Following positive performance in the first quarter, emerging markets (EM) came under pressure from macroeconomic factors in the second quarter, resulting in mixed returns for the asset class:

- The global yield environment dramatically shifted

- Core rates rose sharply

- Positive US growth data increased expectations of a September hike

- The potential for a Greek exit from the EU and the correction in the Chinese equity market dampened global risk appetite and fueled market uncertainty

In the face of these negative headwinds, EM hard currency bonds outperformed global counterparts. During the second quarter, favorable technicals, some stabilization in commodity prices and attractive valuations left EM better positioned to weather the swift bond sell off in May, and the negative headlines in June.

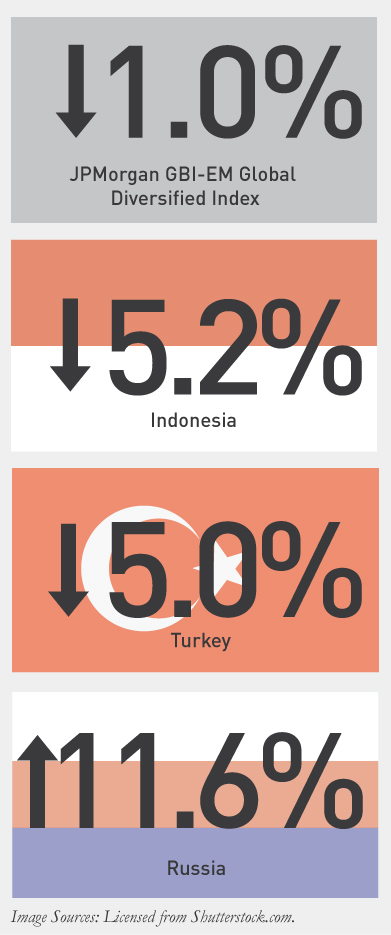

Currency

The JP Morgan GBI-EM Global Diversified Index was down -0.96% in Q2 2015, with both local rates and foreign exchange selling off. EM foreign exchange caught a brief reprieve at the start of Q2, but gains were short-lived and US dollar strength resumed.

Asia was the index’s worst regional performer in Q2. The weakness was led by Indonesia, down -5.21% on the heels of declining growth, reduced government expenditure and downward pressure on the Indonesian rupiah (IDR).

Turkey continued its slide, closing down nearly -5%. The lira weakened and rates sold off in the wake of political uncertainty following the general election in early June and on-going fiscal deterioration.

Russia was once again the top performer in the index, up 11.6% at the close of June. In Q2, the ruble returned nearly 5%, and local bonds were up 7%. A rebound in oil prices in May, optimism over a cease fire with Ukraine, high central bank interest rates, and expectation of cuts in the second half of 2015 enticed investors back into Russian debt.

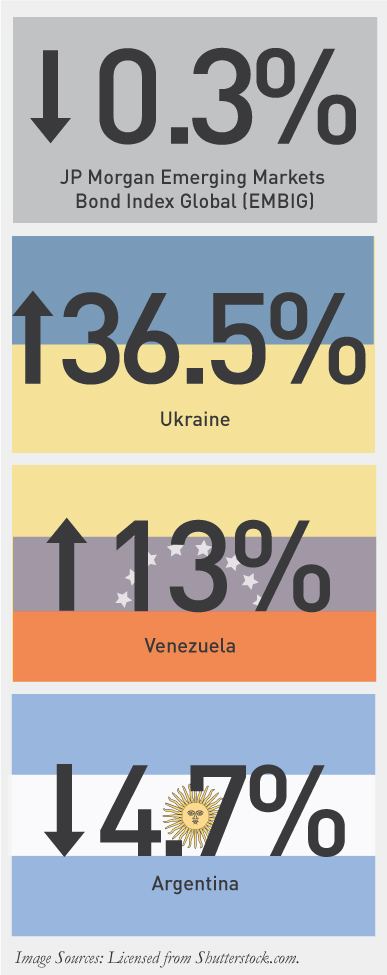

Sovereign USD Debt

The JP Morgan Emerging Markets Bond Index Global (EMBIG) ended the second quarter down -0.29%. There was a substantial divergence in returns, with the high yield component (up 3.53%) substantially outpacing the investment grade segment (down -2.19%). A rally in high beta risk assets drove performance, while rising Treasury yields hurt the higher quality, longer duration IG names.

The top performing country in Q2 was Ukraine, posting double digit gains, up 36.49%. Although Ukraine remains in debt restructuring talks with creditors, investors betting on a positive outcome lifted bond prices.

Venezuela was another top performing name, up nearly 13% in the second quarter. Venezuela secured financing to meet obligations through 2016, reducing its near term default risk and boosting bond levels.

The worst performer for the quarter was Argentina, down -4.71%. Bonds traded off following unfavorable political headlines ahead of the upcoming elections.

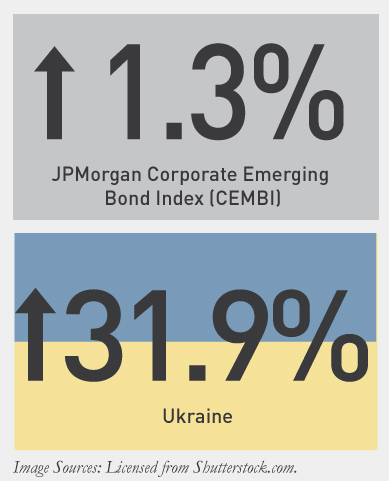

Emerging USD Corporate Debt

The JP Morgan Corporate Emerging Bond Index (CEMBI) returned 1.32% in the second quarter, with the high yield segment, 4.02%, largely outperforming the investment grade segment, -.11%. The spread on the index tightened 25 bps, demonstrating resilience in EM USD corporates, in the face of broader EM weakness.

As we saw in EM USD sovereigns, Ukraine led the pack in quarterly gains, returning 31.9%. Ukrainian bonds had sold off at the end of March, but rebounded in Q2 over investor speculation that restructuring will be successful over the near term.

Looking across sectors, metals & mining was a top performer in the second quarter, up 3.51%. Outperformance in high yield names in both Indonesia and Russia fueled returns.

Equities

The MSCI Emerging Markets Index returned flat gains, 0.82%, at the end of the second quarter. These returns were a result of slowing growth and volatility driven by the large correction in the Chinese equity markets.

2015 Outlook

In the second half of 2015, keep a keen eye on China, as it appears to be the growth engine of EM. Investors continue to question the viability of a 7% growth target. The Chinese government may step in with explicit policy to accelerate growth and calm concerns that a Chinese slowdown could ripple dramatically through emerging markets.