Since the 2007-2009 global financial crisis, it seems like many markets have gone nowhere but up—most notably in the United States. Brooks Ritchey, Senior Managing Director at K2 Advisors®, Franklin Templeton Solutions®, says that amid the third-longest equity bull run in history, investors may not want to leave the game just yet, but would be wise to consider carrying an umbrella.

“I’d keep playing. I don’t think the heavy stuff’s gonna come down for quite a while.”

Carl Spackler (played by Bill Murray)

Caddyshack, directed by Harold Ramis, Warner Bros. Pictures, 1980.

To me, Caddyshack belongs in the pantheon of great films in cinematic history, though I do find myself in the minority when sharing this opinion with some of the younger generations in the office.

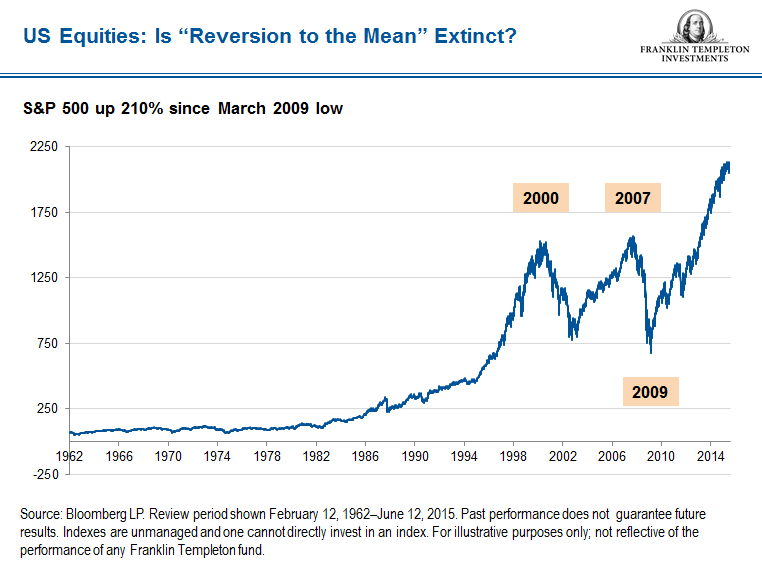

Critical observations aside, I think we all would agree that markets—like Caddyshack’s unflappable Carl Spackler—have demonstrated a remarkable level of post-2009 optimism and resilience. One could even go so far as to say investor sentiment has at times reflected a sanguine naiveté, or indifference to macro factors, driven forward with an unbridled confidence, fed steadily by a diet of central bank stimulus. Indeed, participants in US markets have apparently not seen the heavy stuff—or at least recognized it—for 2,336 days (as of July 31), representing the third-longest bull run in history.1

Even more compelling, it has been 1,398 days since the S&P 500 has experienced a correction of 10% on a closing basis.2

Resilient indeed!

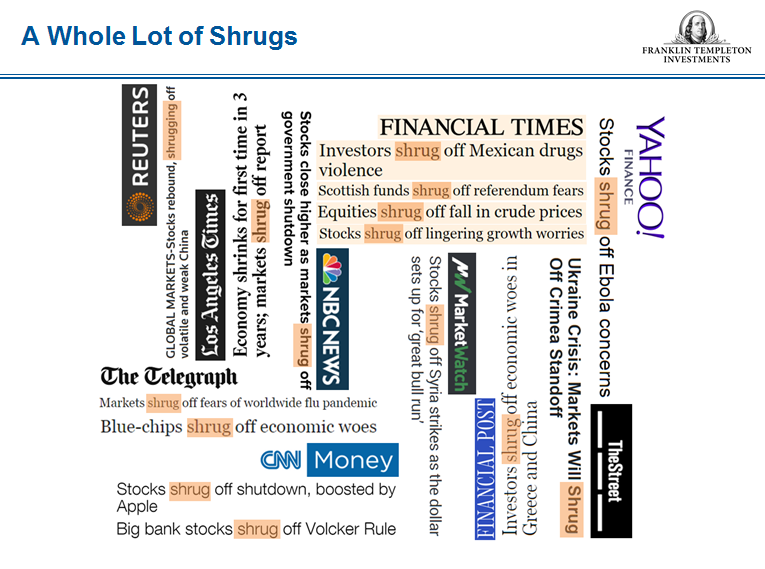

Out of curiosity, I recently searched Google for the terms “markets” and “shrugged” in the headline or body of news articles published over the six-year period from July 21, 2009, through July 21, 2015. My search yielded an incredible 31,000 results! The headlines (in no particular order) help jog the memory as to the many speed bumps we’ve passed along the way—potential obstacles blown past without so much as a basis point3 shudder.

A Whole Lot of Shrugs

Here are a few of these headlines:

And the list goes on. My shoulders hurt . . .

To be clear, I am not attempting to predict a market top or correction, or suggest that we all run for the exits. The question is whether the positive momentum can continue. In my opinion, probably. I thought the Chinese market rout this summer could have been the proverbial straw, but the band played on. From our point of view, trying to predict market declines or rallies is not as important as preparing for incipient shocks smartly and strategically; it is about being vigilant. What I am 100% certain of is the markets will correct—eventually.

And when that happens, and the heavy stuff is at long last upon us, I would like to be well on my way to the clubhouse—or at least have a good sturdy umbrella.

Actively Managing Risk

Perhaps the more important takeaway is that particularly during market extremes, risk management is of utmost importance. K2’s Founding Managing Director David Saunders believes the key to obtaining long-term, positive asymmetric returns lies in minimizing downside capture through actively managing risk. It is about compounding performance over time. Saunders also likes to remind us that bear markets can hurt more and last longer than investors realize—or wish to recall. Averages of course can be deceiving and lead to false impressions. Consider that during the downturn in 1973-1974, it took 7-1/2 years for the market to climb above water, and in 2000-2002 investors did not break even until 20074 (and we know what happened then).

From my viewpoint, there really is only one reasonable way forward. Equity exposure has been a winning investment strategy since 2009, but we believe the winners in the next market phase will be those that demonstrate the most discipline and risk management.

Implicitly, it is our view that the best way to mitigate market risk is through active investment management. The alternative simply means one is willing to go along for the ride, letting the market dictate direction and control. I prefer to have my hands on the wheel (and use the brakes as well).

I prefer to have an umbrella in my golf cart. The market is like a storm cloud threatening to end our game; while it may bring only a mere drizzle, it is not wise to be on the course when lightning strikes. Akin to the Caddyshack theme song, the market may have been telling us, “I’m alright, nobody worry ’bout me.” But we say, shrug at your own risk.

Brooks Ritchey’s comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

This information is intended for US residents only.

What Are the Risks?

All investments involve risks, including the possible loss of principal. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Bond prices generally move in the opposite direction of interest rates. Thus, as the prices of bonds in a portfolio adjust to a rise in interest rates, its value may decline.

1 Source: Bloomberg LP.

2 Source: Bloomberg LP. Indexes are unmanaged and one cannot directly invest in an index. Past performance is no guarantee of future results. For additional data provider information, see www.franklintempletondatasources.com.

3 Basis points represent a unit of measure for interest rates and percentages in finance; one basis equals one-hundredth of one percent.

4 Source: Bloomberg LP.

© Franklin Templeton Investments