This blog post is provided for informational purposes only and should not be construed as investment advice. Any opinions or forecasts contained herein reflect the subjective judgments and assumptions of the authors only and do not necessarily reflect the views of Loomis, Sayles & Company, L.P. This information is subject to change at any time without notice.

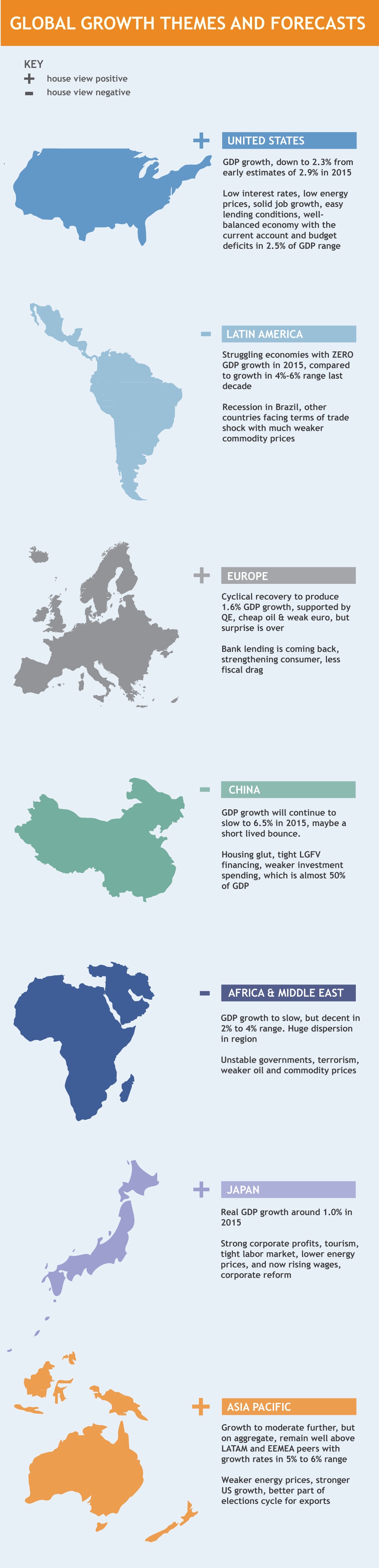

Every quarter, we update our forecast map. What's different this time? We have shaved our US GDP forecast down to 2.3% from 2.9%, mostly on account of weaker exports, a strong dollar and the decline in oil prices. In emerging markets, we still believe Asia Pacific is currently a bright spot - but we expect China to slow further as easing measures fail to gain traction.

Read on for our global highlights: