5 Reasons August May Take Investors for a Ride

Allianz Global Investors

By Kristina Hooper

August 3, 2015

It’s hard to believe it’s August already. 2015 is really flying by. Many American families are gearing up for summer vacations, which is probably why August is known as American Adventures Month. But this year, US investors may be in for a bumpier ride. In the coming weeks, we expect US stocks and bonds to experience significantly higher volatility. Here’s why:

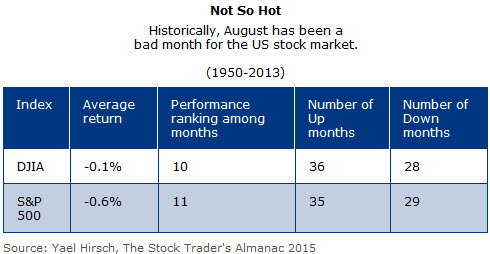

1. History. According to the 2015 Stock Trader’s Almanac, August has been the worst month for the Dow Jones Industrial Average, the S&P 500 Index and the Nasdaq Composite Index since 1987.

2. September FOMC Meeting. The normalization of US monetary policy is a historic, dramatic event, which could have far-reaching effects. Investors will likely become jittery as the September FOMC meeting approaches, given that the Federal Reserve could raise interest rates for the first time since 2006.

3. Data dependency. The Fed’s decision to raise rates will be data-dependent. Data scheduled for release in August will be some of the last metrics available to the Fed in its attempt to gauge the state of the economy. It may take on even more importance given that recent data has been mixed. For example, one of the takeaways from the second-quarter GDP report is that consumer spending is slowly recovering. However, this is a backward-looking metric. Looking ahead, we might see a temporary drop in consumer spending given that consumer sentiment data for July shows a significantly less optimistic outlook for jobs and spending.

Also, the Employment Cost Index, which came out last Thursday, was a negative surprise. It showed 0.2% wage growth—the lowest reading in its 33-year history. Historically, the ECI has indicated higher compensation growth than average hourly earnings, which is another measure of wage growth. The Fed will be keenly focused on wage growth given its impact on inflation. That means average hourly earnings in this Friday’s jobs report will take on even more significance. It’s important to stress that we could see an outsized reaction to data released in the coming weeks, given how significantly they might influence the FOMC’s decision.

4. Puerto Rico. The US territory has officially defaulted on its August 1 debt payment—and this debt crisis shows no signs of being resolved. Puerto Rico’s debt is widely held because its triple tax-exempt status is an attractive feature. And trouble in Puerto Rico could impact other stressed municipalities in the United States. Don’t underestimate Puerto Rico’s ability to rattle investors and the municipal bond market.

5. International developments. There could be another eruption in Greece’s debt negotiations—particularly given recent concerns expressed by the International Monetary Fund—or additional turmoil in China’s stock market. Further, we could see a negative reaction to Japan’s second-quarter GDP report when it’s released in mid-August, which is expected to show a contraction.

The bottom line: It’s important to stress that fundamentals are largely solid for the US economy, which is why we have a more favorable outlook on the stock market in the longer term. But, in the short run, we think there is the potential for higher volatility with a downward bias. Depending on your time horizon, an August downturn could present a buying opportunity.

Kristina Hooper is the US investment strategist and head of US Capital Markets Research & Strategy for Allianz Global Investors. She has a B.A. from Wellesley College, a J.D. from Pace Law, a master's degree in labor economics from Cornell University and an M.B.A. in finance from NYU, where she was a teaching fellow in macroeconomics.

Subscribe Today

The Upshot is available as a subscription for financial professionals only. New issues will be delivered via email every Monday. Visit us.allianzgi.com/theupshot to learn more.

The material contains the current opinions of the author, which are subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities. Forecasts and estimates have certain inherent limitations, and are not intended to be relied upon as advice or interpreted as a recommendation.

Past performance of the markets is no guarantee of future results. This is not an offer or solicitation for the purchase or sale of any financial instrument. It is presented only to provide information on investment strategies and opportunities.

A Word About Risk: Equities have tended to be volatile, involve risk to principal and, unlike bonds, do not offer a fixed rate of return. Foreign markets may be more volatile, less liquid, less transparent and subject to less oversight, and values may fluctuate with currency exchange rates; these risks may be greater in emerging markets.

There is no guarantee that an active manager’s investment decisions and techniques will be successful. It is possible to lose some or all of your investment using active management.

Allianz Global Investors Distributors LLC, 1633 Broadway, New York NY, 10019-7585, us.allianzgi.com, 1-800-926-4456.

AGI-2015-08-03-12952