IN THIS ISSUE

- US Economy Looking Up Ahead of Possible Fed Rate Hike

- World Bond Markets Become “Jittery”

- Europe Gradually Picks Itself Up

US Economy Looking Up Ahead of Possible Fed Rate Hike

After the US economy dipped into negative growth during 2015’s first quarter due to bad winter weather, a West Coast port strike, a surging US dollar and some anomalies in the way economic data are compiled, clear signs have emerged that it is firmly on a growth path, likely bringing closer the day when the US Federal Reserve (Fed) will start to “normalize” monetary policy.

The latest Fed Beige Book, which collates surveys of current economic conditions in each of the central bank’s regional districts, noted that overall economic activity expanded from early April to late May and that respondents were “generally optimistic” about the outlook. It also said that manufacturing activity had “held steady or increased” and that consumer spending was ticking up, with retailers “expecting continued sales growth in 2015.”

In contrast, the Organisation for Economic Co-operation and Development (OECD) decided in early June to lower its forecast for US economic growth to 2% this year—considerably down from a November forecast of 3.1%—and to 2.8% in 2016 (down from 3%). The previous OECD forecasts were made before the plunge in the first-quarter gross domestic product figure to -0.7%, which will inevitably drag down US growth for the year as a whole, but we think this should not disguise improvements in a number of areas, most notably in employment.

In May, job growth of 280,000, according to initial estimates, was much higher than consensus expectations, while data revisions put jobs created in April at over 220,000 and even the disappointing figure for March was revised upward. Meanwhile, the unemployment rate ticked up slightly to 5.5% from the previous month’s 5.4% reading (a seven-year low) as additional people entered the workforce. Encouragingly, there are signs that wages are reflecting the improved jobs picture, with average hourly earnings rising at a year-over-year rate of 2.3% in May. The workforce has grown increasingly confident about prospects, with a University of Michigan survey showing that consumers remained relatively optimistic about their future financial situation, with “86% of all households anticipating their financial situation would be the same or improve during the year ahead.”

Although auto sales in the United States have picked up some considerable momentum, the gains in employment and income have yet to filter into general consumer spending to the extent one might have expected. After having risen by a relatively disappointing 1.8% in the first quarter (down from 4.4% in the fourth quarter of 2014), consumer spending was flat in April, according to the Bureau of Economic Analysis, as US consumers have continued to increase their savings rate and pay down debts. But lackluster spending data may change: It is hard for us to believe the big increases in employment over the past year, together with rises in aggregate wages and the extra disposable income accumulated from the big drop in gas prices, will not translate into increased consumer spending.

We also expect improvements in the corporate sector. The significant scaling back of capital expenditure in the US energy sector in response to the drop in oil prices has had a meaningful impact on US growth statistics, but the large declines in oil prices—as well as the decline in investment—seem to be behind us. Hearteningly, US manufacturing has picked up of late, with the Institute for Supply Management’s (ISM’s) purchasing managers’ index (PMI) rising to 52.8 in May from 51.5 in April, climbing higher above the 50 mark that divides expansion from contraction. This improvement resulted from a decent increase in new orders, which canceled out some disappointing export data. Construction spending has also been picking up, rising at an annual rate of 2.2% in April to its highest level since November 2008.

One disappointing feature of the present upturn in the US economy (and seen throughout the developed world at the present time) is productivity, which has been trending lower for a number of years. Worker productivity actually fell in the first quarter, according to the Bureau of Labor Statistics. Low or declining productivity could constrain wage growth as well as corporate earnings. Anemic productivity growth may eventually mean that recent strong jobs growth does not prove sustainable.

On the whole, however, steady improvement in the labor market and in the US economy overall should, we believe, push the Fed to raise US base rates in the months ahead. Some Fed policymakers have been conveying the impression that uncertainties about growth momentum in the United States mean that rate rises will be shallow and gradual, especially as inflation is not yet a concern. Indeed, the core personal consumption expenditure (PCE) index stood at an annual rate of just 1.2% in April, still well short of the Fed’s 2% target. But the Fed is fully aware that it will take time for PCE to rise to that level and that, for the moment, it is the upward trajectory of prices that counts. In addition, with the core consumer price index up a more robust 1.8% in April and with wages increasing, it is possible that further fundamental improvements in the US economy will force the Fed to become somewhat more hawkish.

World Bond Markets Become “Jittery”

Even as the global economy, in the words of the OECD, “muddles through”—at the beginning of June, the OECD lowered its global growth forecast for this year to 3.1% from its forecast of 3.6% six months before—it looks like it will have to face a bout of increased volatility in bond markets. Much attention is currently focused on the emerging-market universe. Bond issuance, including corporate bond issuance, has grown exponentially in Southeast Asia in the past 10 years, and homegrown institutions such as pension funds and insurers have emerged alongside foreigners as investors. But economic growth has faltered in many countries just as US rate hikes look to be in the offing, reducing these countries’ attractiveness to foreign investors. As a consequence, the Institute of International Finance (IIF) believes that capital inflows to emerging markets will decline this year. Yet, beyond short-term volatility, we are not sure there will necessarily be a replay of the Tequila Crisis in Mexico in 1994–1995 or the Asian Financial Crisis of 1997–1998, when countries found themselves unarmed against massive withdrawals of capital. Since then, many emerging markets have made remarkable progress in reducing inflation, improving government debt ratios, building huge foreign reserves and tightening bank regulation. The development of local-currency debt markets has also made them less vulnerable to exchange-rate gyrations. True, there remain countries with a heavy reliance on external finance and commodity exports that could suffer from a Fed move toward monetary policy normalization, but we think rate rises in the United States have been well signaled, meaning that policymakers and investors should not be taken off guard when they come.

Thus, if Fed rate increases are as small and gradual as many observers believe they will be, any negative fallout could prove temporary and largely restricted to the most vulnerable emerging markets—namely those with weak policy frameworks or with macroeconomic vulnerabilities such as large or poorly funded current account deficits. Some Latin American countries, as well as places like Turkey and South Africa, look particularly exposed in this regard. But we believe that the chances of contagion across the emerging-market asset class based on the difficulties of one or more countries is not certain and that investors will likely learn to differentiate between countries with varying degrees of financial robustness. At the same time, we recognize that emerging markets in general are likely to be “jittery” (in the words of the IIF) as US interest-rate hikes are implemented, at least in the short term. Nerves could be even more frayed if the Fed does not follow the “small and gradual” path currently being predicted. In addition, attention will need to be paid to China, where the doubling in value of stock indexes over the past year reflects a massive build-up of credit.

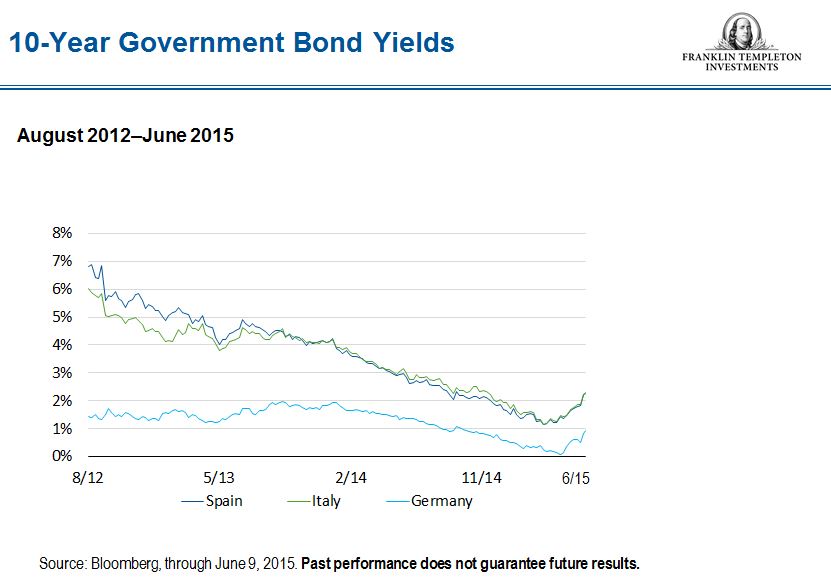

Indeed, the general rise in global asset prices since 2009 has been built on easy money provided by many of the world’s major central banks. Thus, bond markets—and not just those in emerging markets—have become jittery of late, with world bond indexes producing negative returns in May. Yields on 10-year US Treasuries rose close to 2.4% after the release of May nonfarm payroll figures in early June, compared with under 1.9% at the beginning of May and 1.6% in January. After several years of pretty consistent drops in bond yields, these recent rises are still modest and are consistent with a pickup in US growth. Treasury yields are still only where they were at the end of last September. The same is true for benchmark yields in European countries such as Italy. It is therefore not yet clear (although clarity could develop in the coming weeks) that we are at a tipping point from which we will see bond yields march dramatically higher. Instead, it seems more appropriate to argue that we are experiencing a healthy correction to some extreme positioning, including the appearance of negative yields in Europe. As inflation expectations and growth pick up throughout the developed world, negative yields are hard to justify. Thus, it appears market fundamentals have begun to reassert themselves in the face of distortions caused by ultra-easy monetary policy. At the same time, with US and European growth rates expected to remain relatively modest, and with the Fed very transparent about its policy intentions, we would not expect a dramatic hike in base yields. However, we also recognize that some market participants could be caught out if the Fed uses good economic data to hike rates more than futures markets are predicting.

Europe Gradually Picks Itself Up

In spite of lingering concerns about Greece’s fate, the European economy would appear to have hit a sweet spot marked by steadily improving growth and inflation figures, along with declining unemployment. A weak euro, low oil prices and expansionary monetary policy all have had a role to play in this improvement. However, it is probably too soon to be euphoric about Europe’s prospects. Official figures from Eurostat show that the fall in the eurozone unemployment rate has been painfully slow—declining to 11.1% in April from 11.7% a year earlier—and remains much higher in countries like Greece and Spain. In addition, Markit’s composite PMI reading for May, while remaining above the 50 mark, slipped a little. Moreover, European Central Bank (ECB) President Mario Draghi admitted at the beginning of June that while the region’s recovery was “on track,” the ECB had “expected stronger figures.” Nevertheless, the ECB expects the eurozone’s recovery to “broaden” in the months ahead, as private-sector lending growth picks up and inflation expectations move higher.

How long will this sweet spot last? The region’s aging workforce and a concomitant drop in productivity gains indicate that potential growth in the eurozone is falling. Current conditions may mean that the eurozone breaks out of trend growth for a while, but the outlook further out is less upbeat. Reforms in Italy and France have yet to dispel concerns about the competitiveness of either nation in the absence of the kind of ECB-induced euro weakness we have seen since last year, and even in Germany there has been a sharp structural deterioration over the past five years as real wages have grown faster than productivity.

At the time of this writing, Greece and its European partners still had not struck some sort of deal to release €7.2 billion in much-needed bailout aid and thus avoid a payment default in the coming weeks. But Greece’s position remains precarious, and the possibility of the country’s exit from the eurozone cannot be fully dismissed, especially as the Greek government continues to engage in grandstanding (presumably for domestic consumption).

Greece was already close to the brink in 2011, when fears that a financial collapse in the country would lead to the demise of the eurozone, thus helping ensure that copious amounts of money were found to shore up Athens (although with plenty of strings attached). Four years on, the situation has changed, with support for the eurozone edifice much improved. In our assessment, quantitative easing (QE) means the ECB now has a robust firewall against any potential Greek contagion. While bond markets have turned more volatile since mid-April, yields have remained low in all eurozone countries except for Greece, pointing to this lack of contagion. The instruments at the ECB’s disposal explain why there cannot be a blank check for the Greeks this time around, whatever their difficulties. As a result, the Greek government, dominated by radical left-wingers, has much less bargaining power. It may soon have to explain to the Greek population how, in exchange for bailout money, it has had to accept labor and pension reforms that it has fought against since early this year. The political fallout in Greece could be significant, in our view.

Certainly, the situation in Greece may help explain the rise in volatility in eurozone bond markets in recent weeks. For example, some believe that the imminence of a debt deal between Greece and its creditors has encouraged investors to abandon perceived safe-haven bonds. Other forces that are entirely decoupled from Greece are probably at work too. For example, the upturn in European growth could be encouraging investors to abandon low-yielding government bonds in favor of higher-risk, potentially higher-return assets. In addition, concerns over bond market liquidity seem to have convinced investors to abandon crowded positions built up since the end of last year, when QE was first mooted. With a lack of liquidity already an issue, a downturn in trading volume over the summer months could contribute to further volatility. Yet European bond yields currently remain lower than they were in October 2014, and there seems little danger they will spiral so high that they threaten Europe’s recovery any time soon. ECB President Draghi has appeared quite relaxed about the recent spike in yields, arguing that higher volatility is to be expected during periods of ultra-low interest rates. Nonetheless, as Draghi’s remarks imply, the unleashing of massive new money into bond markets via QE is causing distortions, with some bond prices increasingly disengaged from economic fundamentals. Concerns about the divorce between bond prices and economic reality no doubt help explain the gyrations in European bond yields.

The comments, opinions and analyses presented here are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in developing markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity.

© Franklin Templeton Investments

© Franklin Templeton Investments