also cut into exports and the first-quarter corporate earnings of big American multinationals. Meanwhile, global growth has continued to disappoint, US inflation has remained well below the Federal Reserve’s (Fed’s) medium-term target, and US productivity growth has stagnated, leaving the country’s growth potential in question.

These competing forces continue to make the path toward interest-rate normalization particularly tricky for the Fed. In an April statement, the Federal Open Market Committee (FOMC) said that it believed the first-quarter weakness seen in the United States was “transitory.” But with few signs that growth and inflation are likely to run out of control, the FOMC has, no doubt wisely, signaled that it would wait for further indications that job creation is picking up again and that inflation looks to be getting closer to its 2% target before making its anticipated move toward some gradual tightening of monetary policy.

But circumstances may be changing somewhat. The dollar strength that had served as a brake on the US export economy gave way to dollar weakening in late April, while increases in oil prices have been much more rapid than many observers expected. By early May, the cost of Brent crude oil was approaching US$70 per barrel, over 50% higher than its low point in January. Not surprising, therefore, inflation expectations have also been rising. The rise in inflation expectations may also account for the rise in consumer spending. After a slump in retail sales in March, consumer spending showed signs of picking up again in April, according to the Bureau of Economic Analysis.

Even more importantly, the April nonfarm payrolls figure showed a significant pickup in job creation, after a very soft March number. With 223,000 jobs created in April and the unemployment rate falling to 5.4%, according to the Bureau of Labor Statistics (BLS), the improvements in the US labor market seem well entrenched and indicate that the United States may soon reach “full employment.” In light of recent trends, we believe the United States should soon hit the Fed’s estimated level of the natural rate of unemployment (long term), which is approximately 5.0%–5.2%.

The large-scale gains in US employment over the past two years have not been mirrored by wage increases, as employees’ bargaining power has waned. Those who want to work full time but can only find part-time jobs may also be pulling down wage growth. In the year to end-April, wages rose a modest 2.2%. This is a far cry from the 3.0%–3.5% rate that some Fed officials see as normal for a healthy economy. Nonetheless, with full employment in view, that may soon change, while the BLS’s employment cost index showed that compensation costs for civilian workers rose at an annualized rate of 2.6% in the first quarter, up from 2.2% in the previous two quarters. The index showed that private-sector pay rose at an annualized rate of 2.8% for the March-end period, the quickest upward pace since 2008.

All in all, with the global outlook decidedly cloudy, the US outlook for the remainder of 2015 hinges importantly on how consumers respond to improving employment, including any signs that wages are moving higher, as well as savings produced by lower gasoline prices. In our estimation, therefore, any decision on rate normalization by the Fed in the months ahead will remain “data dependent” under the leadership of a highly pragmatic chair, Janet Yellen, although we also believe that recent job data are bringing that decision closer.

Multiple Central Banks Still in Easing Mode

As the United States contemplates a tightening of monetary policy in the months ahead, interest rates continue to be cut in other parts of the world—a sign that the global economy is not by any means on a smooth growth path yet. Indeed, the extent of the growth slowdown in certain large economies has surprised some economic forecasters, given the boost to global growth that should have stemmed from lower oil prices, and the aggressively easy policy stance in all the advanced economies.

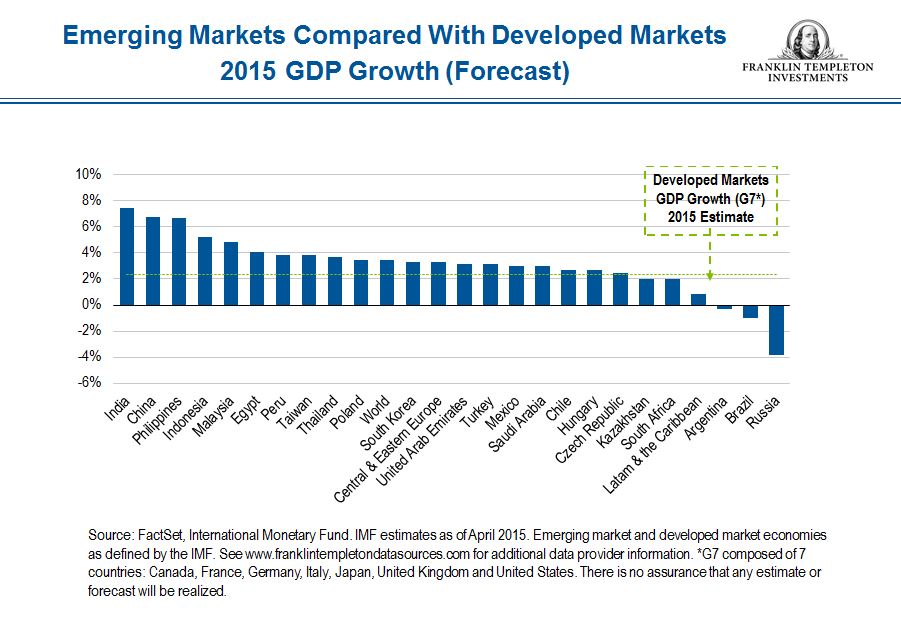

Thailand, Australia and China all relaxed policy rates within days of each other in late April and early May, joining a long line of rate cutters in recent months. Thailand cut rates at the end of April, just six weeks after a previous reduction, reflecting a weaker-than-expected recovery and a steady decline in inflation. Some of the weakness seen in Thailand—and other Southeast Asian countries—stems from the slowdown in the Chinese economy, which has hit trade data in countries such as South Korea and Taiwan. The overall trade between China and the rest of world dropped almost 11% in April from a year earlier, according to the General Administration of Customs, while inflation data for the same month showed Chinese inflation coming in at well below the People’s Bank of China’s (PBOC’s) target of around 3%. The drop in imports was particularly acute. With China reporting annualized growth of 7% in the first quarter—the lowest rate since 2009—such data suggest that there is a lack of any real momentum in the Chinese economy as we move into the second quarter. In response to the slowdown, on May 11 the PBOC cut both the benchmark one-year lending rate and the one-year benchmark deposit rate by 25 basis points—the third time policy has been eased in six months. The Reserve Bank of Australia has cut interest rates twice this year, with the second cut on May 5 bringing base rates down to 2%, their lowest level ever. Australia, like Thailand, has been feeling the effects of the Chinese slowdown, particularly in the demand for its commodities. Australia’s gross domestic product (GDP) growth came in at 2.5% in the final quarter of 2014, which is below long-term trends.

Overall, in Asia as in Europe, the dominant central banks are still in easing mode as they deal with an uncertain growth picture. The authorities in emerging markets will likely also soon have to deal with the end of cheap US money. Although liquidity from the European Central Bank (ECB) and the Bank of Japan will continue to seep into select markets, countries exposed to the US dollar could see bond yields—and hence debt service costs—rise as the Fed tightens policy. Countries with sizable private and public debt burdens denominated in US dollars can be expected to be the worst hit. Asian and Gulf countries with low debt levels and large currency reserves may be able to offset slower growth with lower taxes or increased spending. But this may not be the case everywhere, particularly in some Latin American countries, in spite of the recent respite they have been given thanks to a rise in commodity prices. And even in China, the PBOC warned in its latest monetary-policy report that the “rising debt size is forcing China to use a lot of resources in repaying and rolling over debt” while limiting the room for further fiscal expansion.

Europe Has Bond Market Hiccup

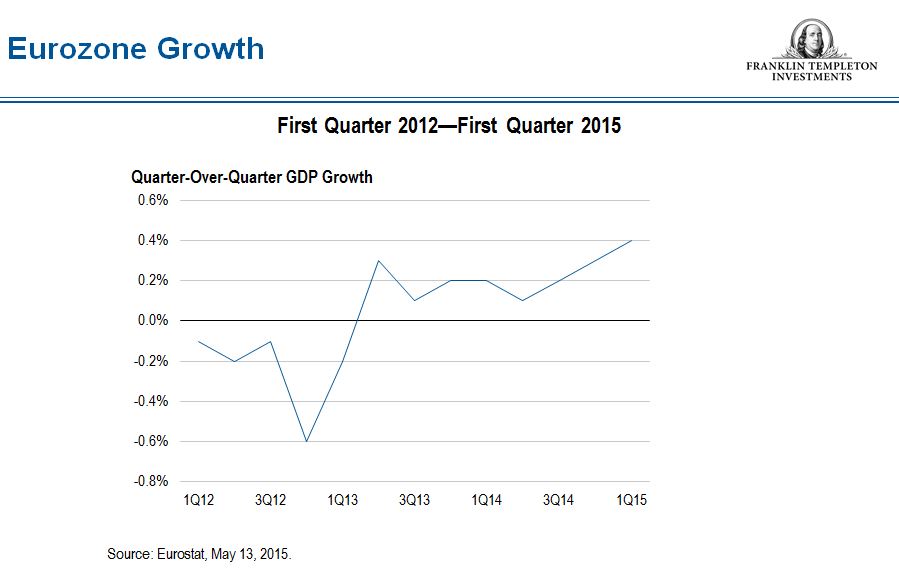

The European recovery appears to be well under way, with Eurostat announcing that quarter-over-quarter growth in the eurozone reached 0.4% in the first quarter, and the European Commission raising its growth forecast for the currency area this year from a previous estimate of 1.3% to 1.5%. The Commission credits low oil prices, the depreciation of the euro and loose monetary policy—including the ECB’s key refinancing rate of 0.05% and its €600 billion-per-month quantitative easing (QE) program—for this progressive improvement in the economy.

Yet, in recent weeks, the first two of these catalysts seemed to be going into reverse, with the euro beginning to rise against the US dollar and the price of Brent crude oil up over 50% from its January low point. There has been significant fallout on the region’s bond markets. European government bond yields, which had fallen to historic lows well before the ECB’s official launch of QE in March, rose again. The yield on German 10-year Bunds, which had fallen to as low as 0.05% in mid-April, were approaching 0.70% three weeks later. Spreads over Bunds for many other eurozone government bonds also rose.1 There is nothing necessarily sinister behind these sudden shifts: In the United States too, large declines in Treasury yields ahead of QE programs gave way to a rise in yields shortly after the Fed’s asset purchases actually started. It was far more unprecedented to see such a high portion of European bonds offer negative yields.

Some might argue more optimistically that the short-term rise in yields seen in late April and early May reflects Europe’s improved prospects, which, with the ECB’s help, have been pushing investors out of the perceived safety of government bonds—some of which have been offering negative yields—and into riskier assets. By contrast, the pessimists might see the short-term spike in European bond yields as heralding a period of heightened instability in markets as the United States heads toward monetary tightening and as negotiations between Greece and its creditors over bailout money reach a climax.

But the simplest explanation for the rise in bond yields would seem to us to be the impact of some investors exiting crowded positions, together with a rise in inflation expectations as oil prices have risen and growth has improved. Meanwhile, disappointing first-quarter data out of the United States have hit the US dollar and caused the euro to rise. But it may be too early to worry about a seismic sea change in the bond market that could eventually threaten Europe’s economic recovery. Already, the improved US jobs data for April served to curb some of the drop in European bond prices, while Europe, with an annualized inflation rate of zero in April (an improvement from -0.1% in March) remains far, far away from the ECB’s inflation target of below, but close to, 2%.

There remains the Greek problem. European finance ministers and negotiators for Greece continue to argue about the release of the final, much-needed €7.2 billion installment of Greece’s current €130 billion bailout. Both sides have taken a tough line: Greece’s partners say they will consider debt relief only after Athens commits to, and completes, the budgetary adjustments contained in its current bailout program, while the Greek government, led by the radical left Syriza party, has set down a series of “red lines” and is adamant it will not make further pension cuts or pass legislation to facilitate layoffs in the private sector. It could well be that the tough stance being taken by both sides is designed to assure their respective power bases—the Greek electorate in the case of Syriza and home country electorates in the case of European Union finance ministers. It is probably not in the interest of either side (at least in the short term) to see Greece tumble out of the eurozone. But accidents can happen—especially if decision makers in Brussels and Frankfurt begin to believe the rhetoric of an inexperienced government that has proven utterly incapable of fulfilling any of the promises that got it elected last January. Meanwhile, negotiations for another bailout program (the third) meant to aid Greece in honoring a heavy creditor repayment schedule over the coming months have not even begun.

One piece of good news for financial markets—at least in the short term—came with the unexpectedly clear victory of the Conservative Party in the British general election, with UK stocks and sterling both marching higher and Gilt yields falling. The Conservative victory may give hope to government parties that have similarly pushed through fiscal consolidation programs that have cost them support in opinion polls. But the possibility of a clash during the years ahead between a Conservative (and unionist) England and a Scotland dominated by secessionists is likely to be greeted less positively by market participants, as is a referendum on continued British membership in the European Union that the British prime minister, David Cameron, has promised by 2017. The race is on for mainland European leaders to come up with enough sweeteners to allow Cameron to present the case for a prolongation of Britain’s semi-detached relationship with the rest of the European Union.

The comments, opinions and analyses presented here are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in developing markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity.

1 A credit spread is the difference in yield between two bonds of similar maturity but different credit quality.

© Franklin Templeton Investments