The Upside to Low Liquidity Bond Markets

By the Multisector Full Discretion Team

Portfolio Managers Dan Fuss, Matthew Eagan, Elaine Stokes & Brian Kennedy; Product Managers Kenneth Johnson & Fred Sweeney

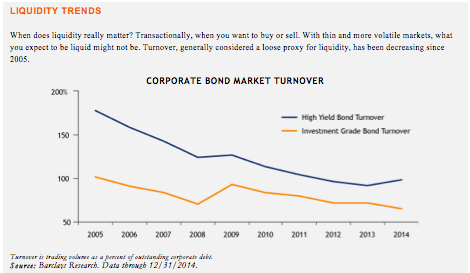

Bond market liquidity continues to slide. Structural market changes, including new regulations, have weakened liquidity. Additionally, we believe the credit cycle is approaching a stage when liquidity is normally low. We expect these converging trends to create a lower-liquidity environment that will be punctuated by market dislocations. While unnerving to many, discerning opportunistic investors can use this environment to purchase fundamentally strong credits trading at significant discounts.

Understanding Bond Market Liquidity

In trading, liquidity is the ability to easily purchase or sell a security at a reasonable price in a reasonable amount of time. However, liquidity is notoriously illusive; normally functioning markets can suddenly become significantly less liquid due to unforeseen catalysts. An investor exodus, for example, pushes prices down because the number of sellers exceeds the number of buyers. As this occurs, buyers willing to step in provide liquidity in exchange for the higher yields that result from lower prices. However, falling prices stoke risk aversion, driving up the number of sellers and snuffing out bid-side appetite. Under these conditions, the vicious cycle of falling prices, higher volatility and evaporating liquidity accelerates.

Structural Changes in Liquidity

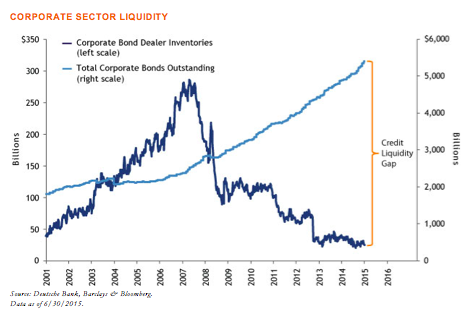

Sharply lower dealer inventories and rising levels of outstanding corporate debt have created a significant liquidity gap in credit markets, as illustrated in the chart on the next page. Regulatory changes enacted in the wake of the global financial crisis sparked several structural changes. Specifically, banks have reduced risks associated with their proprietary trading desks. Historically, proprietary trading desks worked two ways: agency trading, when a bank matched buyers and sellers, and principal trading, when the bank itself took the other side of the trade (a source of secondary market liquidity precrisis). Due to the Volcker rule passed as part of the Dodd-Frank financial reform act and Basel III reforms from the Bank for International Settlements, principal trading is more onerous and less profitable, so banks primarily engage in agency trading. As a result, banks are less willing to bridge temporary supply and demand imbalances, giving rise to larger price and liquidity swings.

Regulatory changes, while significant, have not been the only structural changes. The bond market has grown since the crisis, and its buyer base has evolved. Corporate bond issuance has doubled since December 2007, fueled by low interest rates, central bank quantitative easing and high demand. Additionally, large institutional buyers, such as insurance companies, sovereign wealth funds and liability-driven investors, purchase new issues and hold them until maturity, functionally draining market liquidity. Since secondary supply is scarce, yield-starved investors have flocked to the primary market, often oversubscribing new issues. With bond investors tending to crowd the same sectors and issues, markets trend up strongly with decent liquidity yet are prone to rapid, sharp corrections. In our view, these structural changes magnify selloffs and prolong the return to normal market conditions.

Looking Beyond Liquidity

Deteriorating liquidity can push security prices well above or below fair value. However, short-term price movements may be difficult to interpret without a broader view of the credit markets. Our assessment of the credit cycle, with inputs such as corporate health, leverage, profits, economic growth, inflation and investor risk appetite, informs our three- to five-year credit view. When markets begin to trade away from our long-term view, we draw on our deep research to identify value-oriented opportunities. We believe a key ingredient of our long-term alpha generation is capturing value when prevailing market conditions cause deviations from our fundamental view.

We believe the US credit cycle is in the expansion to late-cycle phase when bonds become more fully valued, although the yield in specific sectors remains attractive. If history holds, this phase could persist for at least one to two more years, with credit metrics stable and defaults low. Eventually, the cycle will progress into a downturn, characterized by low liquidity, widening spreads, falling prices, rising yields and investor flight. Leading up to this transition, we believe we will see increased instances of market dislocation, as occurred recently in the energy sector.

Given our expansion-to-late-cycle assessment, we are comfortable holding higher-than-average reserves, such as cash and high-quality developed market sovereign debt. This gives us room to potentially capitalize on market disruptions without having to sell existing holdings into the same weakness. Since we expect higher US rates or volatility to present buying opportunities, we intend to patiently use reserves to invest in our best ideas. This is a basic tenet of our investment approach; we take a long-term view, carefully research opportunities and step in to buy what we consider attractive securities that seem to have fallen out of favor.

Our Strategy in Action

Two recent applications of this strategy involved the energy sector and Irish sovereign debt. These examples represent how we applied this strategy to two specific market events. While we endeavor to apply our strategy consistently, different market conditions could result in different outcomes.1

Energy, 2014-2015

Oil prices fell by nearly 50% from the end of June 2014 through March 2015 primarily due to weak demand and oversupply, reaching price levels not seen since 2009. As a result, high yield energy sector spreads widened significantly, an indicator of reduced liquidity and increased investor risk aversion.

Though some companies experienced a breakdown in credit fundamentals resulting in capital losses to bondholders, we believed a portion of the spread widening reflected technical selling pressure. As oil prices continued to decline in the third and fourth quarters of 2014, we began to buy what we viewed as long-term, value-oriented energy investments. We focused primarily on US exploration and production firms with strong balance sheets and assets that we believed could weather an extended period of low energy prices. From March through June of 2015, energy prices rebounded meaningfully, bolstering high yield energy prices, and liquidity returned to the sector. However, global macroeconomic and geopolitical events are still playing out. We believe supply and demand will eventually rebalance on US production cuts, resulting in higher prices.

Irish Debt, 2007-2013

Ireland’s financial crisis began in 2007 and accelerated over the next several years, precipitating a recession and a move into the downturn phase of the credit cycle. Ultimately, the banking system became insolvent, and the country faced default. Beginning in November 2010, the European Union (EU) and International Monetary Fund (IMF) provided critical aid, which allowed the Irish government to meet its funding obligations. The government also undertook unprecedented austerity measures to repair the fiscal damage. On July 26, 2012, coincident with Mario Draghi’s “whatever it takes” speech, Ireland returned to the bond markets with its first auction since seeking international aid. Irish government debt rallied significantly in the second half of 2012 and into 2013.

We began building positions in Irish sovereign debt during the fall of 2010, amid the European crisis and prior to Ireland’s formal aid requests. We continued buying bonds through the summer of 2011, as Irish debt prices bottomed following the sovereign’s credit downgrade to junk by Moody’s. Over this period, trading volumes and sizes decreased significantly, reflecting economic stress and compromised liquidity. As investors fled the market, the average quarterly trading volume for an exchange-listed 2018 sovereign bond fell by 91% to €303 million for the first half of 2011, down from an average quarterly volume of €3.4 billion for 2010.2

Unlike the market, we believed overall fundamentals for Irish sovereign debt remained strong, supported by the dynamic, open Irish economy, a highly skilled workforce, relatively favorable demographics and an attractive corporate tax structure. We also expected a favorable outcome for Irish sovereign debt holders. In 2013, we exited our Irish debt position at a significant gain since prices reflected our fundamental view.

A Perennially Opportunistic Stance

Bond markets will continue to adjust to the new liquidity environment, and the credit cycle will eventually progress. We believe we are well positioned to add value through this possibly prolonged late-cycle period and into the next downturn. Leveraging our proprietary insight and long-term view, we seek to exploit liquidity as selective, opportunistic buyers when sellers predominate. Our approach intends to add value over three- to five-year credit cycles through a disciplined investment process, deep fundamental research and good security selection. We believe our long-term, value-oriented approach will help enable us to uncover considerable opportunities offered by these evolving markets.

About Risk

Because the Fund can invest a significant percentage of assets in foreign securities, the value of the Fund shares can be adversely affected by changes in currency exchange rates, political, and economic developments, which can be significant in emerging markets. The Fund is subject to currency risk, the risk that fluctuations in exchange rates between the US dollar and foreign currencies, which may cause the value of a Fund’s investments to decline. Funds that invest in securities denominated in, or receive revenues in, foreign currency are subject to currency risk. Because the Fund can invest a significant percentage of assets in debt securities that are rated below investment grade the value of Fund shares can be adversely affected by changes in economic conditions or other circumstances. These events could reduce or eliminate the capacity of issuers of these securities to make principal and interest payments. Lower-rated debt securities have speculative characteristics because of the credit risk of their issuers and may be subject to greater price volatility than higher-rated investments. The secondary market for these securities may lack liquidity which may adversely affect the value of these securities and that of the Fund. The purchase of Fund shares should be viewed as a long-term investment. Mutual funds that invest in bonds can lose their value as interest rates rise and an investor can lose principal.

Disclosure

Barclays US Aggregate Bond Index is an unmanaged index of investment grade bonds with one- to ten-year maturities issued by the US government, its agencies and US corporations. Indexes are unmanaged and do not incur fess. It is not possible to invest directly in an index.

This paper is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. Investment recommendations may be inconsistent with these opinions. There can be no assurance that developments will transpire as forecasted and actual results will be different. Data and analysis does not represent the actual or expected future performance of any investment product. We believe the information, including that obtained from outside sources, to be correct, but we cannot guarantee its accuracy. The information is subject to change at any time without notice.

The views and opinions expressed may change based on market and other conditions. There can be no assurance that developments will transpire as forecasted. Past market experience is no guarantee of future results.

Before investing, consider the fund’s investment objectives, risks, charges, and expenses. Please visit www.loomissayles.com or call 800-633-3330 for a prospectus and a summary prospectus, if available, containing this and other information. Read it carefully.

NGAM Distribution, L.P. (fund distributor) and Loomis, Sayles & Company, L.P. are affiliated.

LS Loomis | Sayles is a trademark of Loomis, Sayles & Company, L.P. registered in the US Patent and Trademark Office.

MALR013549 1237610.1.2

1 These examples represent past performance, which is not a guarantee of future results, and may be different for other time periods or fund holdings.

2 Irish Stock Exchange, data for an Irish government bond with a 4.5% coupon maturing in 2018, as of 6/30/2015. Most bonds trade over the counter; however, some are listed on exchanges, where trading volume data are more readily available.