Unconstrained Global Investing in an Extraordinary Monetary Policy Enviornment

Monetary policy divergences have given global investors much to think about—and debate about— this year. Speaking at Franklin Templeton’s 2015 Global Investment Forum in New York last month, Michael Hasenstab, chief investment officer of Templeton Global Macro, offered plenty of food for thought on the subject. He believes the markets are at a critical juncture, and said it’s time to reevaluate one’s fixed income portfolios as traditional drivers of return may no longer be able to provide. He shared his team’s approach to navigating what could be the end of an era of historically low US interest rates, while other parts of the world continue fueling liquidity with easy monetary policies.

I think we are at a critical juncture in global markets today. Investors have been on a sort of high for the past few years, where bonds and stocks alike were defying gravity. I think now is the time to reevaluate one’s fixed income portfolio and think very differently about how it’s going to perform going forward, and how it’s going to perform relative to other asset classes. In our strategies, we’ve tried to design something that’s different, that’s diversified, and that doesn’t track traditional asset classes. In our assessment, the global macroeconomic backdrop looks broadly positive right now, but not all markets look the same—or face the same challenges.

United States

The US economic recovery looks robust, but there has been a recent period of volatility in gross domestic product (GDP) growth. While investment spending has been weak in the first half of the year, reflecting a decline in oil-related spending, we would anticipate a pickup in the second half of the year. Furthermore, as oil prices look to remain low at least in the short term, households are increasingly likely to spend additional income. A collapse in oil prices led to a collapse in energy production, which was a big contributor to weak first-quarter growth. In our view, what happened in the first quarter was a unique period that’s unlikely to set the trend for the coming years. US shale producers saw their world turn upside down temporarily, but the majority of the US economy is a massive consumer of oil, and these lower oil prices are going to be a very positive tailwind to US growth in those industries such as chemical, pulp and paper, and others dependent on energy, which essentially saw their costs cut in half. Additionally, the US consumer is benefiting from a functional tax cut as a result of lower oil prices. While it doesn’t appear consumers have initially spent this extra wealth, I think we will start to see that spending come through the economy over time. So, overall lower oil prices are providing a nice tailwind for the United States at a time labor markets are improving.

The Federal Reserve (Fed) has been talking down the improvement in the labor market and talking down any fears about inflation, so there’s an idea the labor market isn’t healthy. However, when we look at the data, we see a labor market that is near pre-financial crisis levels.

It’s true that wages have not generally gone up, but that’s only one part of the picture. The number of people and the hours that they are working have massively increased, and so too, the spending power in the US economy has grown significantly. As we see it, it is only a matter of time before US wages start to rise to levels where inflation is triggered. Using the Fed’s own estimates, we are quite close to what’s considered to be full employment. To us, this does not justify 0% interest rates. Interest rates at zero may make sense when unemployment is close to 10%, but not when close to full employment. With the Fed still deploying monetary policy that’s appropriate in a crisis, we think we are entering a dangerous zone and this behavior that suppressed interest rates is no longer consistent with the macro data we are observing.

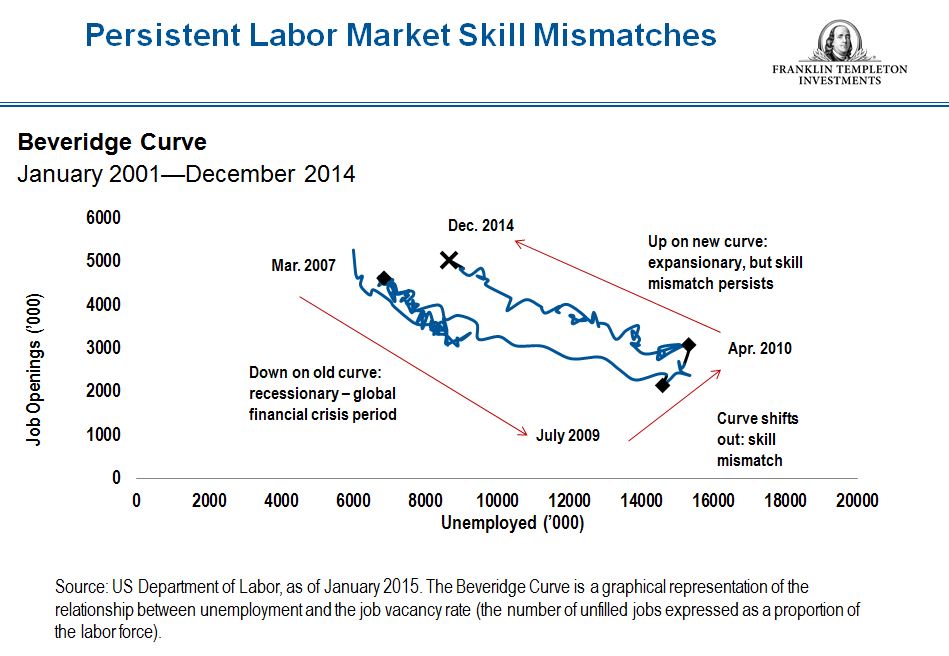

There’s been some talk about the low labor force participation rate; the thinking is that there is a huge pool of labor that is disengaged and is going to reengage into the job market, which will prevent wage growth. I think what has happened during the last recession is fairly unique in that we have a structural loss of employment; there are a lot of people who have left the labor force who will never come back. Some may have been older, or took disability; they basically permanently exited from the labor force and don’t have the skills to reengage in the jobs that are needed. One way of looking at this dynamic is the Beveridge curve, which examines the number of job openings relative to the number of unemployed. We now have the same level of job openings that we had pre-crisis, yet the unemployment rate is still a little bit elevated. That tells us that despite having all these job openings and this pool of labor, they just don’t have the skills required. I think this structural shift is throwing some people for a loop, but I think it means we are much closer to an inflationary level of unemployment than the unemployed numbers will tell you.

Eurozone

Turning to the eurozone and the issue of Greece, I reiterate what I’ve said before, that one of three things will happen: Greece will leave the eurozone, Greece will default, or Greece will be a permanent subsidy of Germany. I think it’s looking like the eurozone exit probably makes the most sense as Greece is in a debt trap there’s almost nothing it can do to get out of. If Greece defaults on its debt but doesn’t leave the eurozone, that’s a big moral hazard. Other countries like Italy may think to do the same—write off their debt. I don’t think that would happen, but it’s a risk. In my mind, Greece’s exit from the eurozone seems the highest probability, and I actually think it could be a positive thing. The eurozone is ring-fenced with ample liquidity, so a tumultuous event in Greece isn’t likely to create much of a ripple.

However, the most important dynamic that’s happening in the eurozone is the European Central Bank’s (ECB’s) quantitative easing (QE) program, not so much in leading an economic expansion by putting liquidity in the banking system (which is happening naturally), but in the weakening of the euro. A weaker euro is important because Germany drives half of European growth, and Germany’s economy is export-oriented. In our view, the weakening euro appears to be the strongest policy tool to re-engineer growth; if you look at the relationship between exports and the euro exchange rate, you can see the further the euro depreciates, the greater the rate of export growth. This gives the eurozone a nice tailwind. The ECB, I think, has been very explicit that it is going to continue on this path of money printing for some time. This will likely continue to further pressure the euro, especially as the US Fed starts to normalize interest rates. That said, our confidence in Europe is more short term in nature due to these tailwinds. In the medium to longer term, there are still some huge structural imbalances in parts of the eurozone, including a lack of full labor flexibility, a lack of fiscal consolidation and coordination, and lack of political coordination. Europe is going to face these challenges, but I don’t think it’s going to be the big story for some time.

In terms of our portfolio positioning, one way we can play this is by shorting the euro, but also looking at which countries will likely benefit from a boost in exports. Countries such as Hungary, the Czech Republic or Poland can benefit from a boost in German exports because much industry in Germany has moved into those countries, which boast high levels of skills, low labor costs and low taxes. We’ve been bullish on Central Europe for some time and believe this extra tailwind should further propel these economies into achieving higher growth rates. That’s one of the themes we’ve been playing in our portfolios.

Japan

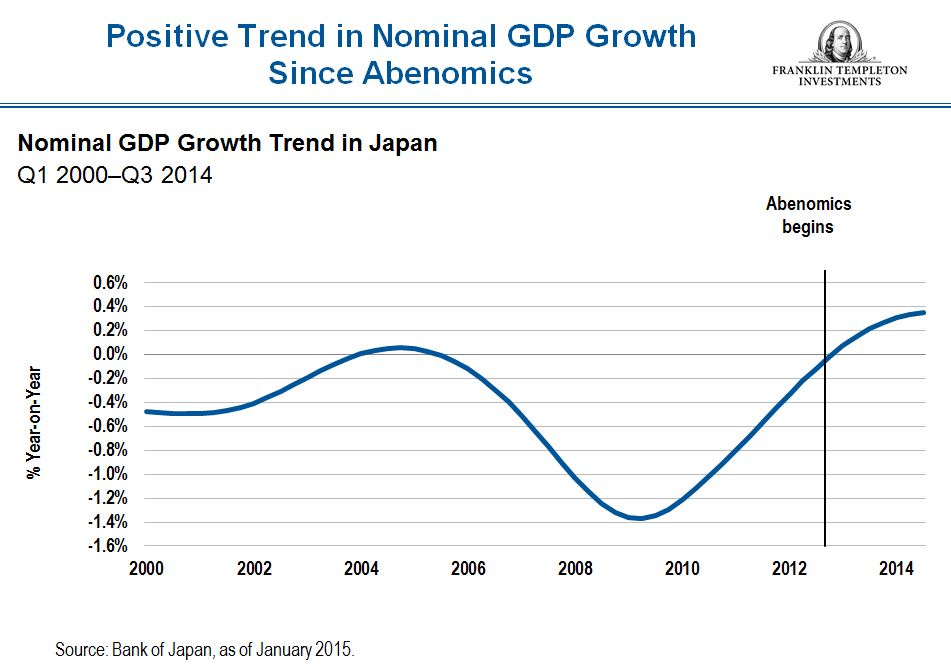

For the first time in decades, Japan seems to have broken a period of deflation, and we actually have started to see growth. Japan has made the first steps toward a recovery that has been 30 years in the making, and I think a lot of the credit goes to Prime Minister Abe for engineering an appropriate sequencing to try to tackle needed long-term reforms. If he had tried to do all the tough immigration reforms, labor reforms and corporate tax reforms at the same time as attempting to engineer inflation, he probably would’ve been unpopular. He engineered it with a different sequencing, starting with a QE program that had two meaningful impacts. He massively lowered real interest rates, which boosted asset prices (equity and real estate markets). That brought him incredible popularity and now gives him the opportunity to try to engineer structural reforms. I also think that it’s important to understand the critical role of QE in his whole political legitimacy, because in order to boost the equity market, he needs pension funds to buy equities. When the pension funds aren’t buying bonds and foreign investors aren’t interested in buying Japanese bonds at 0% yield, the only buyer left is the Bank of Japan (BOJ). The only way to get the Ministry of Finance on the same side with the prime minister is to ensure that Japanese bonds are financed; thus, they are being financed through debt monetization. The BOJ is fully funding the government’s deficit, so QE in Japan is a much different beast than in Europe and the United States, where it was about liquidity injections and currency manipulation. In Japan’s case, it’s pure and simple debt monetization as a way to boost asset prices, to gain political legitimacy. I think QE will likely continue in Japan, and the yen should continue to depreciate as a result.

China

I think China is a fascinating story because of its complexity. I was just in China a few weeks ago and had some interesting conversations with academics trying to disentangle how the duality of China’s economy is unfolding. Parts of the economy are in recession; some local governments are kind of replicating what the US muni market went through during the global financial crisis in 2007–2009, and there are certain other sectors, in manufacturing and in commodity-related areas, that have overcapacity issues. That would typically lead to a rise in unemployment, a cyclical downturn and a collapse in growth; but that’s not happening. In fact, the labor market is tightening in China, and its GDP growth is stable around 6.5%–7%. The reason is that China is experiencing a long-term demographic change. Around the year 2000, the working-age population declined for the first time, and there were increasing labor shortages because of the single-child policy that was put in decades ago. Chinese wages hadn’t increased for decades but subsequently, around 2003 or 2004, wages started to increase significantly.

As wages started to increase significantly, consumption as a percent of GDP started increasing. So while some parts of the economy may be in recession, China has a labor market demographic that is driving consumption and boosting the other half of the economy. However, if you look at the official statistics, they will show consumption continues to decline, but the problem with the official statistics is that they ask individuals how much they earn and rely on that reporting. However, if an individual earns all their money in the gray market (via distribution channels which are legal but may be unofficial, unauthorized, or otherwise not originally intended) and doesn’t want to pay taxes, they are going to understate it. So, some academics went out and observed what people were actually doing with their money, for example, spending it on consumer goods. So, with wage growth we see consumption, the consumer sector, significantly increasing as a share of GDP. If there is 4% or more GDP growth from consumption, then not as much investment is needed. Anyone who has traveled to China has witnessed the need for massive environmental investment and a need for improving transport, as well as more low-income housing in the cities as they continue to urbanize. There is some good investment that can come about, but it’s not the shopping malls and soccer stadiums that China built in the 2009–2011 period.

The challenge in China is that the whole economy is not in sync; you have two very opposite directions, and the balance is precarious. I think earlier in the year, the balance of the downdraft was overpowering the updraft, and the central bank reacted pretty aggressively by easing policy. I think China’s central bank has the tools, the fiscal wherewithal, the monetary levers, to achieve its targeted growth rates this year and next. The bigger question then becomes one of timing: Can it cushion the economy for a couple of years while the recessionary parts work through the system and recover? That remains to be seen.

In summary, we have reasonable global growth today. The United States is growing above trend and Europe, I think, is likely going to surprise to the upside. And, China’s not going to collapse. This backdrop is important for emerging markets because a lot of emerging markets basically sell into these countries, and especially the export-oriented economies like South Korea and Mexico are leveraged to global growth. Our conviction in select emerging markets is partially motivated by what’s going on in individual countries, but also motivated by a decent macro backdrop.

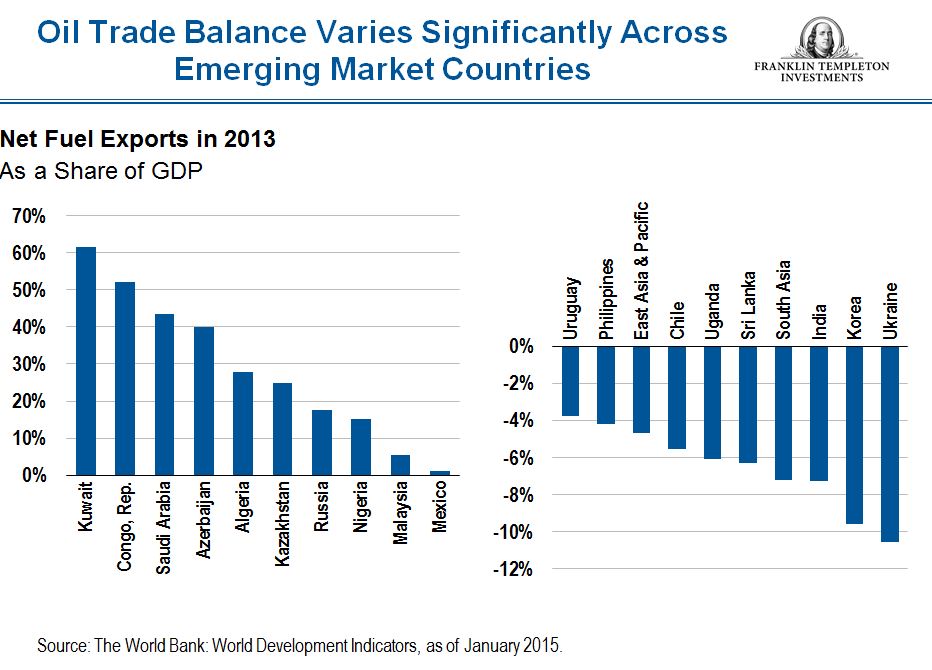

There has been a misperception in the emerging market space that these countries are an oil play and so you should short emerging markets because they are all oil-dependent. But, the reality is it’s quite varied. There is a pool of countries that are huge oil importers, such as China, India and South Korea. And, in the case of Mexico, less than 10% of its exports come from the energy sector. Mexico is really more tied to the US consumer and the US growth cycle, so shorting Mexico as a result of oil, I think, will likely backfire. I also think Mexico has one of the cheapest currencies out there and it is a market we favor. I believe this is an example of how we need to think differently about where we invest today. It is about capturing value outside the mainstream.

For a more detailed analysis of Hasenstab’s views on growth in the United States, Japan, the eurozone, China and other emerging markets, read his team’s quarterly “Global Macro Shifts” paper and view related video content.

Michael Hasenstab’s comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including possible loss of principal. Currency rates may fluctuate significantly over short periods of time, and can reduce returns. Derivatives, including currency management strategies, involve costs and can create economic leverage in a portfolio which may result in significant volatility and cause the fund to participate in losses (as well as enable gains) on an amount that exceeds the fund’s initial investment. Foreign securities involve special risks, including currency fluctuations and economic and political uncertainties. Investments in emerging markets involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size and lesser liquidity. Changes in interest rates will affect the value of a bond portfolio and its share price and yield. Bond prices generally move in the opposite direction of interest rates. As the prices of bonds in a portfolio adjust to a rise in interest rates, the portfolio’s value may decline.

© Franklin Templeton Investments

© Franklin Templeton Investments