KEY TAKEAWAYS

· The Federal Reserve, China, oil prices, and the U.S. dollar continue to be the main drivers of bond price movements this summer.

· This week’s Fed meeting minutes may break the recent pattern, but investors may have to wait for the next employment report on whether recent high-quality bond strength continues.

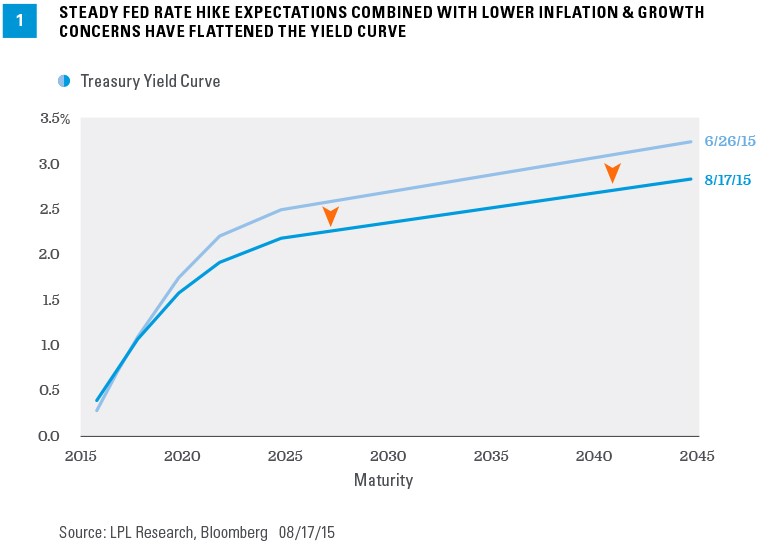

Music from four players continues to influence events in the bond market this summer: the Federal Reserve (Fed), China, oil prices, and the U.S. dollar. The music from these four players has led to a mixed response in the bond market: disturbing for short-term securities, melodic for long-term bonds. Displayed visually, the influence has led to a flatter yield curve [Figure 1]. Concerns over a potential first interest rate hike from the Fed next month have left short-term one- to two-year maturity yields unchanged to slightly higher, while China, oil prices, and the U.S. dollar have exerted downward pressure on longer-term bond yields.

BEHIND THE MUSIC

A closer look at the summer quartet:

· The Fed. Fed Chair Janet Yellen has stated multiple times over the summer that the economy remains on track to warrant a first rate hike “in 2015.” Although not specified, the move is expected to come either at the September or December meeting, since each is followed by a press conference and allows Yellen to explain the Fed’s rationale. Market expectations around a September rate hike have increased in recent weeks as domestic economic data, while mixed, continue to reflect continued modest expansion; in addition, Fed speakers have not wavered from their second half 2015 timeline for a rate hike—despite the changing tune from other players.

· China. Worries over a sharp stock market sell-off to start the summer morphed into currency fears after China lowered its currency peg to the U.S. dollar in a move to devalue its currency. Both developments increased global growth concerns, and the negative reaction was likely exacerbated by poorly communicated and executed policy. The fact that China’s bold moves to support its stock market failed to have their intended effect, and very limited communication around a currency devaluation, eroded investor confidence. The moves have only increased fears that the second-largest economy in the world may be slowing more than anticipated.

· Oil prices. Oil prices continue to hover at their lowest levels of 2015 and continue to stoke fears not only about the impact to the domestic oil industry but also about global growth. Oil supply has not meaningfully fallen and a recent modest increase in U.S. rig counts suggests that domestic producers continue to produce at near peak rates despite falling prices.

· U.S. dollar. Continued dollar strength has cast a shadow over a potential second half economic improvement and is viewed as deflationary. The U.S. dollar gradually moved higher again starting in late June, even though it has not reached prior peaks established in March and April of this year. Still, the increase is enough to maintain concerns that a strong dollar may continue to detract from earnings of U.S. multinational companies. Earnings growth is a key driver of stock prices and in turn, economic growth. The strong dollar contributed to lower commodity prices in 2015 and lower input prices for corporations and consumers.

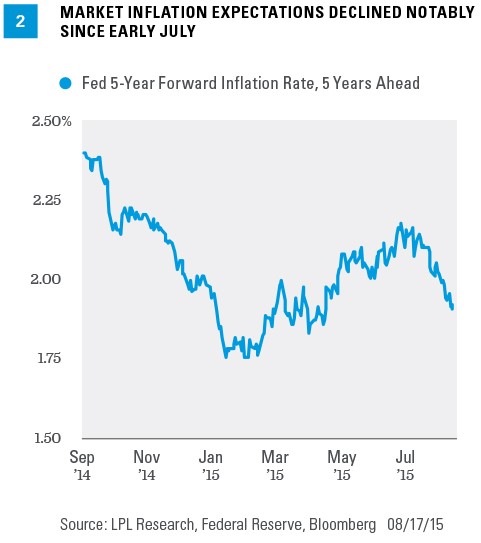

Of course, the trio of China, oil prices, and the U.S. dollar share the same tune in lower inflation expectations. One of the Fed’s preferred measures of market inflation expectations has decreased steadily since the start of summer [Figure 2]. The Fed’s measure of five-year inflation rates five years from now is less sensitive to oil price movements that influence implied inflation expectations embedded in Treasury Inflation-Protected Securities (TIPS) pricing. The measure shows that even aside from oil price declines, investors’ inflation expectations have broadly turned lower in recent weeks, a reflection that economic strength is not enough to generate inflation given ongoing challenges.

Both market inflation expectations and the summer decline in longer-term Treasury yields tell the same story: the Fed’s possible September interest rate hike may come at precisely the wrong time. In the event of a rate hike, the Fed would have to clearly justify why, given the uncertainty surrounding China, a notable decline in inflation expectations to just above the post-recession low established early in 2015, a strong U.S. dollar that may restrain corporate profits, and the absence of any noteworthy wage pressures. This may be a tall order considering the limited downside to merely waiting a few more months.

FED MINUTES

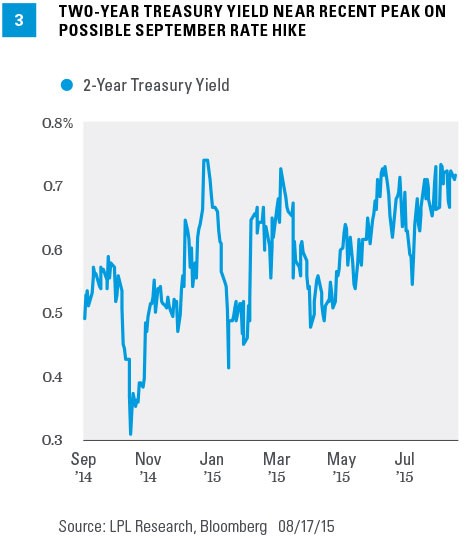

The release of the Fed meeting minutes this week may provide some clues into the Fed’s logic, but the information is dated. Since the July Fed meeting inflation expectations have declined further, China devalued its currency, and U.S. dollar strength continued. All of this new information will not be reflected in the minutes, but it still may shed light on the prospects of a September rate hike. The two-year Treasury yield sits near the highs of the year due to the uncertainty surrounding a potential first rate hike in a few weeks [Figure 3].

The release of Fed meeting minutes may break up the quartet that is influencing longer-term high-quality bond prices. Any hints that the Fed is taking note of lower inflation expectations, the dollar, and overseas developments may ease rate hike fears and, in turn, remove one of the drivers of the recent decline in longer-term Treasury yields. A later start to Fed rate hikes may boost inflation expectations and longer-term bond yields along with it. Conversely, lack of clarity may postpone a potential catalyst until the next jobs report in early September.

Ultimately, we expect the Fed to wait until December, or even early 2016, to raise interest rates. By then we expect further signs of economic improvement to gradually lift high-quality bonds yields higher and prices lower, keeping the challenging low-return bond environment in place.

IMPORTANT DISCLOSURES

wThe opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) may be appropriate for you, consult your financial advisor prior to investing. All performance reference is historical and is no guarantee of future results. All indexes are unmanaged and cannot be invested into directly.

The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values and yields will decline as interest rates rise, and bonds are subject to availability and change in price.

Government bonds and Treasury bills are guaranteed by the U.S. government as to the timely payment of principal and interest and, if held to maturity, offer a fixed rate of return and fixed principal value. However, the value of fund shares is not guaranteed and will fluctuate.

Treasury Inflation-Protected Securities (TIPS) help eliminate inflation risk to your portfolio, as the principal is adjusted semiannually for inflation based on the Consumer Price Index (CPI)—while providing a real rate of return guaranteed by the U.S. government. However, a few things you need to be aware of is that the CPI might not accurately match the general inflation rate; so the principal balance on TIPS may not keep pace with the actual rate of inflation. The real interest yields on TIPS may rise, especially if there is a sharp spike in interest rates. If so, the rate of return on TIPS could lag behind other types of inflation-protected securities, like floating rate notes and T-bills. TIPs do not pay the inflation-adjusted balance until maturity, and the accrued principal on TIPS could decline, if there is deflation.

Investing in foreign and emerging markets securities involves special additional risks. These risks include, but are not limited to, currency risk, geopolitical risk, and risk associated with varying accounting standards. Investing in emerging markets may accentuate these risks.

Currency risk is a form of risk that arises from the change in price of one currency against another. Whenever investors or companies have assets or business operations across national borders, they face currency risk if their positions are not hedged.

Commodity-linked investments may be more volatile and less liquid than the underlying instruments or measures, and their value may be affected by the performance of the overall commodities baskets as well as weather, geopolitical events, and regulatory developments.